Come see this jewel on the coast, The Sequin – 201 Bridgeport in El Granada. This coastal gem features 3 bedrooms and 2 full baths. Freshly painted in and out, step into a cozy living area with custom built in book shelves nestling the fireplace. A reading nook, garden window and skylights round out this space. Venture into the dining area off the kitchen and catch all the action. With updated counters and backsplash, this kitchen is open and inviting. With garden window over the sink and sliding door to the back yard, the outdoors are welcomed in. Down the hall you’ll find the washer and dryer behind the curtain. The hall bath features shower over tub, stylish sink and modern vanity. The primary suite is tucked in back, with shower over tub and rain water shower head. Low maintenance yard with Hot Tub Included. 2 car garage with electrical vehicle charging station. Come enjoy the coastal life at The Sequin. Postal code is Half Moon Bay, home is physically in El Granada. Yearly HOA of $150 includes neighborhood park, close to the harbor, beaches and great dining. Welcome Home to “The Seaquin”.

Call| Text | Sabrina 650.799.4333 |Susan 650.796.0654 | EMAIL | WEB| BLOG

We love what we do and would love to help you navigate your sale or purchase of Residential Real Estate. Please reach out for a personal consultation. Please enjoy our free resources below and get to know our team from our TESTIMONIALS.

Effective. Efficient. Responsive. The Caton Team 🏡 How can The Caton Team help You?

Got Real Estate Questions? The Caton Team is here to help.

We strive to be more than just Realtors – we are also your home resource. If you have any real estate questions, concerns, need a referral, or some guidance – we are here for you. Contact us at your convenience – we are but a call, text or click away!

The Caton Team believes, in order to be successful in the San Fransisco | Peninsula | Bay Area | Silicon Valley Real Estate Market we have to think and act differently. We do this by positioning our clients in the strongest light, representing them with the utmost integrity, while strategically maneuvering through negotiations and contracts. Together we make dreams come true.

A mother and daughter-in-law team with over 35 years of combined, local Real Estate experience and knowledge – wouldn’t you like The Caton Team to represent you? Let us know how we can be of service. Contact us any time.

Call| Text | Sabrina 650.799.4333 | Susan 650.796.0654 | EMAIL | WEB | BLOG

The Caton Team – Susan & Sabrina A Family of Realtors Effective. Efficient. Responsive. What can we do for you?

Finding an affordable loan can seem challenging, especially when you need to borrow money quickly. You must watch out for unfair practices called predatory lending. This is when lenders take advantage of borrowers who don’t understand how loans should work or anyone who is having financial difficulties and needs to find a loan fast. Learning how to spot the signs of predatory lending practices is the best way to identify and avoid a potential financial trap.

What Are Predatory Lending Practices?

Predatory lending is any loan with deceptive, unfair, or illegal terms. These loans frequently have high interest rates, high fees, and other terms that make the loan more expensive and difficult to repay. People who don’t know how loan terms should work and anyone in a financially desperate situation are most at risk of falling victim to predatory lending. If you have a low credit score or require a loan because you struggle to pay your bills or afford another necessary expense, you could be a target. Lenders also often target women and minorities.

Signs and Tactics of Predatory Lending

Lenders who use predatory tactics may try to talk you into taking out a loan despite your concerns regarding your ability to pay it back. They might also offer to help you navigate the loan process to steer you into taking out a loan with less than favorable terms. Some common signs of predatory lending to watch out for include:

High interest rates: Rates that exceed market value or what is standard for your credit score.

Hidden and high fees: Hidden fees or those above the loan type’s average range.

High prepayment penalties: Additional fees for paying the loan in full before the term ends.

Offering too much credit: Beware if your lender is offering you more credit than you can afford.

Balloon payments: A single high payment at the end of the loan that gives the illusion of low monthly payments.

Steering: When a lender tries to get you to accept a subprime, and therefore more expensive, loan even when your credit qualifies you for better terms.

Loan flipping: When a lender offers to extend or refinance the loan and charges new fees each time.

Terms that cost the borrower equity: Homeowners who take out a loan that’s hard to pay back might lose equity in their home.

Asset-based lending: Loans that use an asset like your home or car as collateral. You risk losing the named asset if you fail to repay the loan according to the terms set.

Lower credit-rated loans: Offering terms suited to a lower credit score despite the borrower qualifying for better terms.

Add-ons: Charging more for unnecessary services.

Aggressive lending tactics: Pushing you to accept the loan even if you’re unsure.

Lack of transparency: Failure to disclose all costs and terms before you sign.

Exploitation: Taking advantage of a borrower’s lack of knowledge regarding finances and loans.

Predatory lending is dangerous because it’s practiced even by seemingly reputable lending institutions like banks and mortgage brokers. Many customers encounter deceptive lending when actively searching for a loan, but some predatory lenders send out loan offers in the mail, by phone, and advertise on various media channels.

Types of Loans Associated With Predatory Lending

Any type of loan can be predatory, but some are more prone to using these deceptive practices.

Subprime Mortgages

Lenders may push you into a high-interest loan with poor terms not only to make more money but to benefit from the foreclosure of your home if you can’t make your payments. It’s important to weigh the risks of the loan, understand your finances, and have the ability to make timely payments before you take out any loan.

Payday Loans

Another common example of predatory lending is payday loans. These are short-term loans you are meant to repay with your next paycheck. They have extremely high interest rates and fees. Most borrowers who take out these types of loans have a pressing need for fast cash. Many end up extending the loan and racking up higher debt.

Auto-Title Loans

Stay wary of loans that require your car title as collateral. Auto title loans generally have high interest rates, and the lender can seize your vehicle if you fail to repay the loan.

Unfortunately, lenders come up with new predatory loan strategies all the time. Practices, like buy now and pay later are just one example of how lenders may use unclear loan terms to draw you in.

Anti-Predatory Lending Laws

The government has taken action to help stop lenders from targeting borrowers with unfair loan terms. Most states have some form of anti-predatory lending laws. Consumer protection laws include:

Many states now have some form of anti-predatory lending laws. Regardless, some damage can’t be undone, and borrowers may have lost their homes or gone bankrupt. It’s better to stay vigilant and read the fine print when searching for a loan instead of risking serious consequences later on to secure a loan fast.

How to Protect Yourself From Predatory Lending

Predatory lending is a crime, but that doesn’t stop lenders from trying to take advantage of borrowers who aren’t financially literate. The best way to avoid getting caught in a predatory lending scheme is by educating yourself and comparing offers from several lenders to find the best terms.

Cell| Sabrina 650.799.4333 |Susan 650.796.0654 | EMAIL | WEB| BLOG

We love what we do and would love to help you navigate your sale or purchase of Residential Real Estate. Please reach out for a personal consultation. Please enjoy our free resources below and get to know our team from our TESTIMONIALS.

Effective. Efficient. Responsive. The Caton Team 🏡

Got Real Estate Questions? The Caton Team is here to help.

We strive to be more than just Realtors – we are also your home resource. If you have any real estate questions, concerns, need a referral, or some guidance – we are here for you. Contact us at your convenience – we are but a call, text or click away!

The Caton Team believes, in order to be successful in the San Fransisco | Peninsula | Bay Area | Silicon Valley Real Estate Market we have to think and act differently. We do this by positioning our clients in the strongest light, representing them with the utmost integrity, while strategically maneuvering through negotiations and contracts. Together we make dreams come true.

A mother and daughter-in-law team with over 35 years of combined, local Real Estate experience and knowledge – wouldn’t you like The Caton Team to represent you? Let us know how we can be of service. Contact us any time.

Cell | Sabrina 650.799.4333 | Susan 650.796.0654 | EMAIL | WEB| BLOG

The Caton Team – Susan & Sabrina A Family of Realtors Effective. Efficient. Responsive. What can we do for you?

There’s no guarantee a lender will approve your mortgage application. Here’s a look at how lenders decide to extend credit, and some common reasons why mortgage applications get rejected.

For borrowers in today’s expensive housing market, getting approved for a mortgage can be a challenge. Mortgage rates have soared from pandemic-era lows, home values are near record highs and home price appreciation is outpacing wage growth.

All of that means there’s no guarantee a lender will approve your mortgage application. Here’s a look at how lenders decide to extend credit, and some common reasons why mortgage applications get rejected.

How does mortgage underwriting work?

Mortgage underwriting is the process of verifying and analyzing the financial information you provide your lender — all with the goal of giving you an answer of yes, no or maybe. As part of the application, you hand over bank statements, W-2s and other tax documents, recent pay stubs and any additional documentation the lender requires.

Dispense with any stereotypes about the old days of lending or the movie “It’s A Wonderful Life”, when a banker determined your creditworthiness by the firmness of your handshake and the crispness of your shirt. In most cases, a loan officer or mortgage broker will collect your information and submit it to an underwriting software system. Loans that will be sold to Fannie Mae, for example, use Desktop Underwriter (DU), while loans sold to Freddie Mac leverage Loan Product Advisor (LPA).

Fannie Mae and Freddie Mac are government-sponsored enterprises that interface with lenders to keep the mortgage market stable. Between them, they buy or back about two-thirds of all U.S. home loans.

Systems like DU and LPA don’t allow for much in the way of human judgment. The software determines whether you’re either approved, rejected or asked for additional information.

Such automated underwriting, as it’s officially called, is the norm nowadays — part of the reforms to the mortgage financing world developed after the 2007–09 mortgage meltdown and subsequent financial crisis. “Prior to the crisis, there was more leeway,” says Bill Banfield, chief business officer at Rocket Mortgage. “Now, most of that subjectivity is gone.”

There are many reasons — from your income to the type of property you’re buying — that you could see your mortgage declined by underwriter software. And if it does, there may be little the human loan officers can do about it.

Keep in mind: Beyond your approval or denial, the main thing the lender decides during underwriting is your mortgage’s interest rate. They also use underwriting to determine how much to charge you in fees.

Reasons for mortgage denial

“There are a thousand potential questions Fannie (or Freddie) could return,” says David Aach, chief operating officer at Blue Sage Solutions, a mortgage technology firm. “That’s the nightmare of the underwriting process.” Here are some of the more common reasons underwriters reject mortgages.

1. You have credit issues

Your credit score is the single most important factor in determining your mortgage rate – and whether you get approved at all. Generally, the best deals go to borrowers with credit scores of 740 or above, and ones in the “good” range — 670 to 739 — are the most desirable.

You can qualify for some types of mortgages with much lower scores than others. For instance, VA loans are generally available to borrowers with scores of 620 or above, while loans backed by the FHA can go to those with scores as low as 500.

Before applying for a mortgage, check your credit score and credit report and dispute any errors. If your credit score is low, work on boosting it before you apply (for example, you could ask a card company to increase your credit line, which automatically lowers your credit utilization ratio). If you have a qualifying credit score, make sure you don’t do anything during the mortgage process to cause it to drop, like miss a payment, max out a credit card or apply for some other new loan.

If you don’t have a credit score at all, some lenders do have alternative credit scoring methods, such as analyzing your bank deposits. In fact, in January 2025, Fannie Mae released a new update to DU in support of “increasing access to credit for populations such as those with limited or no credit histories.”

2. You have an income shortfall

Your debt-to-income (DTI) ratio — the portion of your gross (pre-tax) monthly income spent on repaying regular obligations — signals to lenders whether you’re in a position to take on an additional major debt. If your DTI is too high, you may be rejected for a mortgage. Most lenders require a DTI of less than 43%. Some will go up to 50% if you have factors to offset that higher DTI, like a big savings account.

