Hello Caton Team Blog Readers,

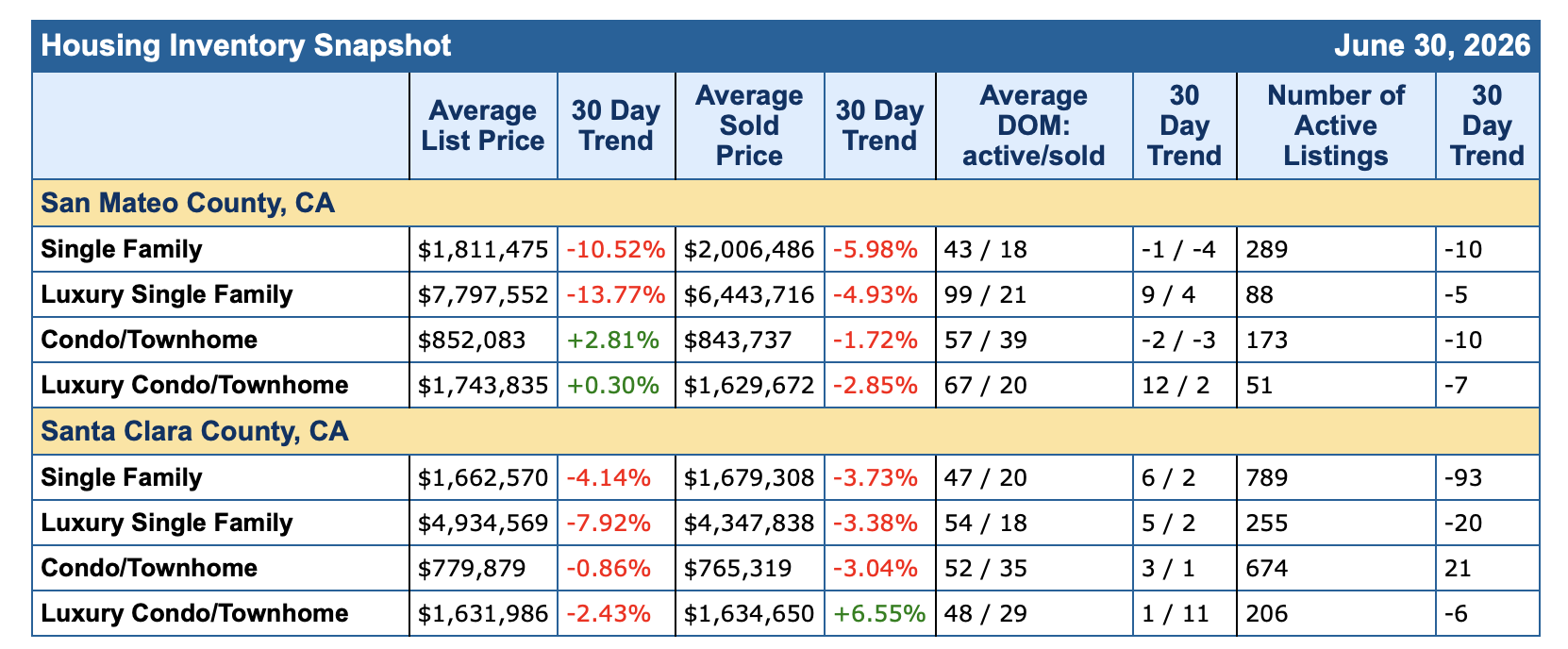

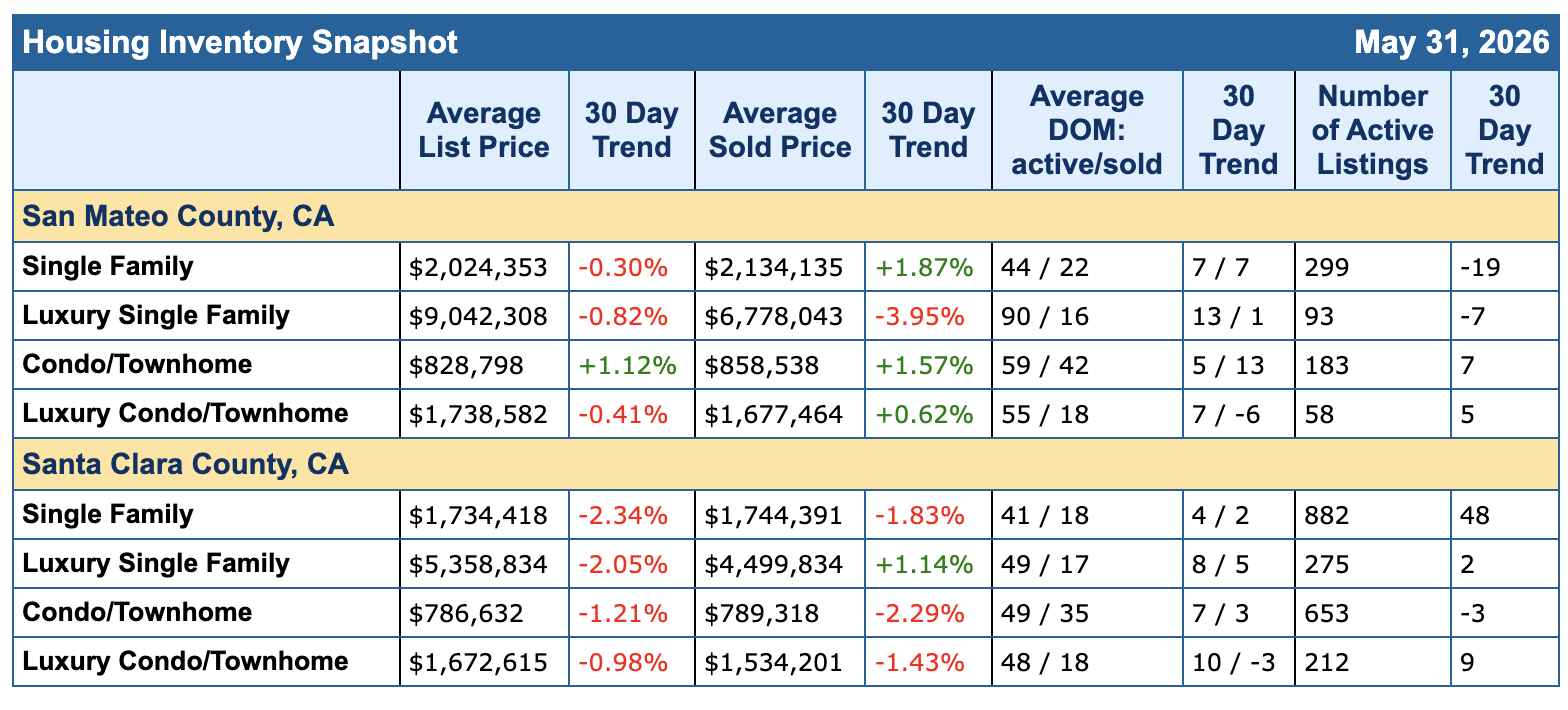