Aim for your payment obligations to make up about one-third of your income: A DTI around 36% is the ideal, qualifying you for better loan terms. If you owe a lot in student loans, car loans or credit card balances, work on bringing those balances down before applying for a mortgage.

Also, think about the length of the loan: The longer its term, the more affordable its monthly payments. So, opting for a 30-year mortgage might lower your chances of getting your mortgage declined by underwriter software. Keep in mind, though, that you’ll pay more in interest over the loan’s lifespan, compared to shorter-term loans.

On the income side, issues often emerge when the mortgage applicant is self-employed. The software is geared to W-2s — the wage-and-tax-statement from an employer — and might flag your file when you use alternative ways to prove your income. It might also cause an issue if your income stream is irregular, even if your earnings are high.

Also, business owners often maximize write-offs and expenses when doing their taxes — but that common practice flummoxes the underwriting models. “Self-employed people know what they make, but they don’t know what an underwriter is looking for,” says Tom Hutchens, president at Angel Oak, a lender specializing in non-qualified mortgage (QM) loans (mortgages outside the conventional criteria). “They might be fully approved, but then an underwriter looks at the tax returns” and sees that “$10,000 a month might become $5,000 a month in income.” The lower amount upsets the software, which then dings the applicant.

3. The loan-to-value (LTV) ratio is too high

Lenders also look at how much of a mortgage you want vis-à-vis the value of the home you’re buying — something called the loan-to-value (LTV) ratio.

The bigger your down payment, the less you borrow, and the lower your LTV. For instance, if you’re buying a $400,000 house with a down payment of $80,000, your LTV is a comfortable 80%. But if you’re putting down $20,000 and financing the remaining $380,000, the LTV is up to 95%. (While there’s no single perfect LTV percentage, lenders usually like to see it around or below 80% — for conventional loans, anyway.)

Low down payments are one of the big reasons for mortgage denial. The higher your LTV, the higher the likelihood that your loan will be flagged for follow-up questions, or rejected altogether. If you feel you need help lowering your LTV, look into down payment assistance — every state has these programs, especially for first-time buyers — to increase the amount of cash you can bring to the deal.

4. You’re trying to finance an out-of-favor property

Not all homes are created equal, as far as lenders are concerned. The traditional, detached single-family residence still rules, and alternatives can confound.

Condos are one particularly tough type of home to finance. In response to the June 2021 collapse of an oceanfront tower near Miami, Fannie and Freddie rolled out new rules covering condo loans. The giant mortgage market-makers have decided not to finance some buildings that have low reserves, need repairs or are facing lawsuits. Critics say the stricter reviews are causing condo sales to fall apart, even in buildings with no structural issues.

Manufactured homes also can be challenging to finance. And if appraisers or inspectors find a structural flaw or other issue with the home itself, that also can slow the approval, or even kill it.

5. Something recently changed in your financial life

The lending process prizes financial stability and predictability (remember what we said about income, above). Unfortunately, a recent job change or period of unemployment can throw a wrench in your approval. A short employment history or interruption in earnings sends warning signals to the software, too.

Unusual activity in your bank account can be another issue, even if it grows your cash reserves. Large, unusual deposits might indicate you borrowed money for your down payment — which you may need to repay along with your mortgage. If you got money from relatives to help you buy a house, make sure to submit a gift letter as part of your application.

6. You don’t meet the loan program’s requirements

Different types of loans come with different specifications.

If you want to get an FHA-insured loan, for example, your house can’t exceed the loan limit applicable to the location. In 2025, that is $524,225 in most areas. The house also needs to pass a special type of appraisal that looks at the property’s condition. The specifics put in the place by the FHA add more potential reasons for mortgage denial.

Similarly, loans backed by the VA and the USDA have their own unique requirements.

On top of all of this, lenders generally have their own proprietary guidelines. Failing to meet any of them can lead to your mortgage application being denied.

7. You’re missing information on your application

Make sure to fill out the mortgage application in its entirety. If it’s incomplete, the underwriting software might discard your application, resulting in an automated rejection.

How to get a mortgage after your application is denied

If you have a unique income situation, such as owning a business with unsteady cash flow, you might apply for a non-QM mortgage. These loans come with more flexible credit criteria and income requirements than conventional loans, making them ideal for those who don’t fit within the standard borrower box.

If your credit score or LTV was the problem, you can also consider loans backed by the FHA or VA. Their terms are more generous, geared toward borrowers with lower credit scores or little cash for down payments.

Manual underwriting

The vast majority of conforming loans — those eligible to be bought by Fannie and Freddie — are decided via automatic underwriting. It’s fast, cheap and takes bias out of the process. But some loans are still reviewed by a human. Lenders often do manual underwriting when an application would likely be denied through an automated system, or if the borrower has some unusual circumstances but is otherwise qualified.

Certain types of mortgages, like jumbo loans and non-QM loans, are more likely to be manually underwritten. But you can request it for any mortgage, if you believe your particular situation will not be fully understood by the software. Be prepared to supply additional paperwork — financial statements reaching farther back, for example — and for a longer process. Bear in mind that, even with a manual underwriter, your loan still has to conform to specific requirements.

Bottom line

The mortgage application process can be full of surprises — with a key one being that an automated underwriting system often decides your approval or denial. The key reasons underwriters reject mortgages often involve credit score issues, income shortfalls, high LTV ratios, property type or recent changes in your financial situation. But the software doesn’t necessarily have to have the last word.

Find out why your application was denied, and then seek remedies. You can explore alternatives to conventional conforming loans, or request manual underwriting (a review by a human underwriter), for example. Any of these may provide a pathway to homeownership.

FAQs

How long do underwriters take to approve a mortgage?

It depends on the lender, the tools they use and how good you were at providing the required information. On average, it takes about 44 days to close a new-purchase mortgage.

How worried should I be about underwriting?

Not very. Take steps before you approach lenders — like paying down other debts and improving your credit score — and you should feel confident when applying. If you’re still nervous, you can explore prequalification before you seek preapproval. This is a less stringent process that can give you an idea of where you stand.

What are some things I should not do during underwriting?

To avoid a mortgage declined by underwriter teams, do two things. First, don’t make any financial changes. Keep paying your bills on time and don’t open any new loans or lines of credits. Second, stay responsive. The lender might ask for additional information. If you don’t provide it in a timely manner, it can lead to denial.

I read this article HERE. By Jeff Ostrowski, Bankrate.com

Got Questions? The Caton Team is here to help.

Cell| Sabrina 650.799.4333 |Susan 650.796.0654 | EMAIL | WEB| BLOG

We love what we do and would love to help you navigate your sale or purchase of Residential Real Estate. Please reach out for a personal consultation. Please enjoy our free resources below and get to know our team from our TESTIMONIALS.

Effective. Efficient. Responsive. The Caton Team 🏡

Got Real Estate Questions? The Caton Team is here to help.

We strive to be more than just Realtors – we are also your home resource. If you have any real estate questions, concerns, need a referral, or some guidance – we are here for you. Contact us at your convenience – we are but a call, text or click away!

The Caton Team believes, in order to be successful in the San Fransisco | Peninsula | Bay Area | Silicon Valley Real Estate Market we have to think and act differently. We do this by positioning our clients in the strongest light, representing them with the utmost integrity, while strategically maneuvering through negotiations and contracts. Together we make dreams come true.

A mother and daughter-in-law team with over 35 years of combined, local Real Estate experience and knowledge – wouldn’t you like The Caton Team to represent you? Let us know how we can be of service. Contact us any time.

Cell | Sabrina 650.799.4333 | Susan 650.796.0654 | EMAIL | WEB| BLOG

The Caton Team – Susan & Sabrina A Family of Realtors Effective. Efficient. Responsive. What can we do for you?

You’re probably aware that your credit score holds a lot of weight in determining your financial health and can influence a lot of major life decisions. It affects everything from loan approvals to interest rates.

Among the factors influencing your credit score, payment historyis the biggest one, accounting for about 35% of your total FICO score. Late payments can seriously impact your credit score, leading to long-term financial consequences. Understanding their impact and learning to avoid them can help you maintain a healthy long-term credit score and avoid costly mistakes.

Keep reading as we explain how late payments affect your credit score, the broader consequences they bring, and practical strategies to avoid missing payments.

How Late Payments Affect Your Credit Score

When you make a late payment on any debt—whether a credit card, mortgage, auto loan, or student loan—it can significantly hurt your credit score. The total impact depends on several factors, including how late the payment is and your credit history before the missed payment.

1. The 30, 60, and 90-Day Rule

Creditors will usually report any late payments to credit bureaus once a payment hits the 30 days late mark. Payments 30 days past due can drop your overall score by 60 to 110 points, depending on your previous credit standing. The longer a payment remains unpaid, the more damage it does:

30 Days Late: The impact can still be remedied at this stage if the payment is quickly made, though you may incur late fees.

60 Days Late: After 60 days, your credit score drops further, and additional fees may accumulate. Repeated 60-day late payments signal a larger financial issue to creditors, further reducing your credit score.

90 Days Late: Once payments are 90 days late, they cause significant damage to your credit score. Accounts that reach this stage may be sent to collections, leading to a mark on your credit report that can remain there for seven years.

2. How Long Do Late Payments Stay?

As mentioned above, a late payment can stay for up to seven years on your credit report. This is calculated from the date of the first missed payment.

However, the impact of a late payment on your score will slowly decrease as time goes by, especially if you continue to make on-time payments. Generally, your score is most affected in the first two years after a missed payment.

Broader Consequences of Late Payments

Late payments don’t just hurt your credit score—they can lead to a range of other financial challenges that affect your overall financial health. Have you ever heard of the snowball effect?

1. Increased Interest Rates

Late payments indicate a higher level of risk to potential lenders, which can result in higher interest rates on future loans. Higher interest rates mean you’ll pay more over time, whether on a mortgage, personal loan, or credit card balance.

Some issuers of existing credit cards impose a penalty APR after a late payment. This higher interest rate can apply to your balance and any new purchases, making it harder to pay down your debt.

2. Difficulty Securing New Credit

Lenders evaluate your payment history when you apply for new credit. Recent late payments on your record may lead to denied applications for loans, credit cards, or even rental agreements. Even if you’re approved for credit, you will likely receive less favorable terms, such as higher interest rates or lower credit limits.

3. Late Fees and Increased Debt

Your creditor will likely charge a late fee when you miss a payment. Over time, these fees can add up and compound your debt, especially if you miss multiple payments. Some credit card companies could also impose a penalty APR, which can increase the amount of interest you’re charged on your balance, further deepening your financial burden.

4. Collections and Legal Action

The creditor may send your account to a collections agency if a payment remains overdue for several months. This can lead to additional damage to your credit score, as accounts in collections appear as negative marks on your credit report. In extreme cases, creditors might also take legal action to recover unpaid debts, resulting in wage garnishment or other legal consequences.

How to Avoid Late Payments

The best way to avoid the financial consequences of late payments is to stay proactive about your bills and financial obligations. Here are several strategies to help you avoid missing payments and protect your credit score:

Set Up Automatic Payments

One of the easiest ways to avoid missed payments is by selecting auto-pay for recurring bills. It is usually pretty easy to go into the interface and set up these scheduled payments, creating one less thing for you to worry about each month. You can decide whether you want to make minimum payments or pay in full, if you have the budget, it is always best to pay the full statement balance each month.

Use Payment Reminders

If you prefer to make manual payments, set up reminders to alert you when a payment is due. Many financial institutions and credit card issuers allow you to opt into email or text reminders a few days before your payment date.

Create a Budget

Late payments often result from cash flow issues, where you simply don’t have enough funds to cover your bills. Creating and sticking to a budget helps ensure that you always have money set aside to cover essential expenses, such as credit card payments, loans, utilities, and rent. Budgeting apps or simple spreadsheets can help you track your spending and set aside money for bills.

Build an Emergency Fund

An emergency fund is critical to ensuring you can make payments on time, even when unexpected expenses arise. Aim to set aside three to six months’ worth of living expenses in an easily accessible account to cover costs like medical bills, car repairs, or job loss.

Contact Your Lender for Assistance

If you know you’ll be late on a payment, it’s better to contact your lender in advance. Many creditors will work with borrowers by offering temporary payment plans, deferring payments, or waiving late fees if you can explain your financial situation.

How to Recover From Late Payments

If you’ve already missed a payment and seen the effects on your credit score, you can take steps to repair the damage.

Make All Future Payments on Time: The best way to improve your credit score after a late payment is to make sure all future payments are made on time. As the negative mark ages, its impact will diminish.

Pay Off Any Outstanding Debt: Reducing your overall debt will help improve your credit score over time and reduce the amount of interest you pay. Prioritize high-interest debt and work to lower your balances.

Dispute Errors on Your Credit Report: If you believe a late payment was incorrectly reported, you can dispute the error by calling the credit bureau. Providing documentation and proof of payment can help remove inaccuracies from your report.

Don’t Let Late Payments Get the Best of You

Late payments can be detrimental to your financial health and your credit score, affecting everything from interest rates to loan approvals and future life decisions.

However, with careful planning, automatic payments, and proactive communication with lenders, you can avoid missed payments and maintain a strong credit profile. If you’ve already made a late payment, there’s still hope for recovery through timely payments and reducing your debt over time. By understanding the impact of late payments and how to avoid them, you can take control of your financial future and protect your credit.

Cell| Sabrina 650.799.4333 |Susan 650.796.0654 | EMAIL | WEB| BLOG

We love what we do and would love to help you navigate your sale or purchase of Residential Real Estate. Please reach out for a personal consultation. Please enjoy our free resources below and get to know our team from our TESTIMONIALS.

Effective. Efficient. Responsive. The Caton Team 🏡

Got Real Estate Questions? The Caton Team is here to help.

We strive to be more than just Realtors – we are also your home resource. If you have any real estate questions, concerns, need a referral, or some guidance – we are here for you. Contact us at your convenience – we are but a call, text or click away!

The Caton Team believes, in order to be successful in the San Fransisco | Peninsula | Bay Area | Silicon Valley Real Estate Market we have to think and act differently. We do this by positioning our clients in the strongest light, representing them with the utmost integrity, while strategically maneuvering through negotiations and contracts. Together we make dreams come true.

A mother and daughter-in-law team with over 35 years of combined, local Real Estate experience and knowledge – wouldn’t you like The Caton Team to represent you? Let us know how we can be of service. Contact us any time.

Cell | Sabrina 650.799.4333 | Susan 650.796.0654 | EMAIL | WEB| BLOG

The Caton Team – Susan & Sabrina A Family of Realtors Effective. Efficient. Responsive. What can we do for you?

More buyers and homeowners want wellness features in their homes, and real estate agents need to be ready to deliver.

Architects, designers and wellness experts are curating wellness spaces for individual and group activities in large part because of demand for these kinds of features. Certain demographics such as Gen Zers and Millennials show extra interest, according to McKinsey’s latest wellness report, which pegged the 2024 global market at $1.8 trillion. Real estate professionals will find more and more of their customers seek homes with wellness-specific features or examples of how to add wellness into their lives.

Here are ways to share with homeowners how wellness can become part of their residential surroundings and lives:

Use Natural Elements in the Home

To fashion the right backdrop and mood for a wellness space, more professionals incorporate the tenets of biophilic design, which connects users to nature through views and access to the outdoors and choices of natural materials. Designer Alena Capra, CMKBD, who works with Armina Stone, a large importer and fabricator of natural stone, suggests using natural stone to surface countertops, walls and floors. “Whether it’s a stone accent wall, cladding on shower walls, countertops in a spa or primary bath or even counters in a home gym, the ability to bring in a bit of natural stone for that connection with nature is something we are seeing more of in residential and commercial interiors,” she says. Among popular choices are marble, quartzite and even semi-precious stone in serene colors.

Another option is to paint walls and ceilings in a limewash, a breathable, natural material that allows moisture to evaporate and prevent mold and mildew growth, says real estate salesperson Delaney Fox of Keller Williams Luxury International SVSI in Ketchum, Idaho. Some also like to install a kill switch to pare exposure to magnetic electromagnetic fields (EMF), Fox says.

Make Relaxation Intentional

Morgante Wilson Architects sees more clients look to the built environment to improve their mental and physical well-being, whether it’s installing spaces that maximize connectivity with others or locations with direct access to natural elements like water. “Many want a spa experience to help them decompress,” says firm associate architectural designer Kevin Thayer. More people are installing wet rooms that include both a shower and tub to save space and make rinsing off after a bath easier. These spaces require less square footage than a traditional primary bathroom does, a trend also noted by Houzz.

The home gym is still popular, especially with the rise of online fitness classes post-pandemic. Thayer says homeowners want functionality and style, which his firm elevates through Scandinavian-style hardwood flooring rather than rubber matting.

For a bigger investment and new twist, some install cold plunge pools and saunas indoors or outdoors, Fox says. The therapeutic benefit is that getting into the cold water can reduce inflammation and it’s said to be great for longevity, regeneration and clarity, she says.

Still another new option is what designer Sharon McCormick, Sharon McCormick Design, Allied AIA-CT, terms a “Zen Den,” a room designed for Zen meditation or Nia—a combination of holistic modern dance, martial arts and mindfulness workout. “Mindfulness is a hot topic as the general public becomes more informed of the practice and its positive effect on mind, body and soul and to ease anxiety and anger,” McCormick says.

Communal Wellness in Multifamily

Developers of condominium and apartment buildings are adding choices as wellness trends extend beyond pilates and yoga and more buildings hire wellness experts to launch experiences. Salesperson Claire O’Connor of O’Connor Estates sees more sauna and cold plunge pools in the luxury mix.

Curated Options

Related Group, a multifamily developer, incorporates more saunas but also newer features such as salt spa rooms to improve breathing and promote relaxation. The company’s St. Regis Residences in Miami also includes a relaxation area and juice bar. At its Rivage Bal Harbour in Miami Beach, there are hammam spa amenities, which use hot steam to encourage a deep and invigorating cleanse.

At 200 Amsterdam in New York City, SJP Properties designed amenities to inspire creativity and relaxation. Residents can enjoy a soundproof rehearsal room, a children’s playroom featuring a performance stage and costume area, luxurious rain showers and golf simulators with championship courses for an immersive experience.

Immersed in Nature

The wellness trend has moved outdoors where setting aside land for green parks and trails encourages healthfulness amid fresh air. The town of Tower at Trilith in Fayetteville, Ga., planned its sustainable environment with a large central park and 19 pocket parks so that homes face or are within one block of green space. There are also 15 miles of pedestrian pathways throughout the planned town, says Rob Parker, president. Many homes were also designed with a small footprint—down to 500 square feet for its micro models—for easy maintenance and the conservation of land for shared purposes.

Developer Lendlease took a similar step when it developed outdoor space at two downtown Chicago buildings, which nearby residents and workers can also use. As part of its Cirrus development, a 350-unit condominium tower on Lake Michigan, the firm designed Cascade Park, an adjacent public space with series of switchbacks that provide lakefront access, transforming what was once a 50-foot elevation change into a safe, accessible connection to the lakefront and its adjacent trail. Cirrus also features The Conservatory, a 900-square-foot biophilic space with raised garden beds, vegetation and seating nooks.

Another example, located in Chicago’s South Loop, is The Reed at Southbank. The 440-unit residential tower features a central lawn, stone amphitheater and native plantings. Meandering walkways link to a new riverwalk with viewing platforms and seating, providing settings that support physical and mental well-being and community interaction.

Focus on Indoor Air Quality

More residential builders and homeowners are focused on HVAC systems and technologies that help curtail air leakage and perform more sustainably such as Aeroseal. More also build to higher green standards, through a leading sustainable certification program known as BREEAM. Health and well-being feature strongly in the certification, which addresses and rewards building features that improve indoor air quality such as ventilation systems designed to reduce pollutant exposure, use of low-emission materials and monitor systems that track and maintain healthy air levels.

It also addresses energy efficiency, which is linked to thermal comfort, and resilience which helps homeowners and residents prepare for natural disasters and ensures that a building continues to provide a healthy home.

As wellness continues to shape home design, both buyers and builders are prioritizing features that promote health, relaxation and sustainability. From natural materials to curated wellness spaces, these elements not only enhance daily living but also add long-term value. By integrating thoughtful design choices, homeowners can create environments that support well-being, efficiency, and a deeper connection to their surroundings.

Cell| Sabrina 650.799.4333 |Susan 650.796.0654 | EMAIL | WEB| BLOG

We love what we do and would love to help you navigate your sale or purchase of Residential Real Estate. Please reach out for a personal consultation. Please enjoy our free resources below and get to know our team from our TESTIMONIALS.

Effective. Efficient. Responsive. The Caton Team 🏡

Got Real Estate Questions? The Caton Team is here to help.

We strive to be more than just Realtors – we are also your home resource. If you have any real estate questions, concerns, need a referral, or some guidance – we are here for you. Contact us at your convenience – we are but a call, text or click away!

The Caton Team believes, in order to be successful in the San Fransisco | Peninsula | Bay Area | Silicon Valley Real Estate Market we have to think and act differently. We do this by positioning our clients in the strongest light, representing them with the utmost integrity, while strategically maneuvering through negotiations and contracts. Together we make dreams come true.

A mother and daughter-in-law team with over 35 years of combined, local Real Estate experience and knowledge – wouldn’t you like The Caton Team to represent you? Let us know how we can be of service. Contact us any time.

Cell | Sabrina 650.799.4333 | Susan 650.796.0654 | EMAIL | WEB| BLOG

The Caton Team – Susan & Sabrina A Family of Realtors Effective. Efficient. Responsive. What can we do for you?

Over a 14-month period starting in September, lenders are phasing in new appraisal reporting for all GSE-conforming loans. As appraisers adjust to the new standards, agents will be key partners in ensuring the data is accurate and complete. Learn more— and watch the latest “Supporting Your Value” appraisal webinar.

For a long time, appraisals for mortgage transactions have been reported in the same way—via a form designed for a typewriter. The form varies depending on property type, but each variation includes boxes to check and blank spaces to fill out.

Although appraisers have long completed forms using web-based platforms, these forms—required for loans conforming to government sponsored enterprise standards—are rigid in structure. Often, there isn’t enough space for the appraiser to provide all relevant information. In that case, the reader sees the dreaded, “See addendum.” At that point, the reader of the report will have to read through sometimes pages of freeform text to find what they are looking for.

Beginning in September 2025, all of this will change. Read on to learn more about the transition, and how appraisers and agents can work together to get through the transition.

Why Appraisals Are Changing

The new appraisal reporting structure, known as the Uniform Appraisal Dataset (UAD 3.6), was spearheaded by Fannie Mae and Freddie Mac under the direction of the Federal Housing Finance Agency. The initiative has been underway since 2018.