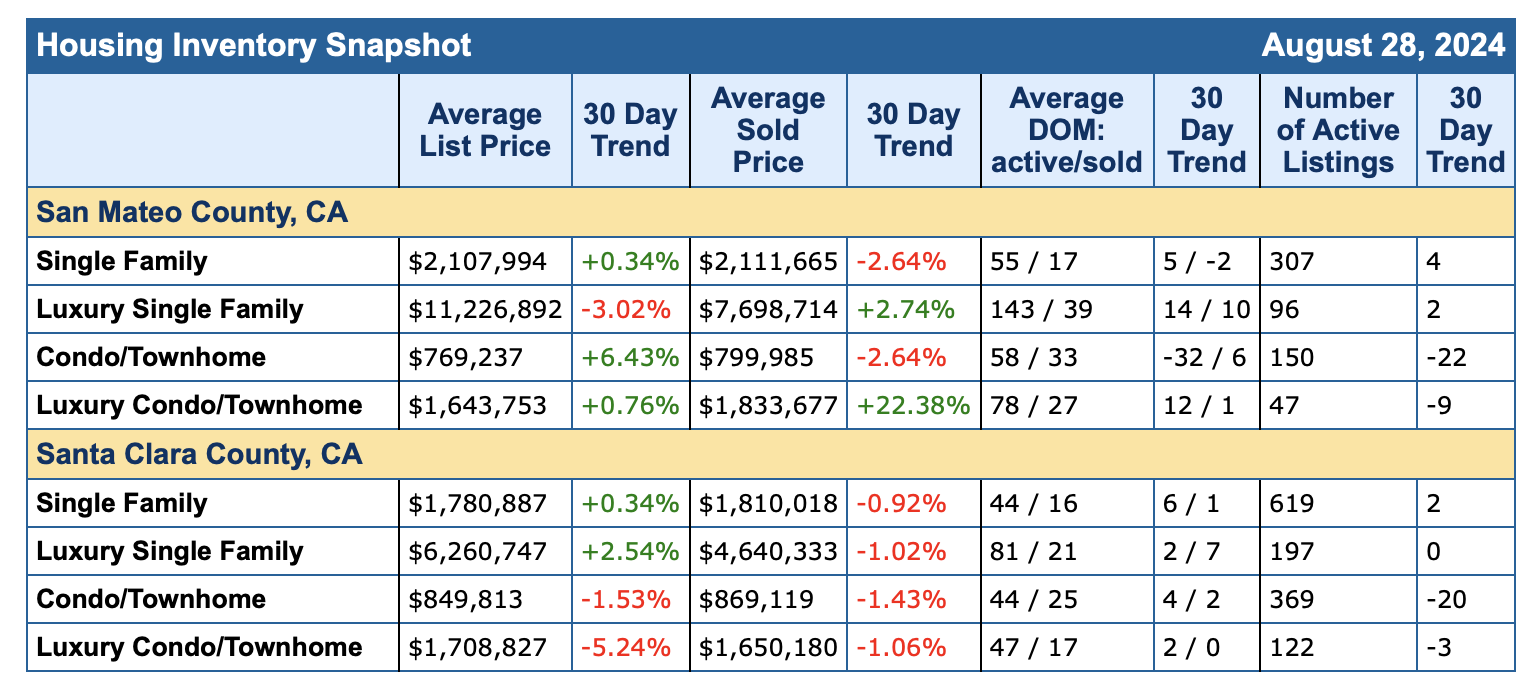

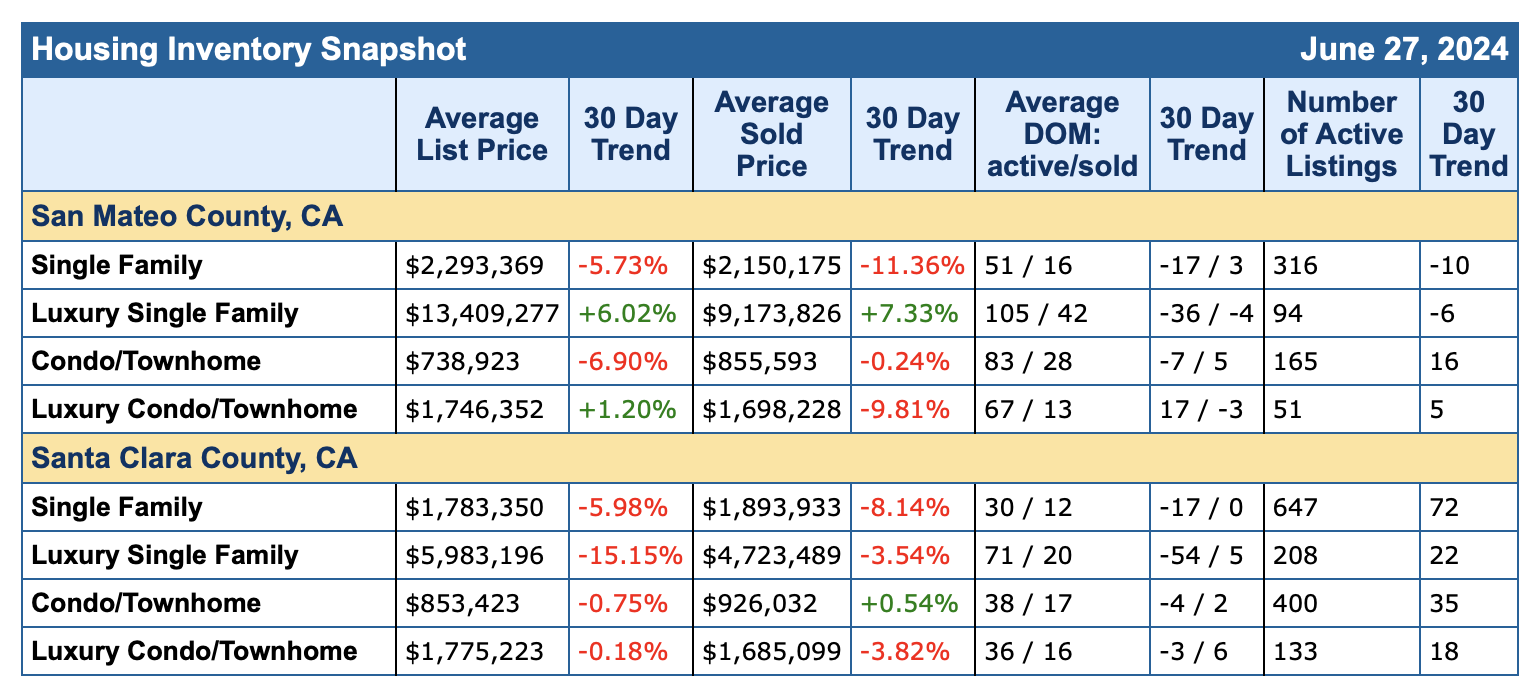

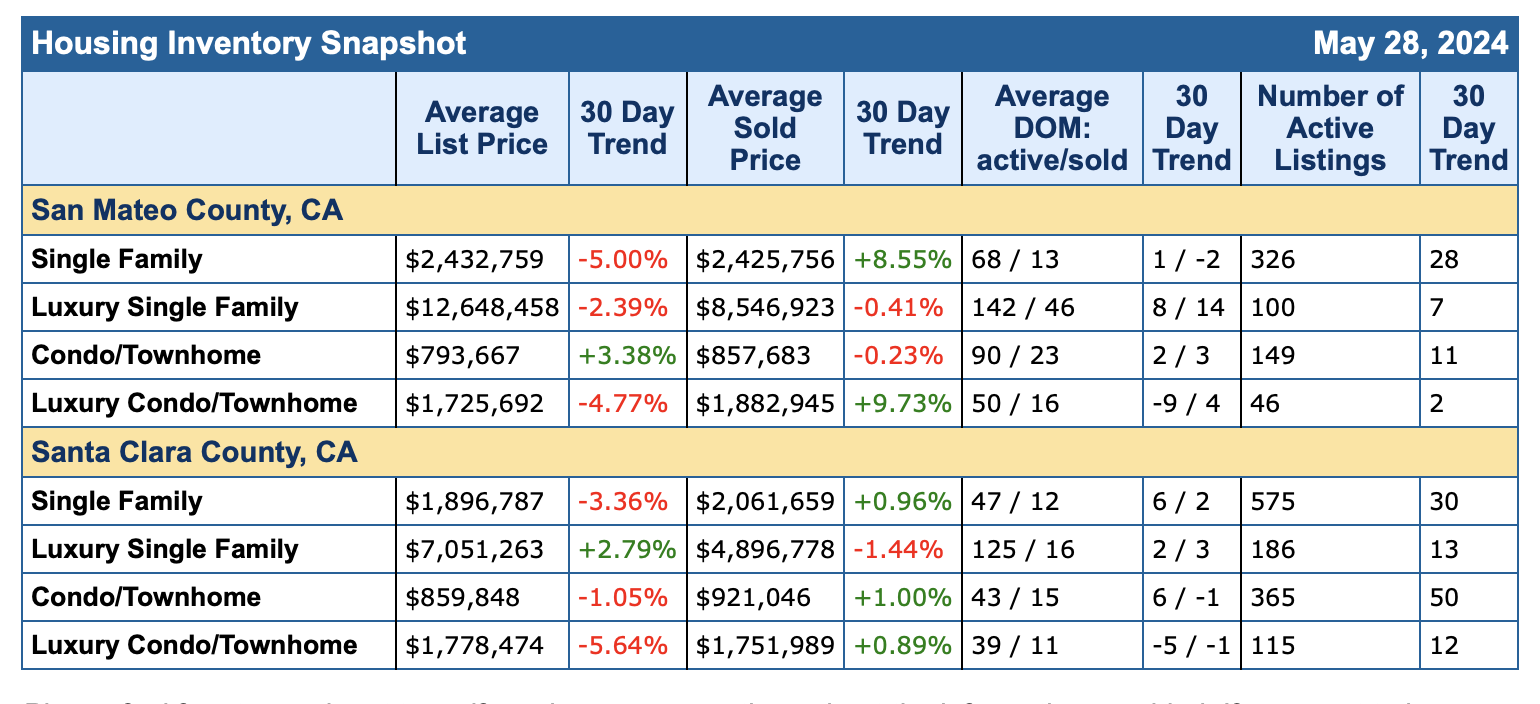