UAD 3.6 aligns appraisal data with current mortgage industry data standards. In addition, the new appraisal report allows for dynamic reporting of appraisal data and makes the information easier for readers to consume while increasing discrete data points that the GSEs can use for internal analysis.

Under this new structure, appraisal reports, regardless of property type, will have a standard front page that includes:

Property summary with the opinion of market value

Photo of the subject property

Property description

Appraisal type

The report will also feature much more detail upfront on the interior of the property, allowing appraisers to add descriptive commentary to go along with photos. Condition and quality will be broken out by exterior and interior, with areas for description of interior details.

The dynamic form expands as needed to include additional information. For instance, if the appraiser indicates there’s an accessory dwelling unit, a section will appear for the appraiser to provide details. If there is no ADU, however, that section will not appear. (Here are some sample scenarios to show you what the new reports will look like. The Single Family Scenario 5 beginning on page 271 contains key characteristics that appear often in residential appraisals.)

Appraisers across the country are preparing for the change, but it won’t be easy. That’s why the GSEs have allowed a 14-month rollout period. During that time, all appraisal software used for mortgage transactions is changing to accommodate the new report. Appraisers must consider whether their existing provider or a competitor best meets their needs.

In addition, UAD 3.6 also has many new discrete datapoints that appraisers must relay—and this highlights the importance of the appraiser-agent relationship. Any relevant information agents can provide upfront will help appraisers complete the appraisal in a timely manner and prevent the need for a return trip the property or other delays.

Take a Deeper Dive into UAD 3.6

The UAD 3.6 will bring big change—from the datapoints appraisers are required to provide to the way appraisal results are reported. Appraisal forms for individual property types will be a thing of the past for most appraisals. Some lenders will begin using the new UAD as early as September 2025. Use of the form will be required for all Fannie Mae and Freddie Mac loans as of November 2026.

How can you get up to speed? As part of NAR’s “Supporting Your Value” webinar series, speakers from Fannie Mae and Freddie Mac recently gave NAR members a rundown of why the UAD is being updated, showed examples of data required and what the new reporting look will look like, and provided resources to help agents and appraisers prepare for the transition. Hundreds of NAR members registered and attended the no-cost session, and you can now watch a recording of the April 29 webinar, “The New Uniform Appraisal Dataset: What REALTORS® Need to Know.”

Cell| Sabrina 650.799.4333 |Susan 650.796.0654 | EMAIL | WEB| BLOG

We love what we do and would love to help you navigate your sale or purchase of Residential Real Estate. Please reach out for a personal consultation. Please enjoy our free resources below and get to know our team from our TESTIMONIALS.

Effective. Efficient. Responsive. The Caton Team 🏡

Got Real Estate Questions? The Caton Team is here to help.

We strive to be more than just Realtors – we are also your home resource. If you have any real estate questions, concerns, need a referral, or some guidance – we are here for you. Contact us at your convenience – we are but a call, text, or click away!

The Caton Team believes, in order to be successful in the San Francisco | Peninsula | Bay Area | Silicon Valley Real Estate Market, we have to think and act differently. We do this by positioning our clients in the strongest light, representing them with the utmost integrity, while strategically maneuvering through negotiations and contracts. Together we make dreams come true.

A mother and daughter-in-law team with over 35 years of combined local Real Estate experience and knowledge – wouldn’t you like The Caton Team to represent you? Let us know how we can be of service. Contact us any time.

Cell | Sabrina 650.799.4333 | Susan 650.796.0654 | EMAIL | WEB| BLOG

The Caton Team – Susan & Sabrina A Family of Realtors Effective. Efficient. Responsive. What can we do for you?