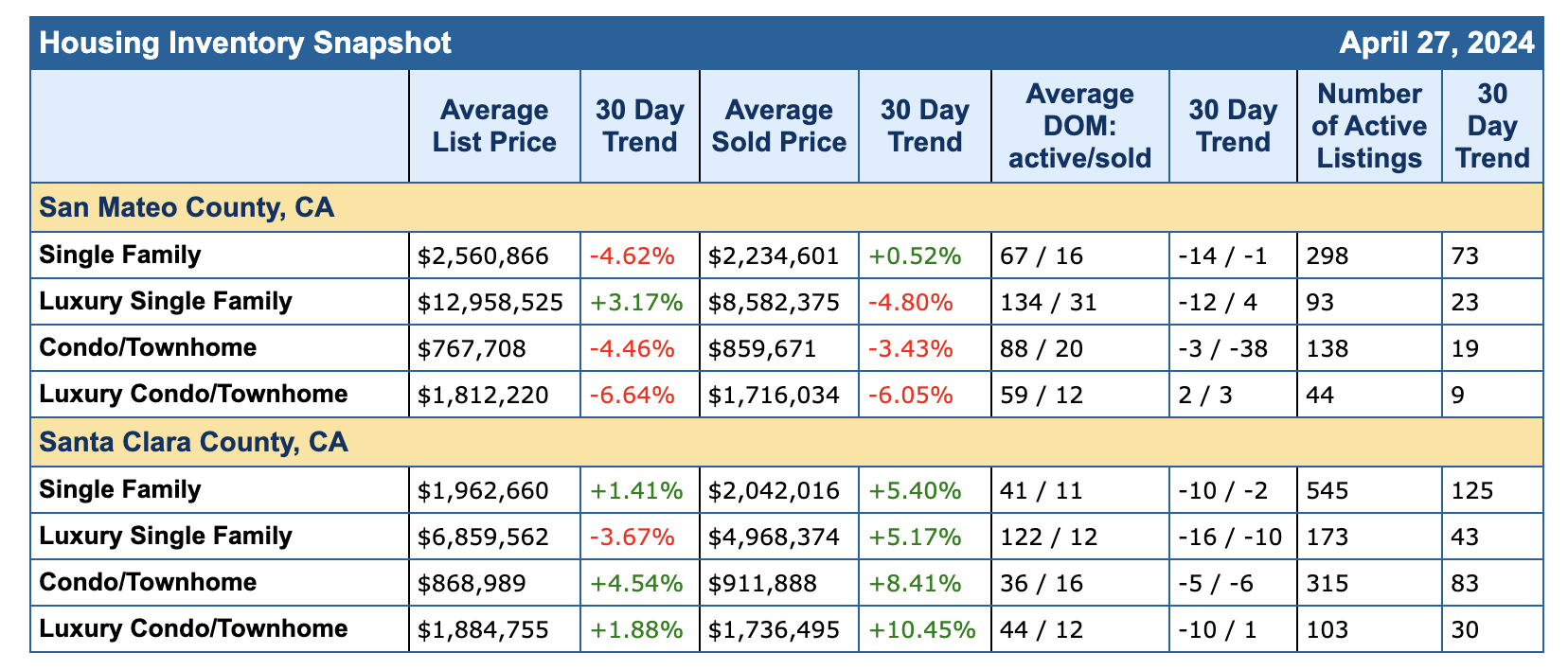

Thank you for tuning in. The stats are in for May and June 2026.

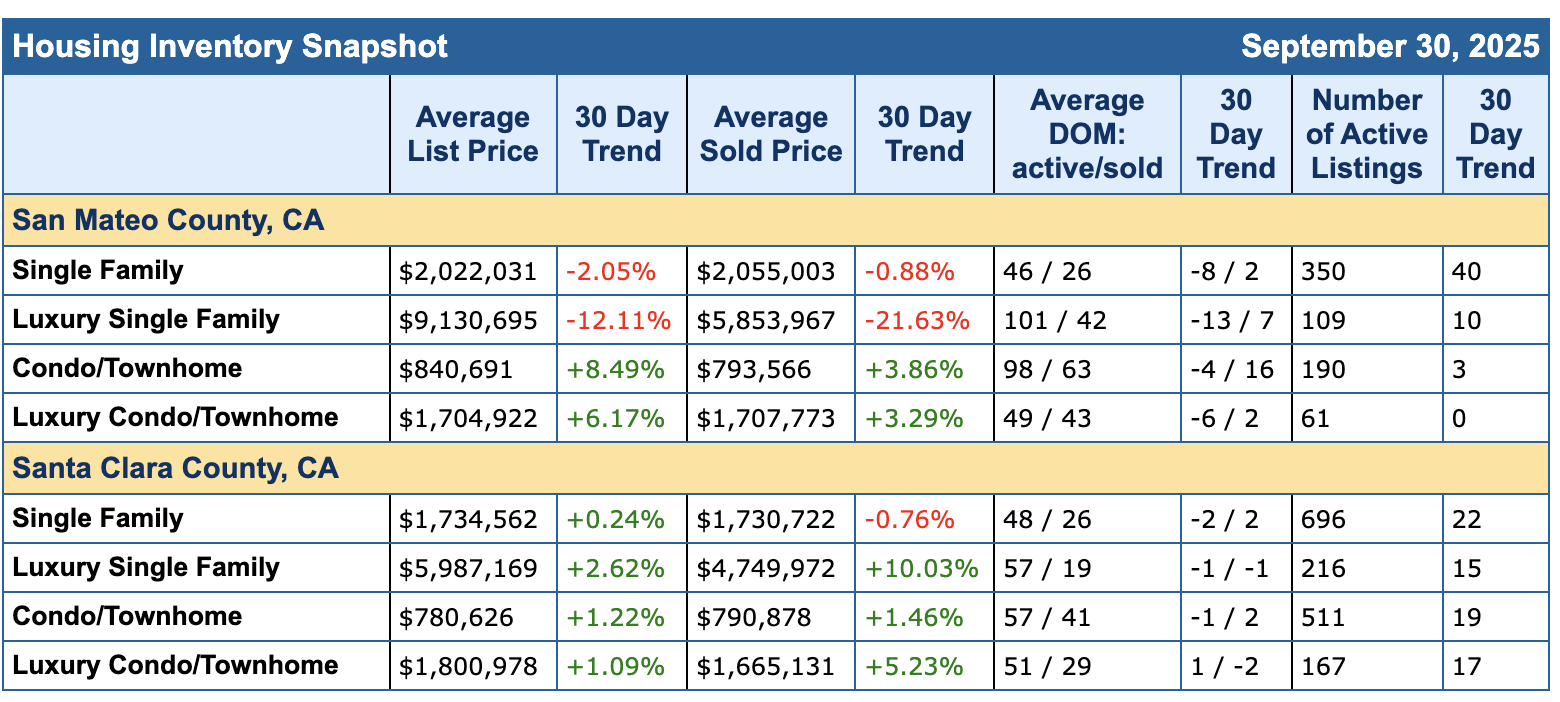

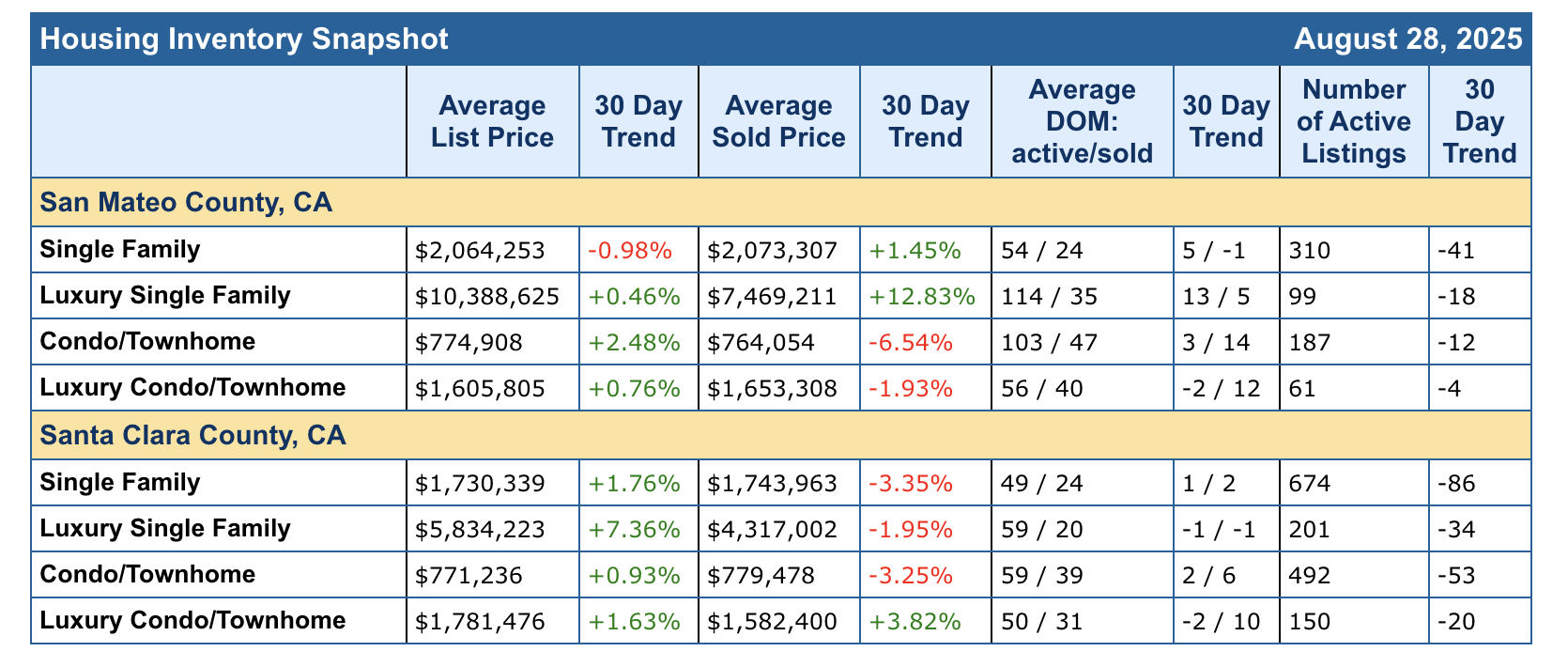

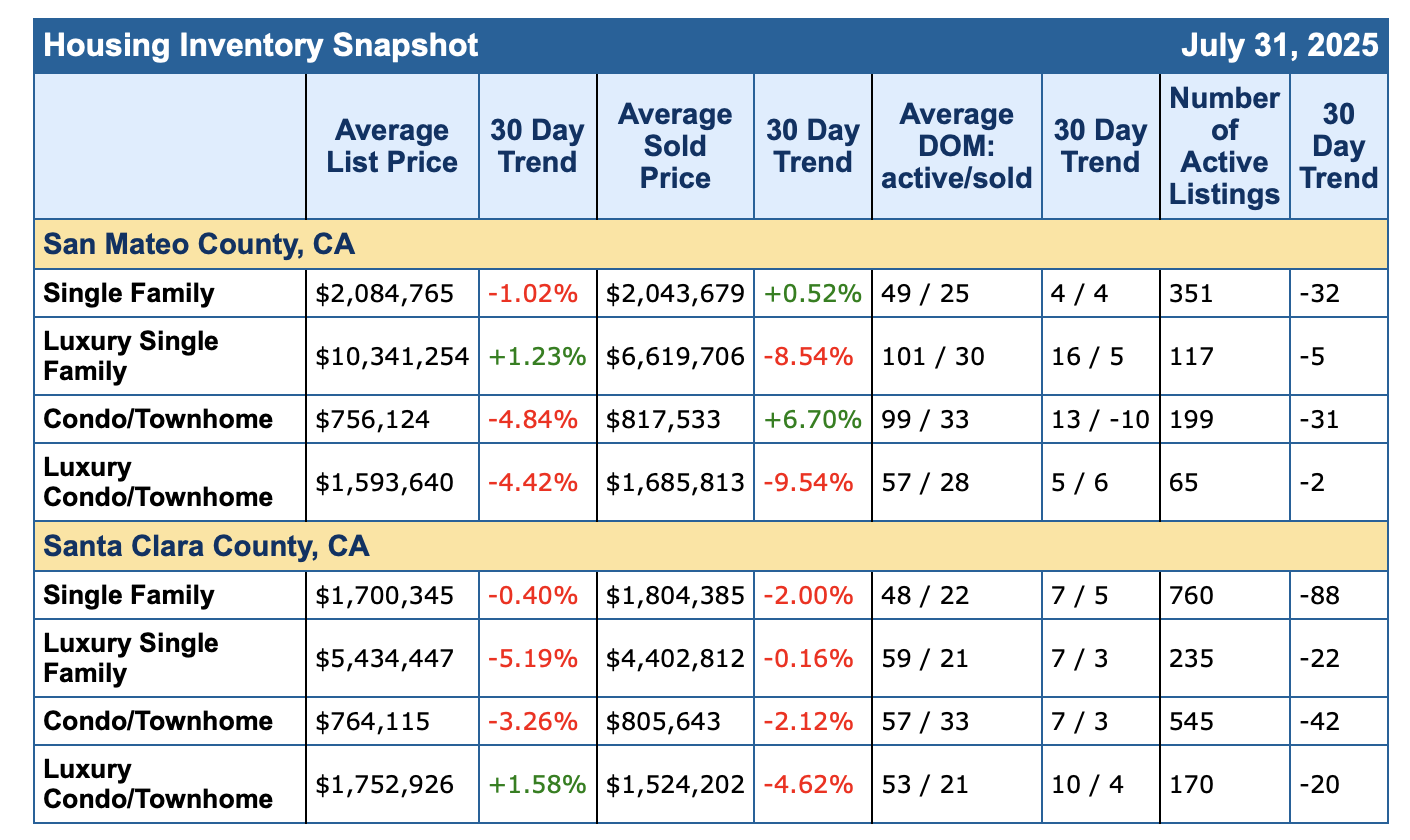

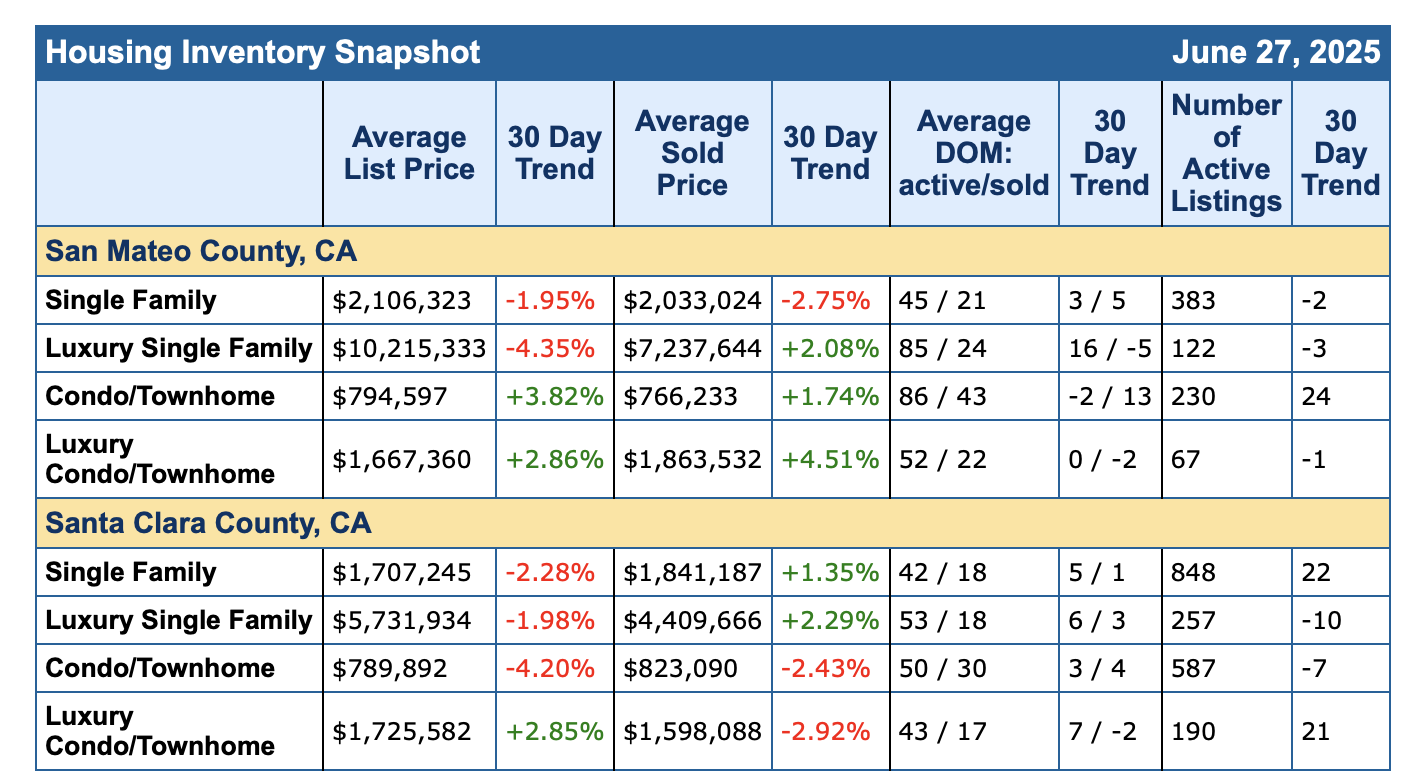

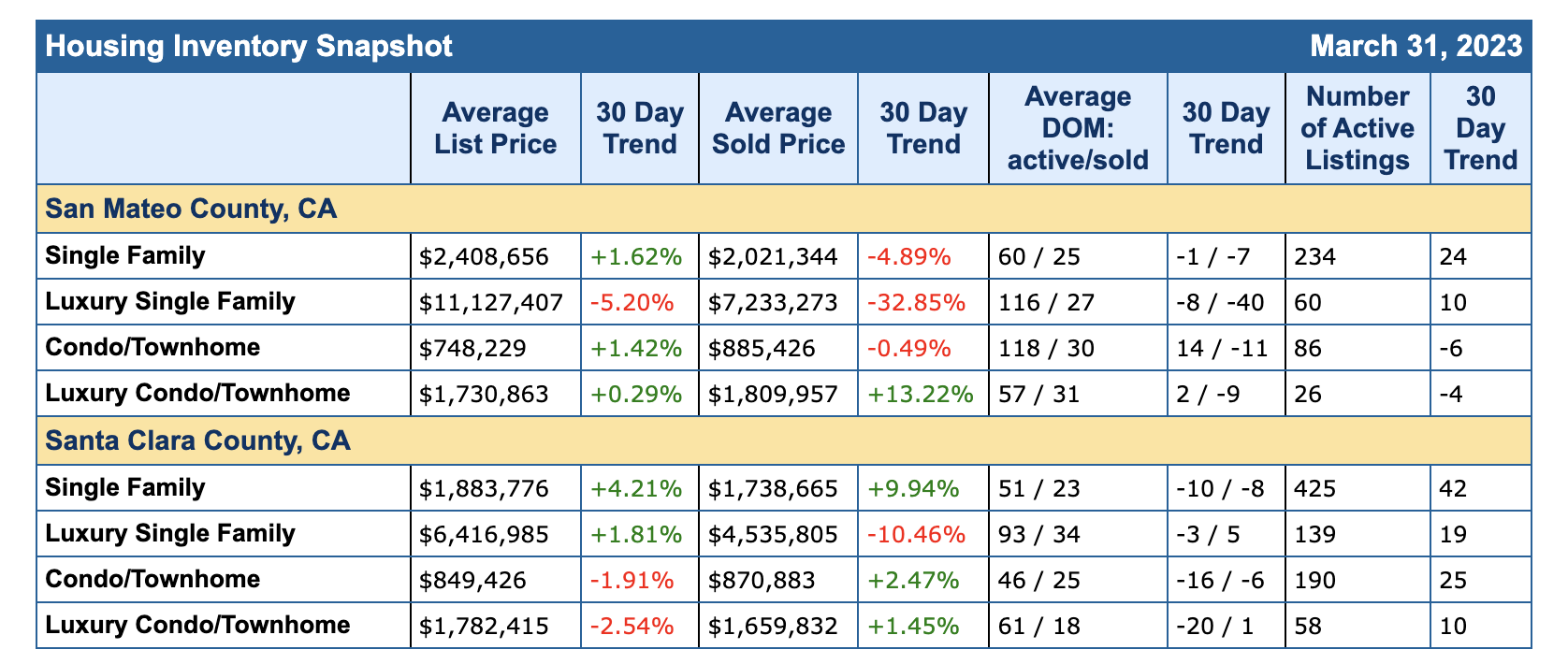

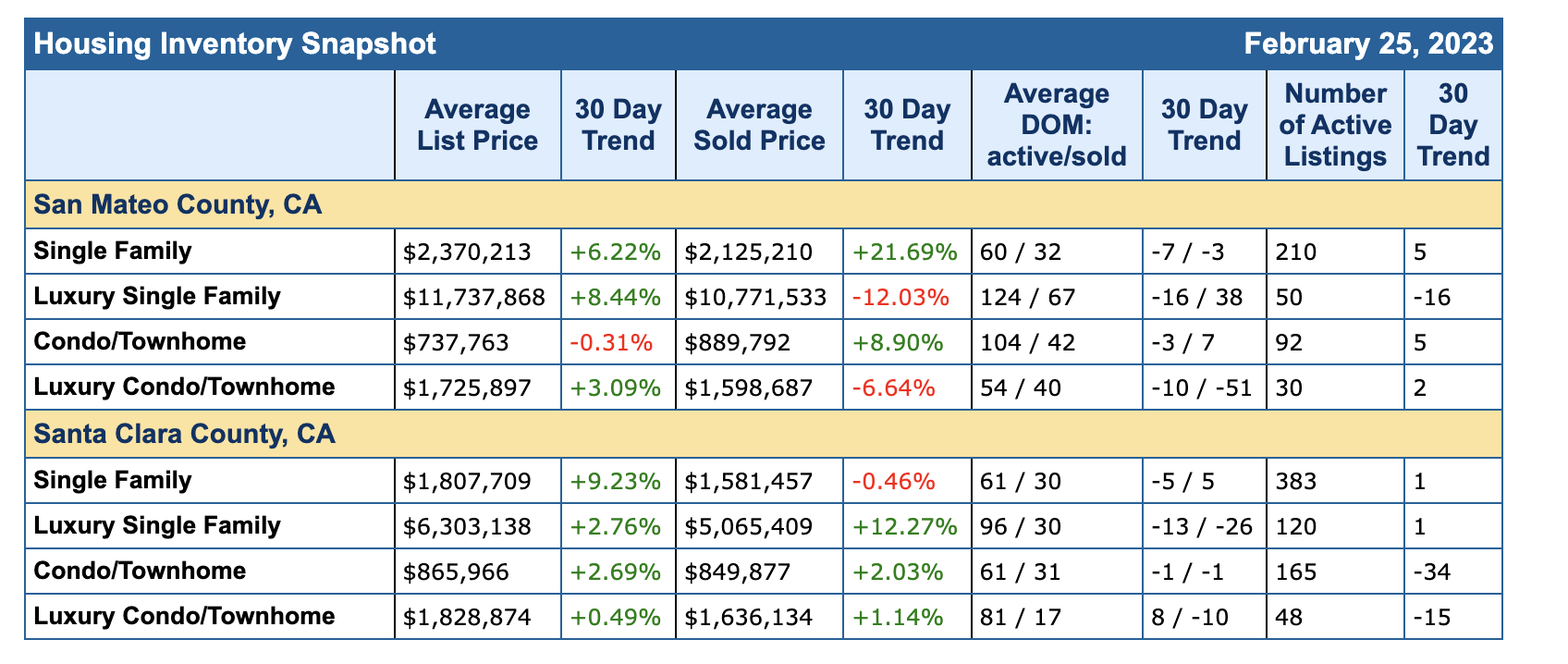

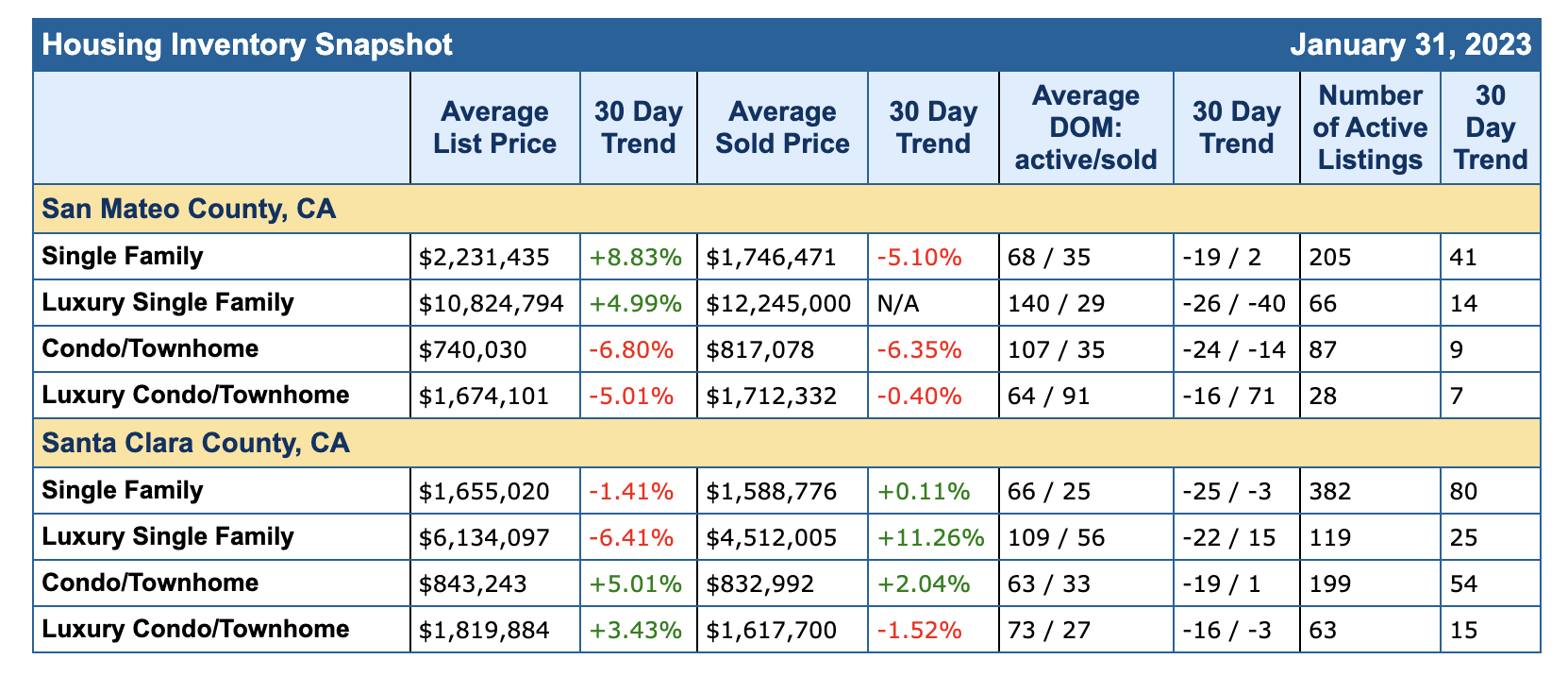

Welp – in May we saw all market points take a dip. With a slight rise in May and June for Condos / Townhomes. Across the board we are seeing a dip in sales. Is it seasonal? Doesn’t feel that way – we often see a good boost in sales each May – as that is the start of selling season and June often holds steady but this year is a bit different. There is so much going on in the world, economically and socially.

With no expected drop in interest rates and the cost of gas and groceries at an all time high. Folks are feeling it. When fear prevails, or concern, we see a dip in sales, and a dip in active buyers. Oddly enough – this sort of data makes the market ripe for buyers but not everyone feels they can take the plunge.

When the market is weird, it is actually a great time to buy in the Bay Area. Some homes still get multiple offers but some do not – and instead of waiting for a price drop – when you work with