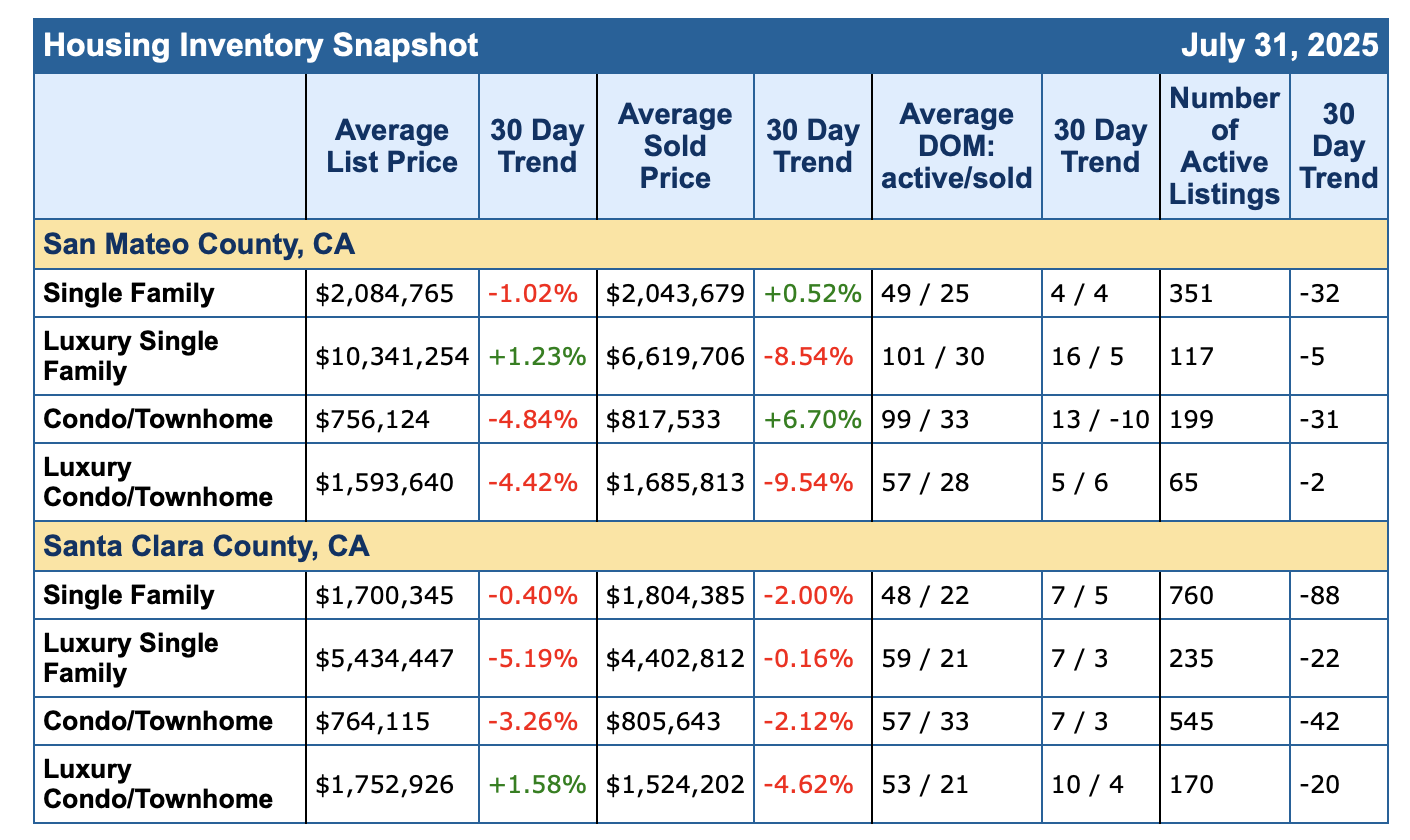

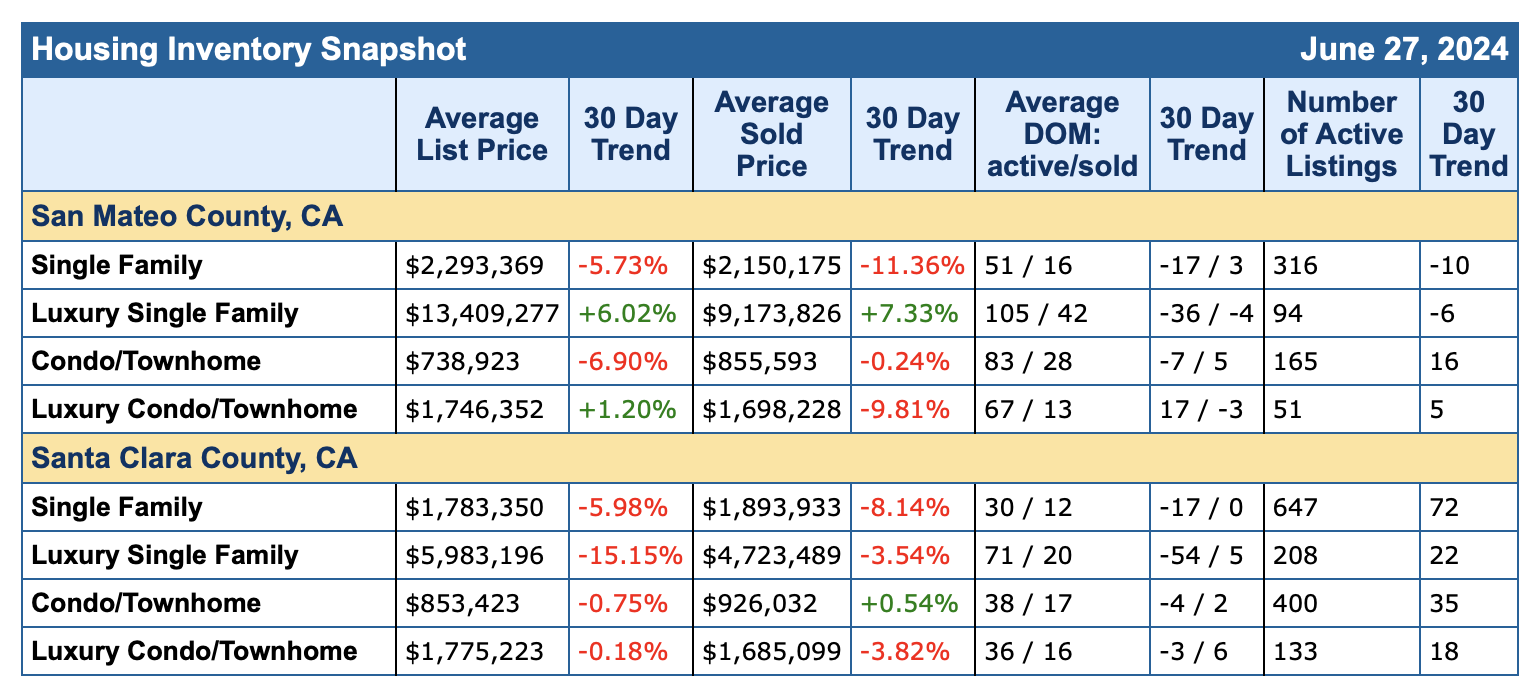

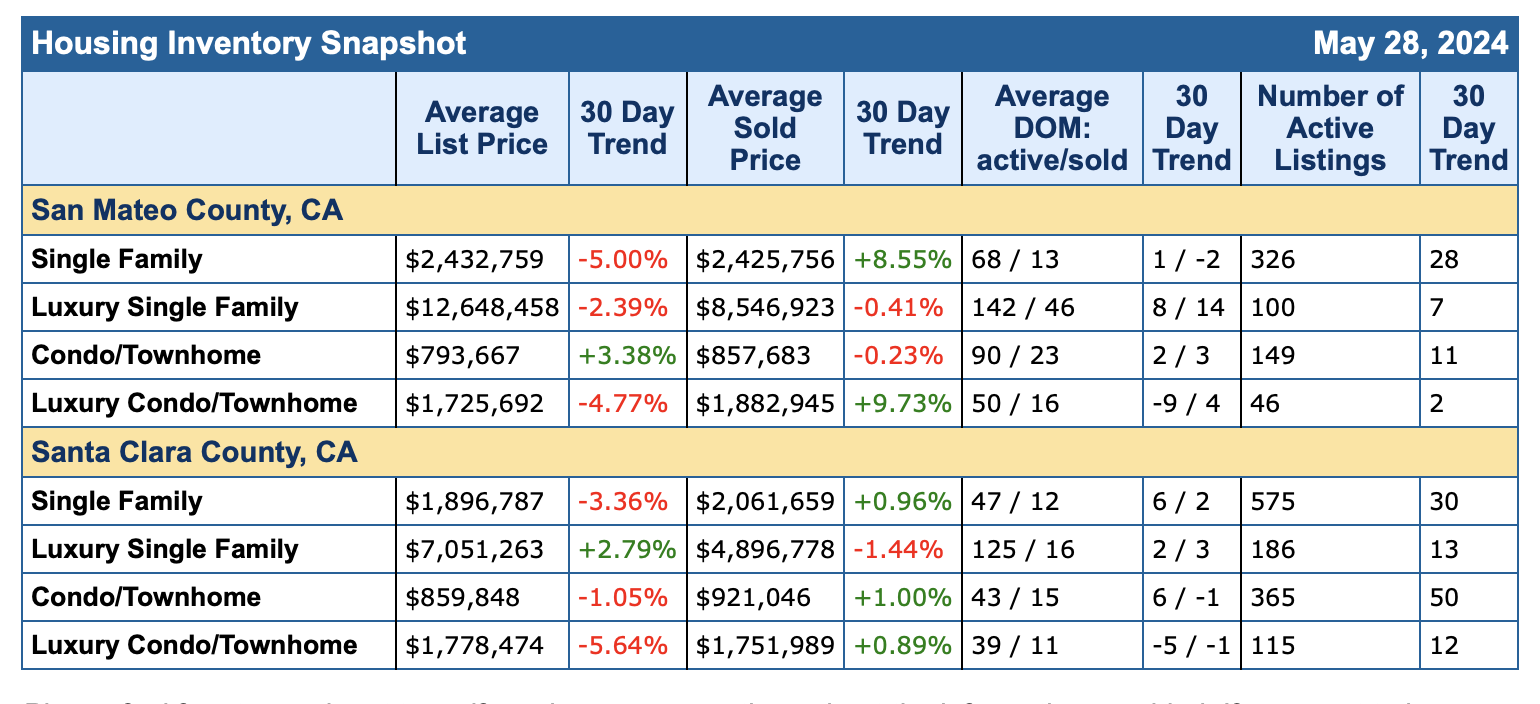

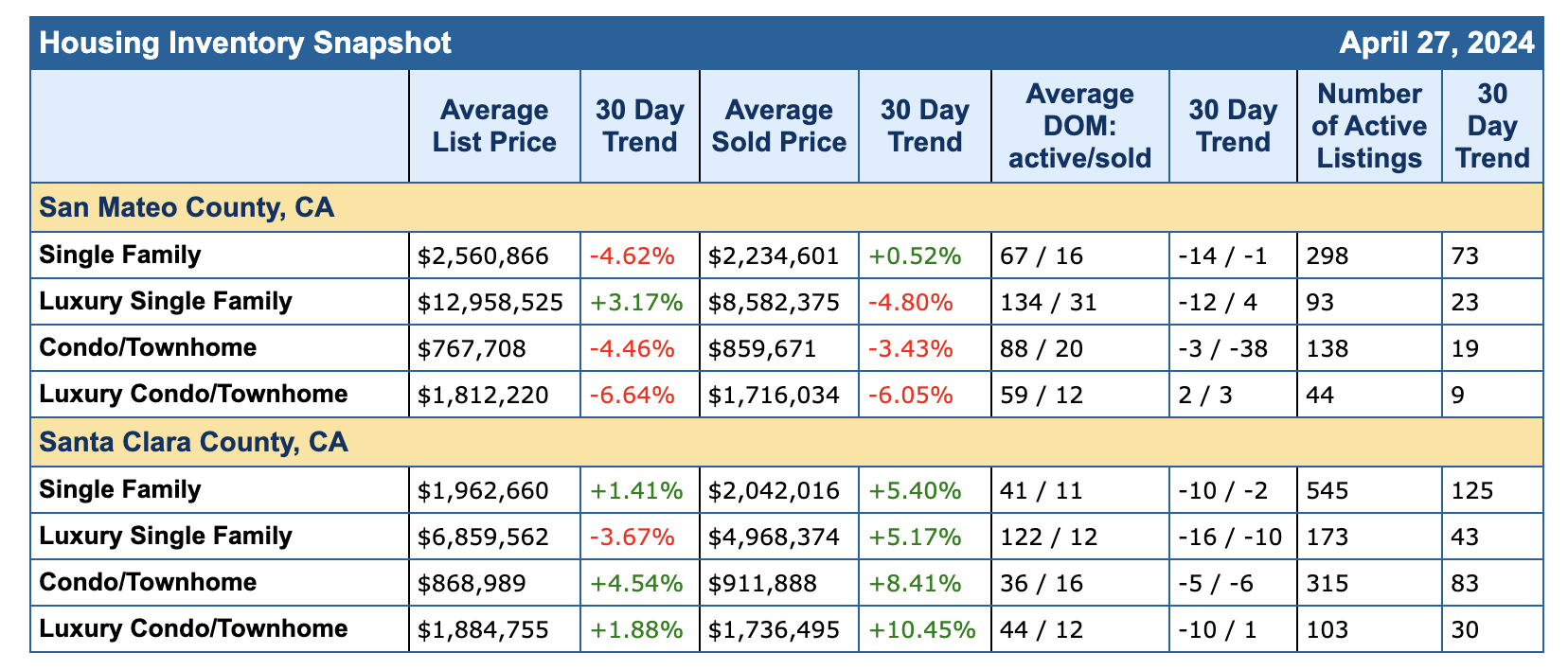

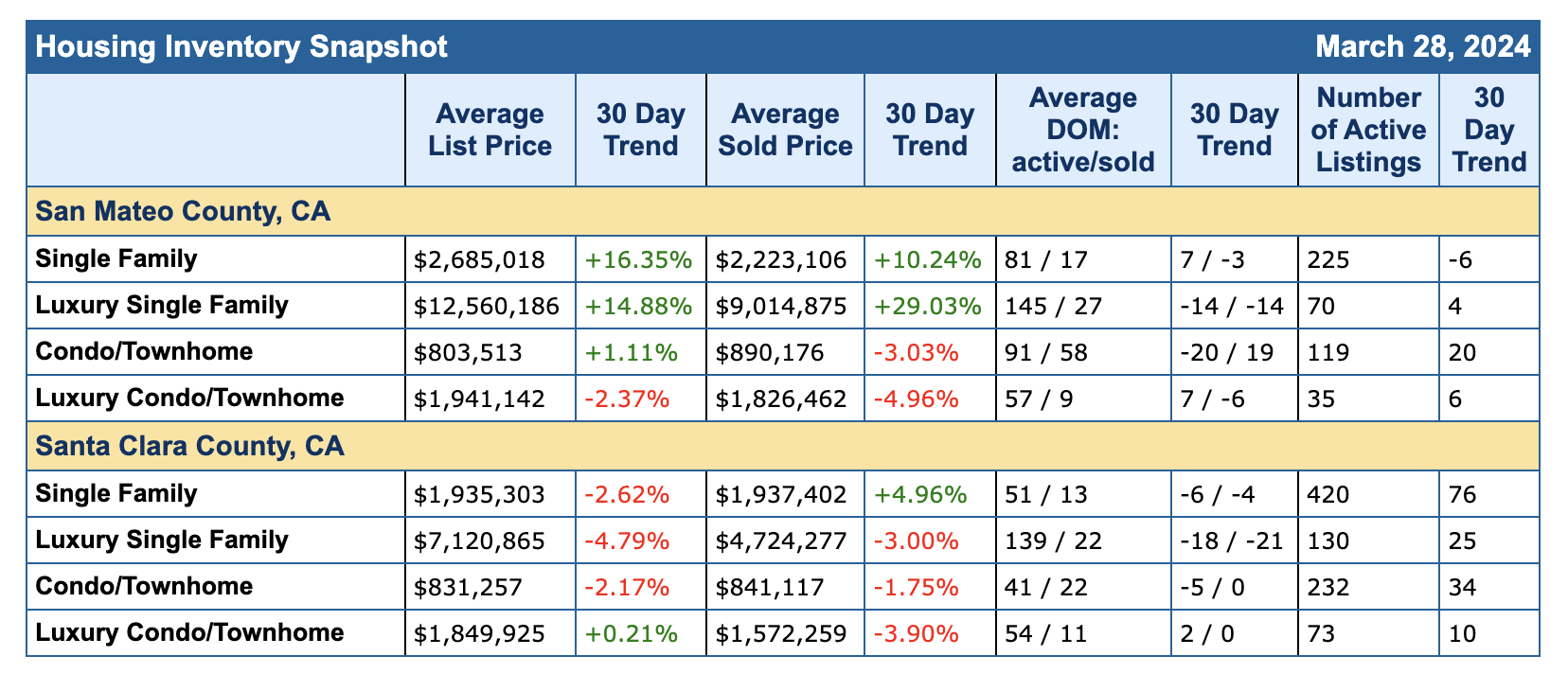

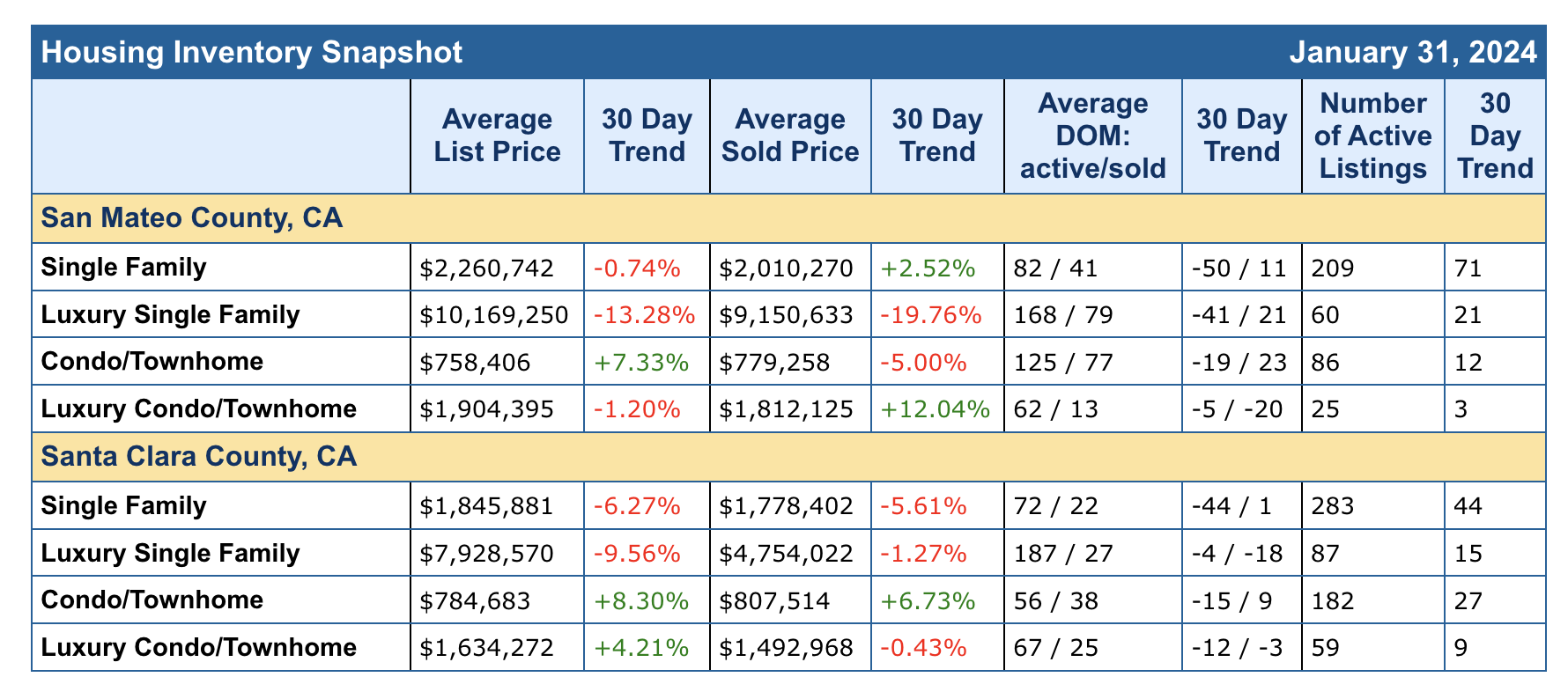

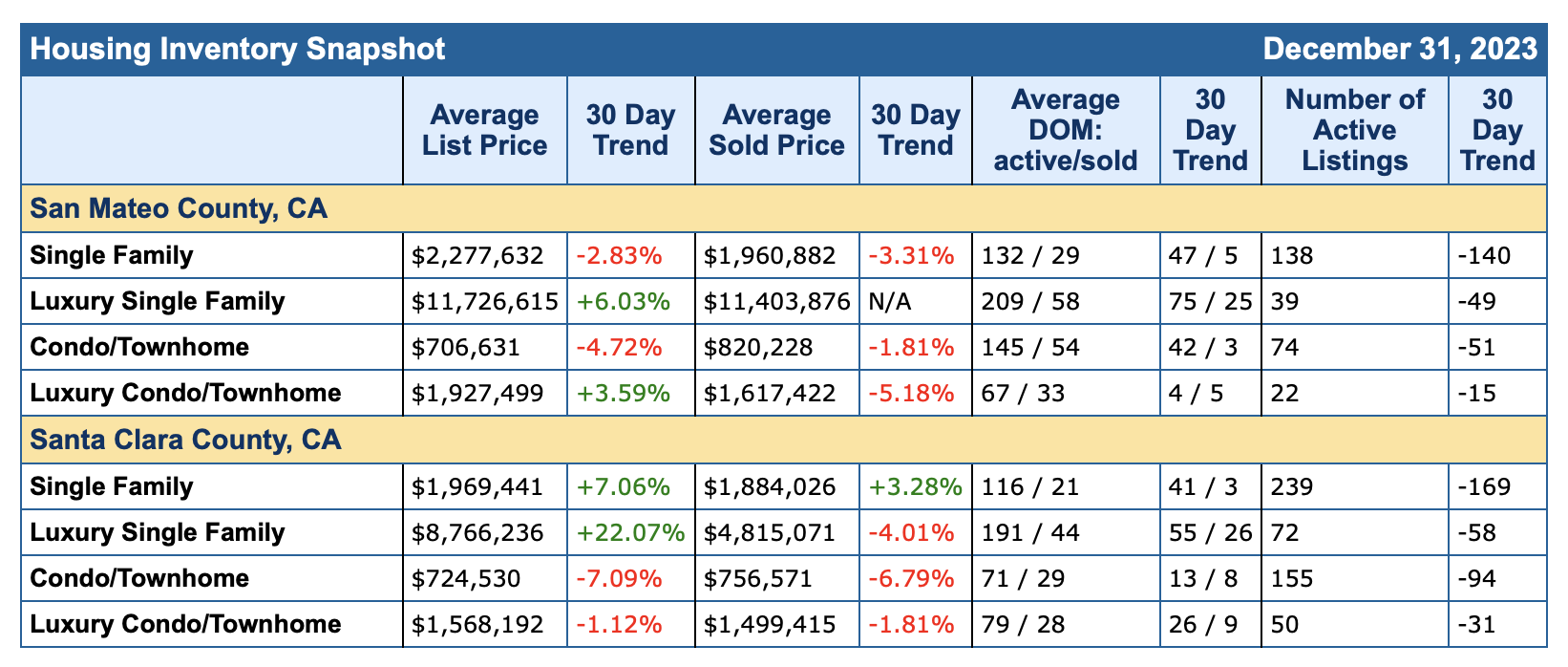

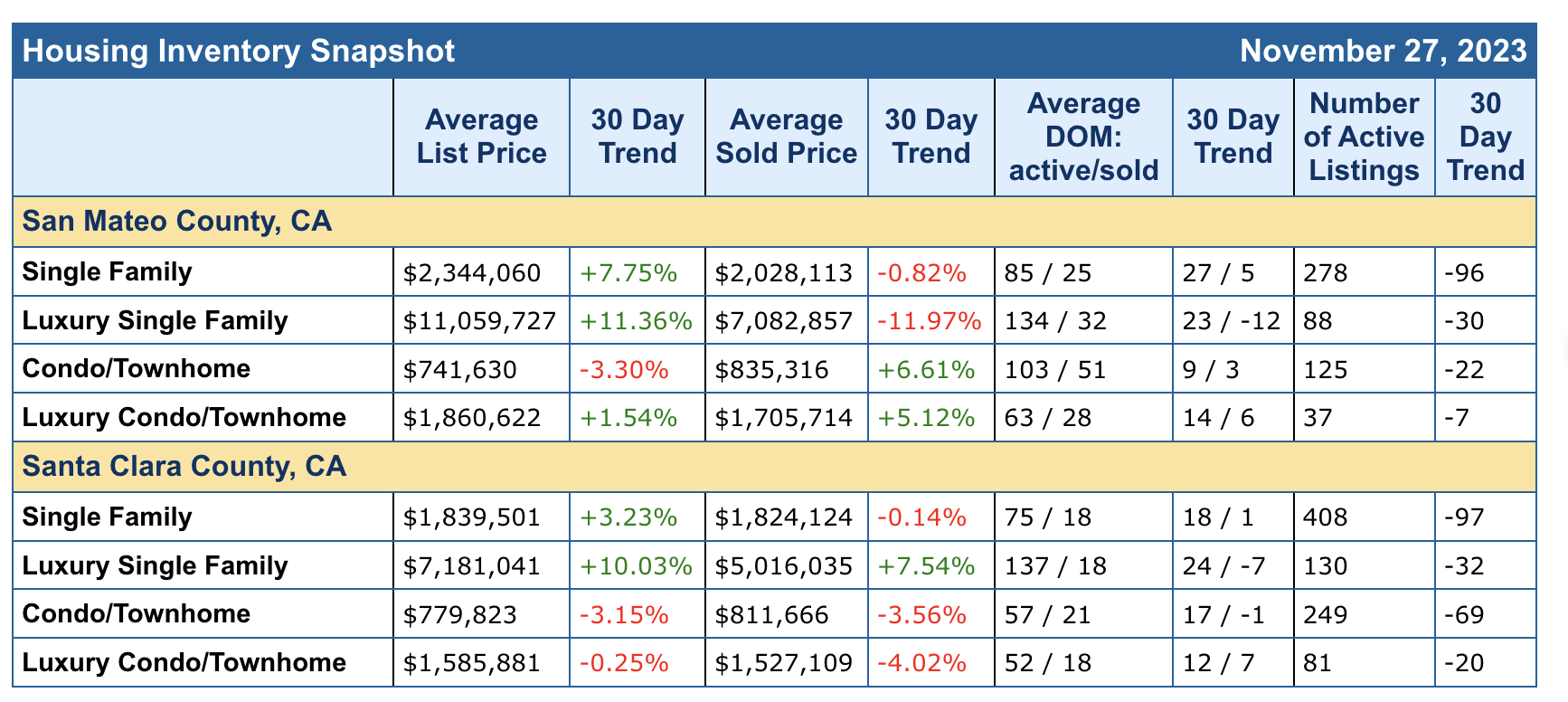

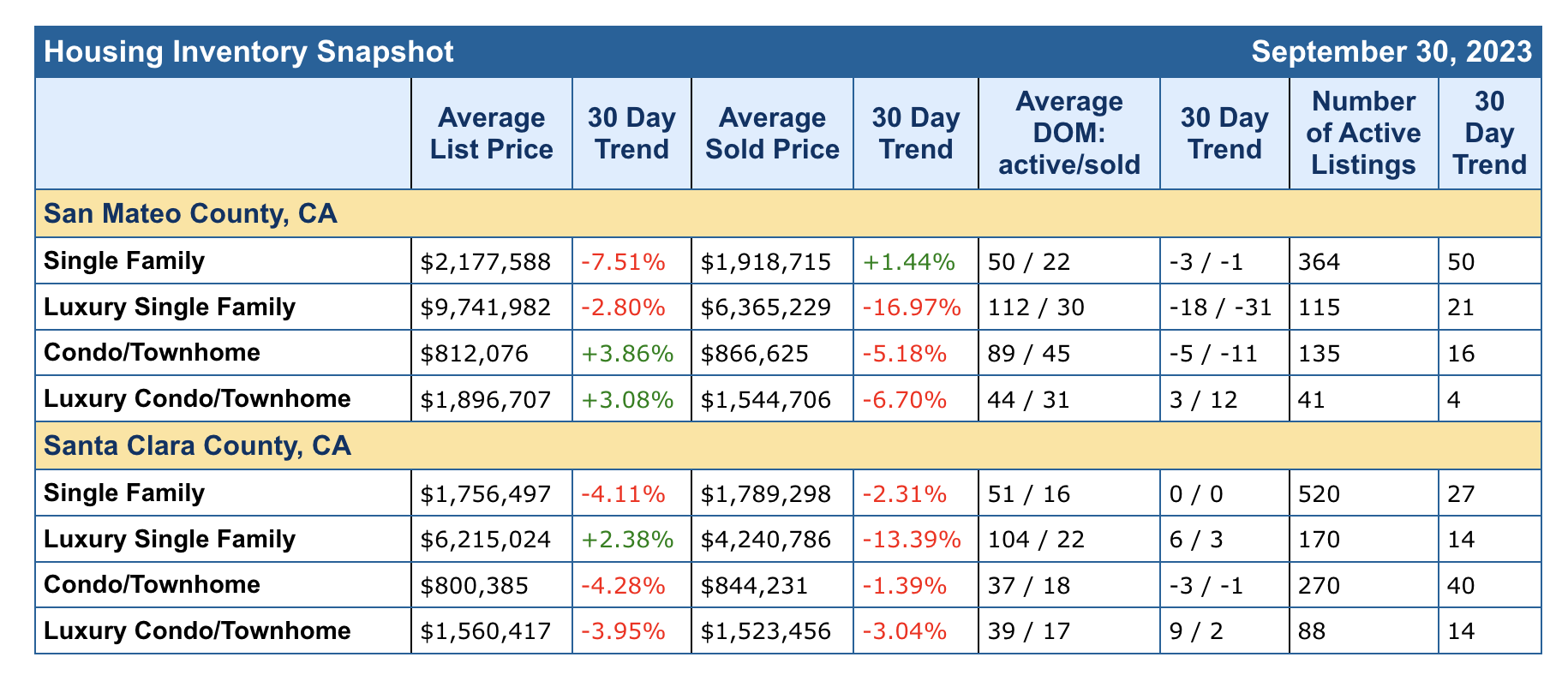

The stats are in for July 2025. The last 30 days reflect a softening of the market with values adjusting down. This is part of the normal summer slowdown as folks are off on vacation before summer ends. However, this whole year hits different from the year past. Job changes, market insecurity, and tariffs have many people on the fence about their next move, and who can blame them? However, in my gut, I know this: if you want to live and stay in the Bay Area, the best time to buy is during a weird market. Why, you ask? Well, in our “normal” market, which is characterized by low inventory and high demand, most buyers face multiple offers and often experience huge overbidding. When the market is weird, when other buyers are on the fence, we see opportunity. A home can only be sold once, so when multiple bids are the norm, folks get priced out pretty quickly. This year, not a day goes by that I don’t see a price adjustment down, meaning there is a gap between what sellers want/expect and what buyers can afford. Those interest rates changed things.