professional Realtors like The Caton Team – we search those over looked properties – and show them. Don’t wait for a price drop – if you’ve watched a home and it has not sold in 2 -3 weeks – have your agent contact their agent and get the whole picture. We do not wait for price reductions – we are proactive and will see if there is middle ground a buyer and seller can stand on.

With values dipping .8% – 13% – that is a market for buyers! Sellers are not seeing the demand we once had when rates were lower and if a seller has to sell, they are taking a moment to grieve their lost value and hopefully moving forward. The market is the people and what the people are feeling.

If you want to live in the Bay Area, if you have a steady job here and want to grow roots here – NOW – is a great time to buy. There are properties sitting, there are price reductions – this is an opportunity for a buyer to get a house, even under list with contingencies! As long as you see yourself here for about 7-10 years – that is the normal time it takes to see appriciation. The longer you hold onto a home, the better. So when the market is soft and you have long terms goals here – let’s jump in.

The Caton Team provides free buying and selling consultations – to determine the current value of your home if you are selling or if you’re in the market to buy – where you get the most bang for your buck.

Remember, each neighborhood is different, if you are considering a purchase – let us guide you through this and help you find your way home.

If you’re in the market to sell – each area and price point has it’s own pros and cons – let us help you figure out your next steps.

What are your thoughts for the year ahead?

For my selling clients, life changes everyday and if you need to sell your home – let’s come up with a strategy to get you sold! Even in an odd market The Caton Team can help you strategically sell your home. We have before and we will again. We move with the market.

For my buyers, some homes are garnering multiple offers, but some are overlooked. With a little legwork, a buyer can truly find some great opportunities when they align with the market.

If you’re considering a Real Estate move, contact The Caton Team for a free consultation. With over 45+ years of combined Real Estate experience, we have the knowledge and know-how to guide you to your goal. Call us at 650.799.4333 or email us at sabrina_caton@yahoo.com.

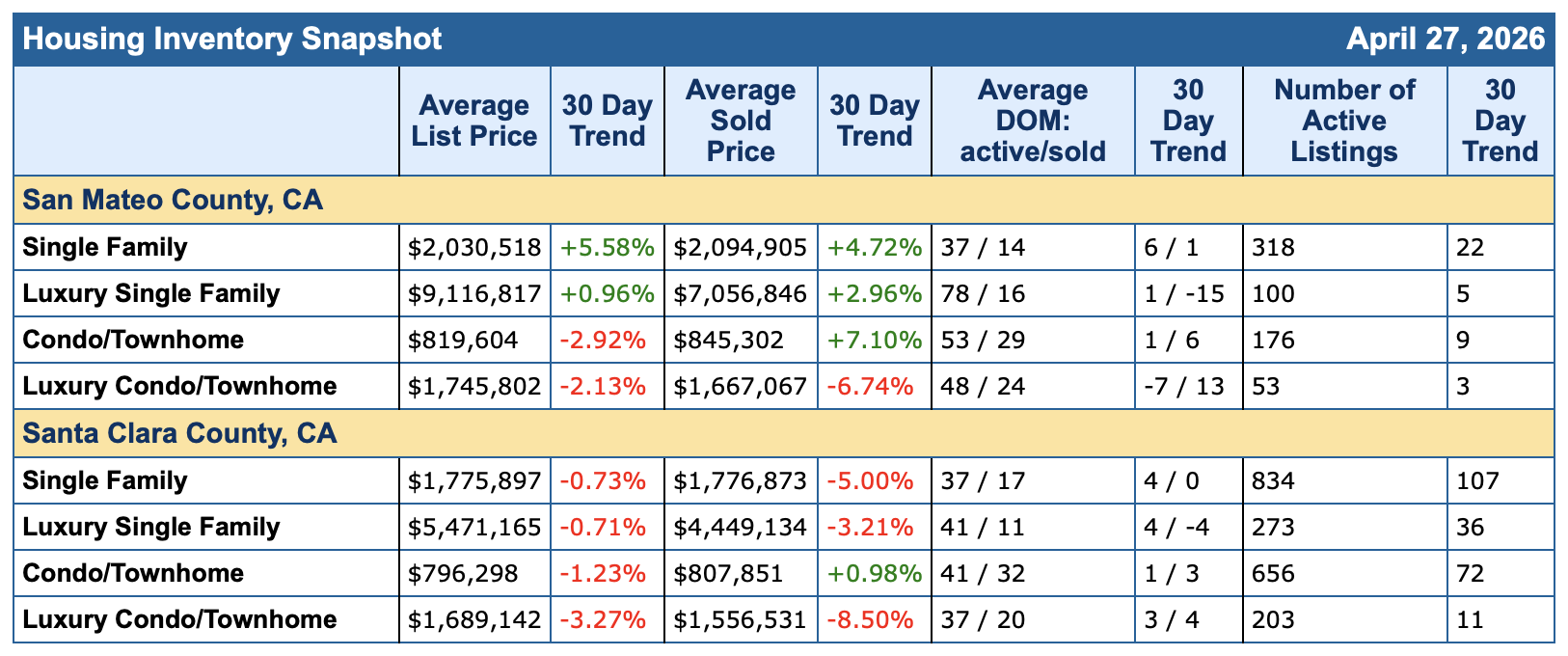

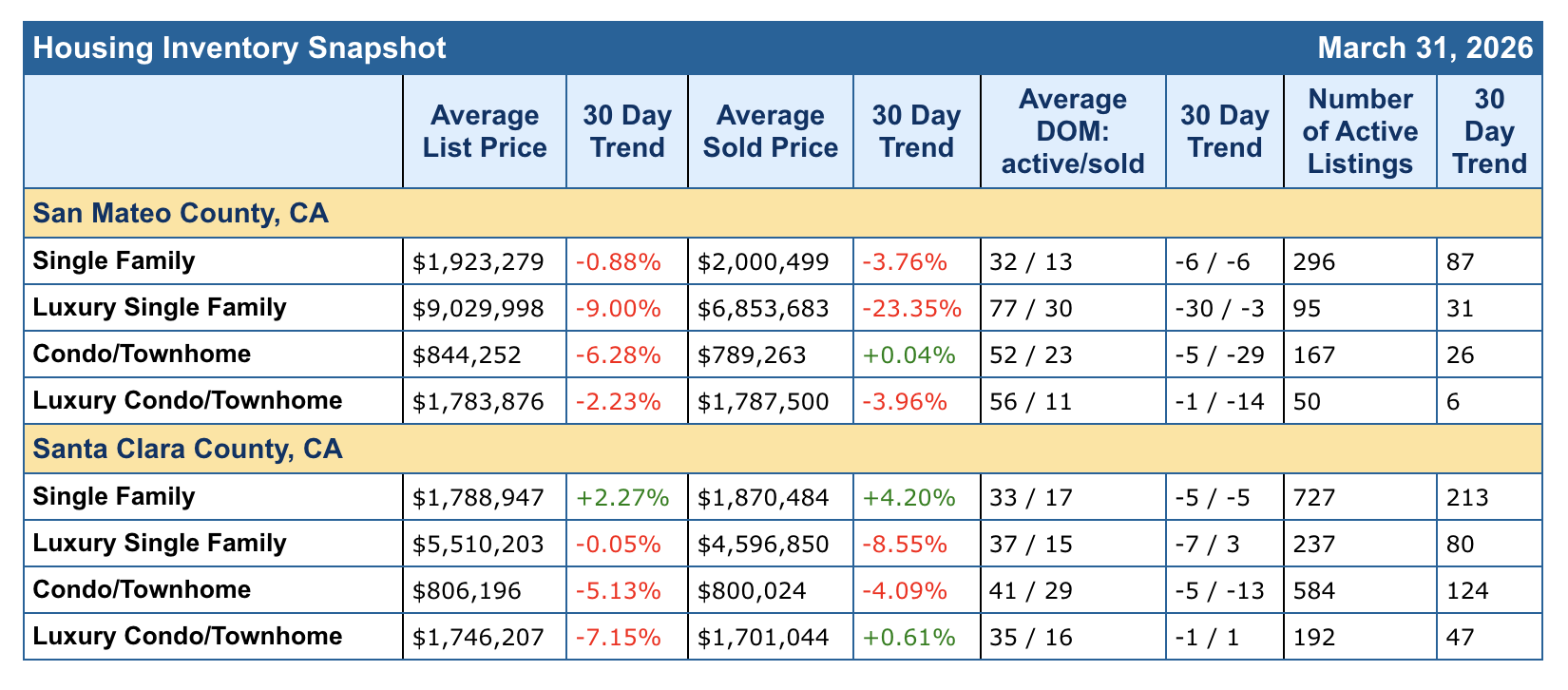

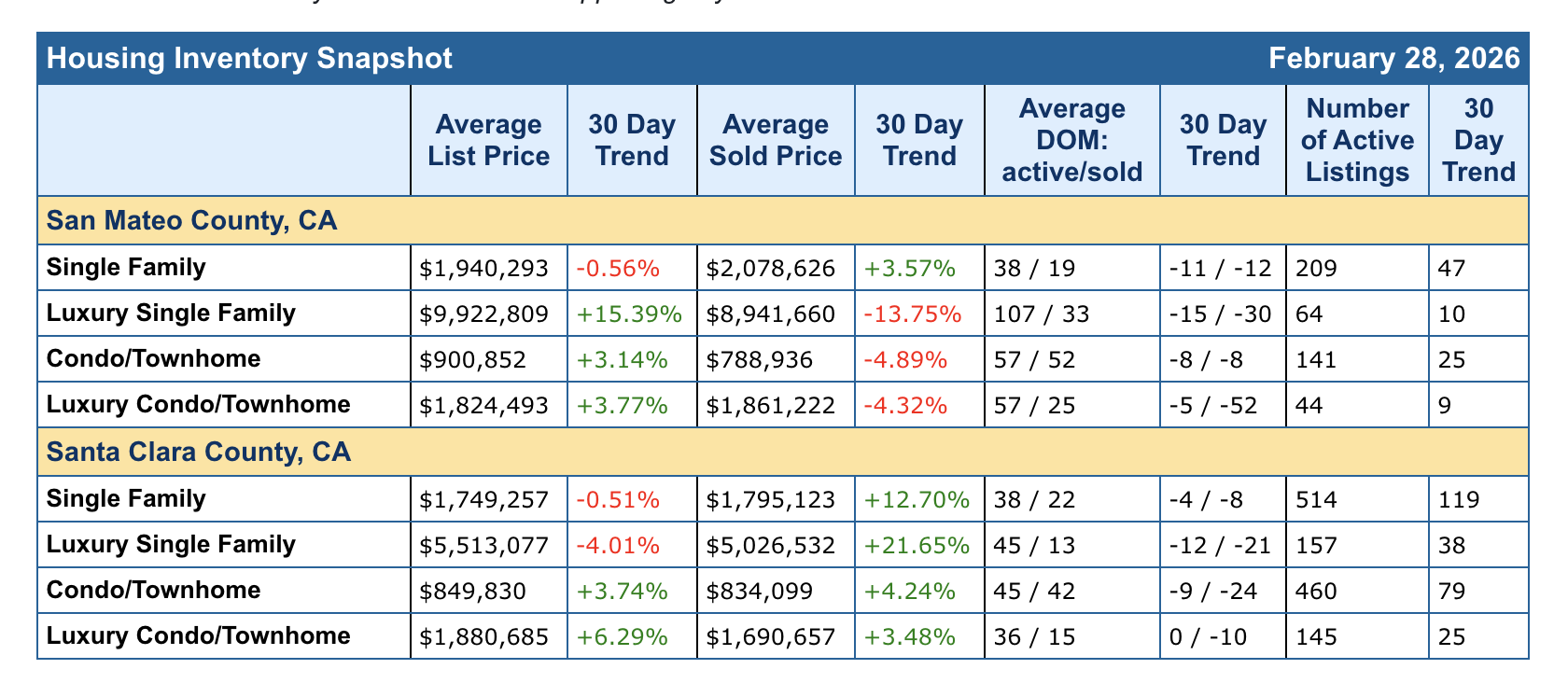