Now is a great time to buy – even sell. Not every property has a price adjustment. We sold a 100+ year home this year, over list price with multiple offers.

For my buyers, some homes are garnering multiple offers, but some are overlooked. With a little legwork, a buyer can truly find some great opportunities when they align with the market.

If you’re considering a Real Estate move, contact The Caton Team for a free consultation. With over 40 years of combined Real Estate experience, we have the knowledge and know-how to guide you to your goal. Call us at 650.799.4333 or email us at info@TheCatonTeam.com.

Whether you are selling or buying – today or tomorrow – contact The Caton Team – we’re happy to help you achieve your Real Estate goals.

Effective. Efficient. Responsive. The Caton Team 🏡

Each market is unique and with over 40 years of combined Real Estate experience, The Caton Team is more than happy to be of service if and when you are considering a move. Contact us anytime during your journey, together we’ll help you achieve your Real Estate goals.

Got Questions? The Caton Team is here to help.

Call| Text | Sabrina 650.799.4333 |EMAIL | WEB| BLOG

We love what we do and would love to help you navigate your sale or purchase of Residential Real Estate. Please reach out for a personal consultation. Please enjoy our free resources below and get to know our team TESTIMONIALS.

Got Real Estate Questions? The Caton Team is here to help.

We strive to be more than just Realtors – we are also your home resource. If you have any real estate questions, concerns, need a referral, or need some guidance – we are here for you. Contact us at your convenience – we are but a call, text or click away!

The Caton Team believes, in order to be successful in the San Fransisco | Peninsula | Bay Area | Silicon Valley Real Estate Market we have to think and act differently. We do this by positioning our clients in the strongest light, representing them with the utmost integrity, while strategically maneuvering through negotiations and contracts. Together we make dreams come true.

A mother and daughter-in-law team with over 35 years of combined, local Real Estate experience and knowledge – wouldn’t you like The Caton Team to represent you? Let us know how we can be of service. Contact us any time.

Call| Text | Sabrina 650.799.4333 | Susan 650.796.0654 |EMAIL | WEB| BLOG

The Caton Team – Susan & Sabrina A Family of Realtors Effective. Efficient. Responsive. What can we do for you?

Save your cash for more important things, like, you know, your mortgage.

You can’t swing a tool belt without hitting a website or TV network offering tips on taking care of your digs. Save money by watering your lawn at night! No, water it in the morning! No, dig up your lawn and replace it with a drought-hardy meadow!

Throw in the info you pick up from well-meaning friends, and there’s a sea of home care truisms out there, some of which can sink your budget.

Myth 1: Stone Countertops Are Indestructible

Fact: Even rock can be damaged.

Marble, quartz, travertine, soapstone, and limestone can all pick up stains. Regular household cleaners can dull their surfaces over time. And marble is maddeningly fragile — it’s the prima donna of stone.

Marble is easy to scratch and stain. Here’s the worst part: Mildly acidic substances — like soda, coffee, lemon juice, even hard water — will eat into marble, creating a cloudy, dull spot in a process known as etching.

“Spill a glass of wine on a marble counter and go to bed without cleaning it. The next morning you’ll have a problem,” says Louwrens Mulder, owner of Stone World in Knoxville, Tenn.

And while stone counters won’t crack under a hot pot, such direct heat can discolor quartz or marble, says Mulder. So be nice to your counters, no matter what they’re made of. And note that the best rock for your buck is granite. “It doesn’t stain or scratch. It’s tough because it’s volcanic rock,” Mulder says. Which means it can stand up to all the merlot and barbecue sauce you can spill on it.

Myth 2: Your Smoke Detector’s Test Button Is Foolproof

Fact: The test button doesn’t tell you what you really need to know.

Yes, check your smoke detector twice a year. But all that test button will tell you is whether the alarm sound is working, not if the sensor that detects smoke is working. Pretty key difference there.

The best way to check your device is with real smoke. Light a long, wooden match; blow it out; and hold it near the unit. If the smoke sets off the alarm, it’s working. If the smoke doesn’t set off the alarm, replace the batteries. If the smoke detector still doesn’t work after that, you need a new one. And replace those batteries once a year anyway, because dead batteries are the No. 1 reason smoke detectors fail.

Myth 3: Gutter Guards Are Maintenance-Free

Fact: You gotta clean gutter guards, too.

Gutter guards keep out leaves, but small debris like seeds, pine straw, and flower buds will still get through.

Gutter guards can lessen your work, though — sometimes a lot. Instead of shoveling out wheelbarrow loads of leaves and other debris twice a year, you might just need to clean gutters every two years. But if there are lots of trees in your yard, once a year might be necessary.

Related: Money-Saving Tips to Repair Those Dastardly Gutters

Myth 4: A Lemon Is a Great Way to Clean a Disposal

Fact: While wanting to use natural cleaners is admirable, most of them will damage your disposal and pipes over time.

The lemon’s acidic juice will corrode the metal parts of your disposal. The mixture of salt and ice contains metal-eating acid, too. The coffee grounds are abrasive enough to clean the gunk off the blades and make it smell like a cup of Americano, but they’ll accumulate in pipes and clog them.

The best natural cleaner for your disposal is good old baking soda. It’s mildly abrasive, so it will clean the blades. But it’s a base, not an acid, and won’t damage the metal. Best of all, a box with enough baking soda big enough to clean your disposal twice costs about a buck.

Myth 5: Mowing Your Lawn Super Short Means You’ll Mow Less Often

Fact: You might not have to mow as often, but your lawn will look like awful.

Cut that grass under an inch high, and you’ll never have to mow again because your grass will die. Mowing a lawn down to the root — a screwup known as scalping — is like cutting all the leaves off a plant.

Grass blades make and store your lawn’s energy. Removing more than a third of the length of the blade will leave your grass too weak to withstand weeds and pests. It also exposes the roots to the sun, causing the lawn to dry out quickly. Leave one to three inches of grass above the roots to keep your lawn lush.

Myth 6: The More Insulation in My Home, the Better

Fact: Too much of a good thing can actually cause problems.

You want enough attic insulation to keep heat from escaping from your home. But overloading your attic with insulation can create problems rather than solving them. It can compress the lower layers, making the insulation less effective, according to National Property Inspections. Plus, you could block your eaves or soffit ventilation, resulting in moisture buildup and even mold, warns the NPI. And no one wants that.

Energy Star offers guidance on how much attic insulation is enough.

Myth 7: A Trendy Kitchen Redo Will Increase My Home’s Value

Fact: Décor trends come and go as fast as viral videos.

Remember those Tuscan-style kitchens with mustard gold walls, ornate cabinets, and medieval-looking light fixtures that were the must-have of the late ’90s and early aughts?

Today, they’re as dated as flip phones. Instead of remodeling, try repainting in on-trend colors. The cost difference is significant. A kitchen upgrade costs an average $45,000, according the the National Association of REALTORS® “Remodeling Impact Report,” but repainting costs $400 to $1,200, according to FixR. If you do opt for a full remodel, choose elements like Shaker cabinets, wood floors, and subway tile, a timeless style you’ll love 10 years from now.

Related: 7 Bad Habits Homeowners Need to Quit Now

Myth 8: A Contractor Recommendation from a Friend Is Good Enough

Fact: Good contractors have more than just your buddy to vouch for them.

Your neighbor’s rec is a good start, but talk to a couple of sources before you hire anyone. Check the contractor’s reviews on Angie’s List or other online rating sites.

Ask a local building inspector which contractors meet code on the properties they inspect. Ask the contractor for the names of past clients you can talk to, how many other projects they have going, how long they’ve worked with their subcontractors, and if they routinely do projects the size of yours.

Look at this as a job interview where the contractor is an applicant and you’re the hiring manager. Make them show you they’re the one for the work.

Related: 5 Secrets Your Contractor Doesn’t Want You to Know

Myth 9: Turning Off Your AC When You Leave Saves Energy

Fact: Turning off the air conditioner when you leave could actually cost you money.

That’s because when you turn it back on, all your savings will be lost as the unit works overtime to cool your hot house. A better way to save on utilities is to turn the thermostat up or down (depending on the season) 5 to 10 degrees when you leave, says home improvement expert Danny Lipford.

And the best option? “Install a programmable thermostat,” he says. Even better, buy one you can control remotely with your smartphone and adjust the temperature before you get home. Because thermostats you have to touch are so 1998.

Myth 10: Permits? We Don’t Need No Stinkin’ Permits

Fact: You do.

Let’s say your neighbor’s brother-in-law, Cecil, is an electrician. Cecil can rewire your kitchen in a weekend because he won’t inconvenience you with a permit. Should you hire Cecil? No. Building codes protect you. From Cecil. Getting a permit means an inspector will check Cecil’s work to make sure he didn’t screw up.

Plus, if your house burns down in an electrical fire and your insurance company finds out the work was done without a permit, it won’t cover your loss. Check with your local planning or building department to find out if your project needs a permit. If it does, get one.

Cell| Sabrina 650.799.4333 |Susan 650.796.0654 | EMAIL | WEB| BLOG

We love what we do and would love to help you navigate your sale or purchase of Residential Real Estate. Please reach out for a personal consultation. Please enjoy our free resources below and get to know our team from our TESTIMONIALS.

Effective. Efficient. Responsive. The Caton Team 🏡

Got Real Estate Questions? The Caton Team is here to help.

We strive to be more than just Realtors – we are also your home resource. If you have any real estate questions, concerns, need a referral, or some guidance – we are here for you. Contact us at your convenience – we are but a call, text or click away!

The Caton Team believes, in order to be successful in the San Fransisco | Peninsula | Bay Area | Silicon Valley Real Estate Market we have to think and act differently. We do this by positioning our clients in the strongest light, representing them with the utmost integrity, while strategically maneuvering through negotiations and contracts. Together we make dreams come true.

A mother and daughter-in-law team with over 35 years of combined, local Real Estate experience and knowledge – wouldn’t you like The Caton Team to represent you? Let us know how we can be of service. Contact us any time.

Cell | Sabrina 650.799.4333 | Susan 650.796.0654 | EMAIL | WEB| BLOG

The Caton Team – Susan & Sabrina A Family of Realtors Effective. Efficient. Responsive. What can we do for you?

Preparing and keeping a fully stocked home emergency preparedness kit could be the key to your family’s safety if disaster strikes.

Recent weather events have made homeowners get serious about having an up-to-date emergency kit. You may be at home without water or power or need to quickly evacuate. Either way, you’ll want to have the supplies you need ready to go. When you pack or update your emergency kit, you’ll need to factor in the type of event you might be dealing with and stock up accordingly. The following advice covers a basic kit as well as extra items you should have for a hurricane or storm surge, a winter storm, or an evacuation.

Basic Emergency Kit

Here are 15 basics recommended by the Red Cross:

Water: one gallon per person, per day (3-day supply for evacuation, 2-week supply for home)

Food: nonperishable, easy-to-prepare items (3-day supply for evacuation, 2-week supply for home)

Flashlight

Battery-powered or hand-crank radio (NOAA Weather Radio, if possible)

Extra batteries

First aid kit

Medications (7-day supply) and medical items

Multi-purpose tool

Sanitation and personal hygiene items

Copies of personal documents (medication list and pertinent medical information, proof of address, deed/lease to home, passports, birth certificates, insurance policies)

Cell phone with chargers

Family and emergency contact information

Extra cash

Emergency blanket

Maps of the area

Extra Emergency Supplies for a Hurricane or Storm Surge

Here are extra supplies and actions to take before a hurricane or a storm surge:

Gather your insurance information and check your coverage. Do this long before a storm strikes.

Take a photo inventory of your home.

Download the FEMA app to help you with preparations such as creating a family emergency communications plan. FEMA recommends including the same items as in a basic emergency kit.

Take a can opener.

Invest in a generator and make sure you have whatever gas or propane you need to power it. The size of the generator should be based on the amount of wattage you need to power the items you want. Even a small generator can be helpful for necessary appliances such as your cell phone, a CPAP machine, or a small refrigerator to keep medicines cold. If you’re on a limited budget, you can purchase a fairly inexpensive foldable solar panel to charge your phone and some lights.”

Use your electric car, if you have one, and a wall battery as a power source. And there are ways to run power through an inverter from your car battery and get power from your car to your home.

Extra Emergency Supplies for a Winter Storm

The Federal Emergency Management Agency recommends having these items on hand, especially if you want to prepare for being at home several days without power. This list includes items in addition to those listed in the basic kit.

Snow shovels: You’ll need more than one because they can break, and four hands are better than two

Deicers, preferably the pet-safe type: Some types of deicer that are more environmentally safe include calcium magnesium acetate and sand to improve traction. Stock up early in the season, because they become scarce before a well-publicized storm.

Wood: store a supply of dry, seasoned wood if you have a working fireplace or wood burning stove with a safe flue or vent, a full propane tank, or a generator.

Warm bedding and clothes: Clean blankets, pillows, and warm clothing (including hat and mittens) for everyone in the house in case you can’t do laundry for a while.

Build an emergency supply kit for your car including a first aid kit, jumper cables, a full tank of gas, a cell phone and charger, a shovel, an ice scraper, a snow brush, sand/cat litter, warm clothing and blanket, water and snacks, tire chains, tow rope, and flares.

Extra Emergency Supplies and Guidelines for an Evacuation

Here are guidelines and items beyond the basics in case you need to evacuate.

Keep copies of important papers in a plastic, waterproof case. FYI, this stuff is priceless, because you may need to prove who you are and that you own your house. Note that FEMA is now accepting more ways to verify home occupancy or ownership before providing certain types of assistance.

In addition to the documents listed for the basic emergency kit, Include:

Your driver’s license

Proof of insurance

Social Security cards

Take these ongoing or preliminary precautions as well:

Safeguard pets. Make sure they’re microchipped and have identification collars. Create pet grab-and-go kits that include leashes, medications, meal bowls, and three days’ worth of food and water.

Prep your yard. Maintain your trees and shrubs so diseased or weakened branches won’t fall down and damage your property.

Know your utility shutoffs. Learn now how to safely shut off all utility services in your home. FEMA has tips for shutting off electricity, water, and gas. Note: To turn off gas you may need a special wrench.

Stockpile sandbag materials. If you live in a flood prone area, keep sandbags on hand or the materials to make them. It takes 100 sandbags to create a 1-foot-tall wall that’s 20 feet long. If you’re filling bags on the fly, two adults can create the wall in about an hour.

Protect windows. If you live in an area susceptible to hurricanes, install shutters that are rated to provide protection from windblown debris.

Emergency Kit Storage Locations

Since you can’t predict where you’ll be during an emergency, it’s essential to have a well-prepared home kit:

Keep your emergency kit in a designated, easily accessible location and ensure it’s ready in case you need to leave your home quickly.

Make sure all family members know where the kit is stored.

Emergency Kit Maintenance

Update your kit as your needs change, and replace food and water approaching its expiration date. You might pick a specific time each year to check, such as before hurricane season in the south or after Thanksgiving if you live in the north.

Once you’ve put your kit together, it’s important to keep it in good condition so it’s available when necessary:

Store canned goods in a cool and dry location.

Keep boxed foods in airtight plastic or metal containers.

Regularly check and replace items that have expired.

Annually reassess your requirements and adjust your kit to accommodate any changes in your family’s needs.

Annually reassess your requirements and adjust your kit to accommodate any changes in your family’s needs.

Cell| Sabrina 650.799.4333 |Susan 650.796.0654 | EMAIL | WEB| BLOG

We love what we do and would love to help you navigate your sale or purchase of Residential Real Estate. Please reach out for a personal consultation. Please enjoy our free resources below and get to know our team from our TESTIMONIALS.

Effective. Efficient. Responsive. The Caton Team 🏡

Got Real Estate Questions? The Caton Team is here to help.

We strive to be more than just Realtors – we are also your home resource. If you have any real estate questions, concerns, need a referral, or some guidance – we are here for you. Contact us at your convenience – we are but a call, text or click away!

The Caton Team believes, in order to be successful in the San Fransisco | Peninsula | Bay Area | Silicon Valley Real Estate Market we have to think and act differently. We do this by positioning our clients in the strongest light, representing them with the utmost integrity, while strategically maneuvering through negotiations and contracts. Together we make dreams come true.

A mother and daughter-in-law team with over 35 years of combined, local Real Estate experience and knowledge – wouldn’t you like The Caton Team to represent you? Let us know how we can be of service. Contact us any time.

Cell | Sabrina 650.799.4333 | Susan 650.796.0654 | EMAIL | WEB| BLOG

The Caton Team – Susan & Sabrina A Family of Realtors Effective. Efficient. Responsive. What can we do for you?

There’s a lot you can do to visually expand your bathroom, without any physical renovations.

In an ideal world, your bathroom would be a spacious, spa-like retreat with a double vanity, a separate shower and tub, and ample storage for all your essentials. But in reality, your bathroom might just be a small, primarily functional space. But don’t worry—if expanding isn’t an option, you’re not entirely out of luck. With a few smart design tricks, you can create the illusion of a larger, more comfortable space. Here’s how to make a small bathroom look bigger, according to interior designers.

Replace That Shower Curtain With a Glass Door

Shower curtains cut off your bathroom, making the space appear smaller. So, swap it out and add a glass door instead. “A glass door instantly can add a few more square feet into the space visually,” says interior designer James Pearse Connelly. “Now you can see more of the room!” Don’t forget, however, that the more you can see, the more you need to keep tidy, he warns.

If you don’t have the budget to install a new shower door, you can, at the least, swap your opaque shower curtain for a transparent option that will still allow you to expand the space visually.

Reflect as Much Light as Possible

Another trick to making your bathroom look bigger is to reflect light. Connelly suggests using big mirrors, which means it’s time to replace that small, dated medicine cabinet with a much more substantial mirror.

Another way the designer advises reflecting light is to choose chrome hardware. “It will make the light dance around the room,” he says.

Go Monochromatic

Connelly recommends opting for either a very dark or very light color scheme in the bathroom to expand the space visually. “For instance, an all-white or an all-black bathroom can affect lighting differently and dramatically make the space look larger while taking the space to new dimensions,” he explains.

As for specific hues, the designer likes incorporating deep navy blues and dark burgundies, as well as ivories and creams. “These shades offer a sophisticated yet spacious feel,” he says.

When It Comes to Sinks, Less Is More

The sink and vanity can mean the difference between feeling like you’re in a crammed closet or not. Designer Shannon Askinasi of Ash and Pine Interiors says floating wood or marble vanities are always a great choice for small bathrooms.

“When you can see the floor below the vanity, it makes the room feel larger,” Askinasi says. “Pedestal sinks are also a space-saver, but they lack the storage potential of a floating vanity.”

Connelly also recommends keeping the sink proportional to the room. “If the room is small, keep the sink small,” he says. “I prefer to see as much floor as possible in small rooms.”

Install Patterned Wallpaper

While it’s a different approach than the monochromatic look Connelly suggests above, Askinasi is a big fan of installing vinyl wallpaper in smaller bathrooms. “I find that vertical stripes, chevrons, and large repeating patterns—with a lot of negative space—are the perfect way to make a small bathroom appear larger,” she says.

Don’t Be Afraid to Go Bold

“When designing a small bathroom, I always try to include a few design elements that pack a punch,” notes Askinasi. “Whether it’s a fluted vanity, a beautiful accent wall, interesting lighting, or all of the above, I give the eye multiple places to look in order to make a small space feel larger. I also like to include glass pendants or sconces in order to reflect light and create the illusion of depth.”

Keep Your Finishes Consistent Across All Surfaces

Connelly tells me it’s best to avoid emphasizing specific details, like the molding, ceilings, or flooring, and instead aim to create a cohesive look. “Let your floor tile come up on the wall,” he recommends. “Paint your ceiling the same color as the walls. Bring your countertop stone behind the mirror.”

Keep It Clutter-Free

While it’s necessary to have some items out, like a soap pump and perhaps a toothbrush, keeping out too many decorative items (and all your skincare products) is only going to make your bathroom look more cluttered and crammed.

Lastly, while you probably need a garbage can, it’s best to keep the plunger and toilet brush off the floor and stored away, out of sight.

Cell| Sabrina 650.799.4333 |Susan 650.796.0654 | EMAIL | WEB| BLOG

We love what we do and would love to help you navigate your sale or purchase of Residential Real Estate. Please reach out for a personal consultation. Please enjoy our free resources below and get to know our team from our TESTIMONIALS.

Effective. Efficient. Responsive. The Caton Team 🏡

Got Real Estate Questions? The Caton Team is here to help.

We strive to be more than just Realtors – we are also your home resource. If you have any real estate questions, concerns, need a referral, or some guidance – we are here for you. Contact us at your convenience – we are but a call, text or click away!

The Caton Team believes, in order to be successful in the San Fransisco | Peninsula | Bay Area | Silicon Valley Real Estate Market we have to think and act differently. We do this by positioning our clients in the strongest light, representing them with the utmost integrity, while strategically maneuvering through negotiations and contracts. Together we make dreams come true.

A mother and daughter-in-law team with over 35 years of combined, local Real Estate experience and knowledge – wouldn’t you like The Caton Team to represent you? Let us know how we can be of service. Contact us any time.

Cell | Sabrina 650.799.4333 | Susan 650.796.0654 | EMAIL | WEB| BLOG

The Caton Team – Susan & Sabrina A Family of Realtors Effective. Efficient. Responsive. What can we do for you?

You must be logged in to post a comment.