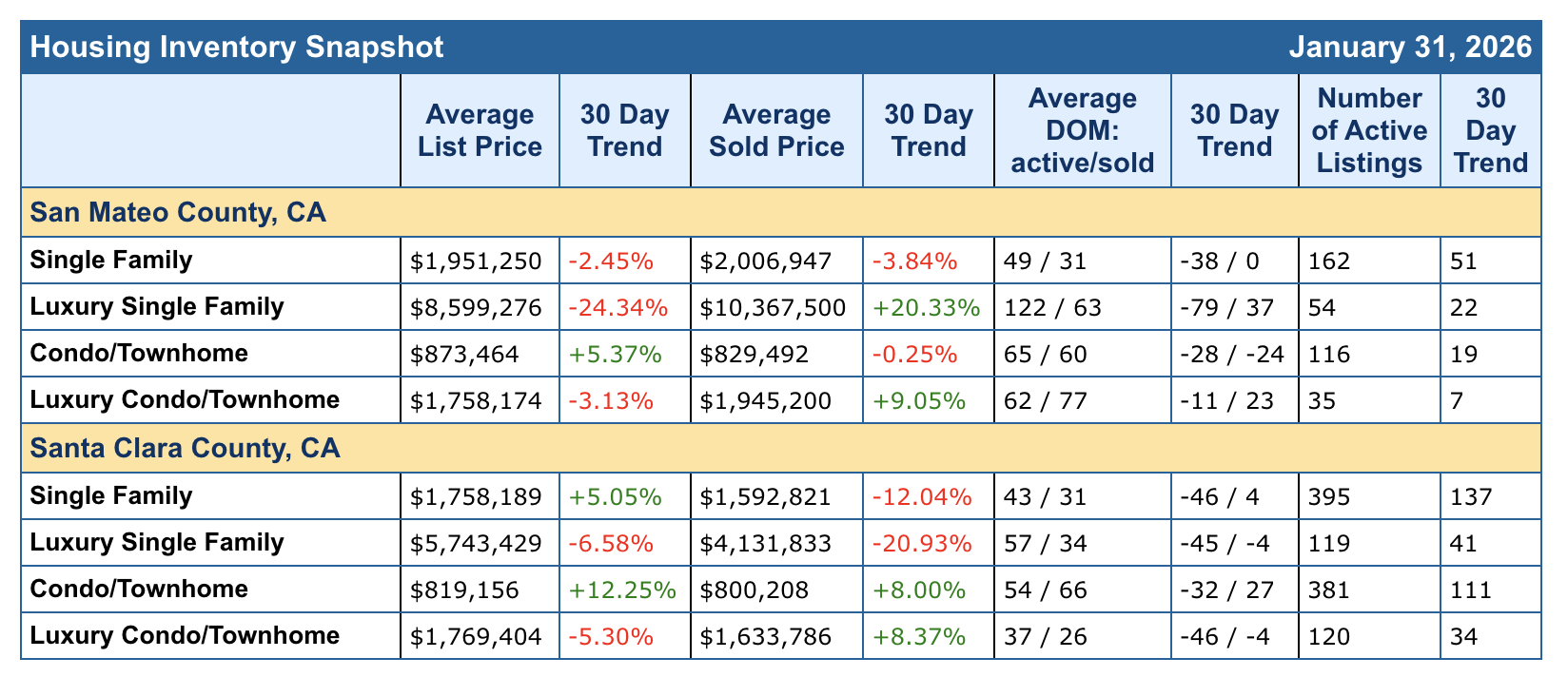

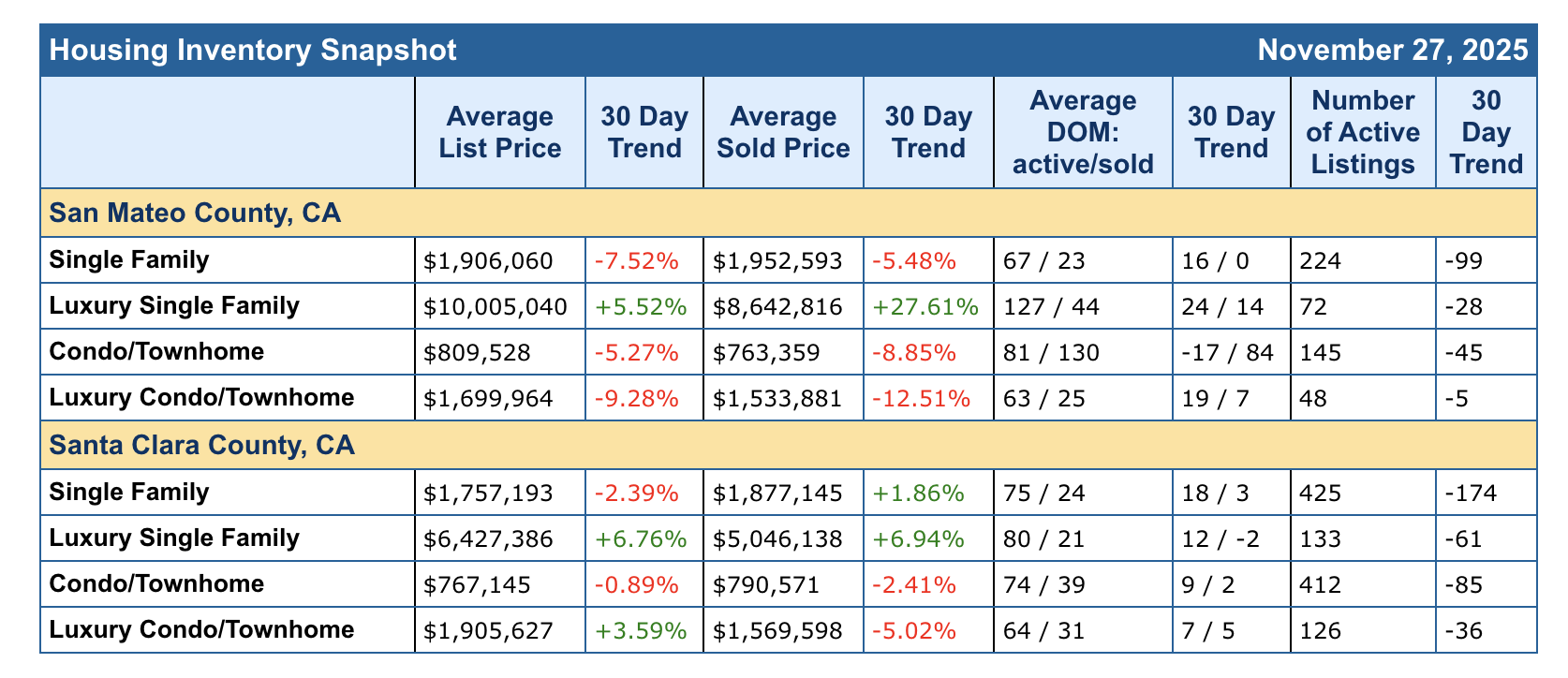

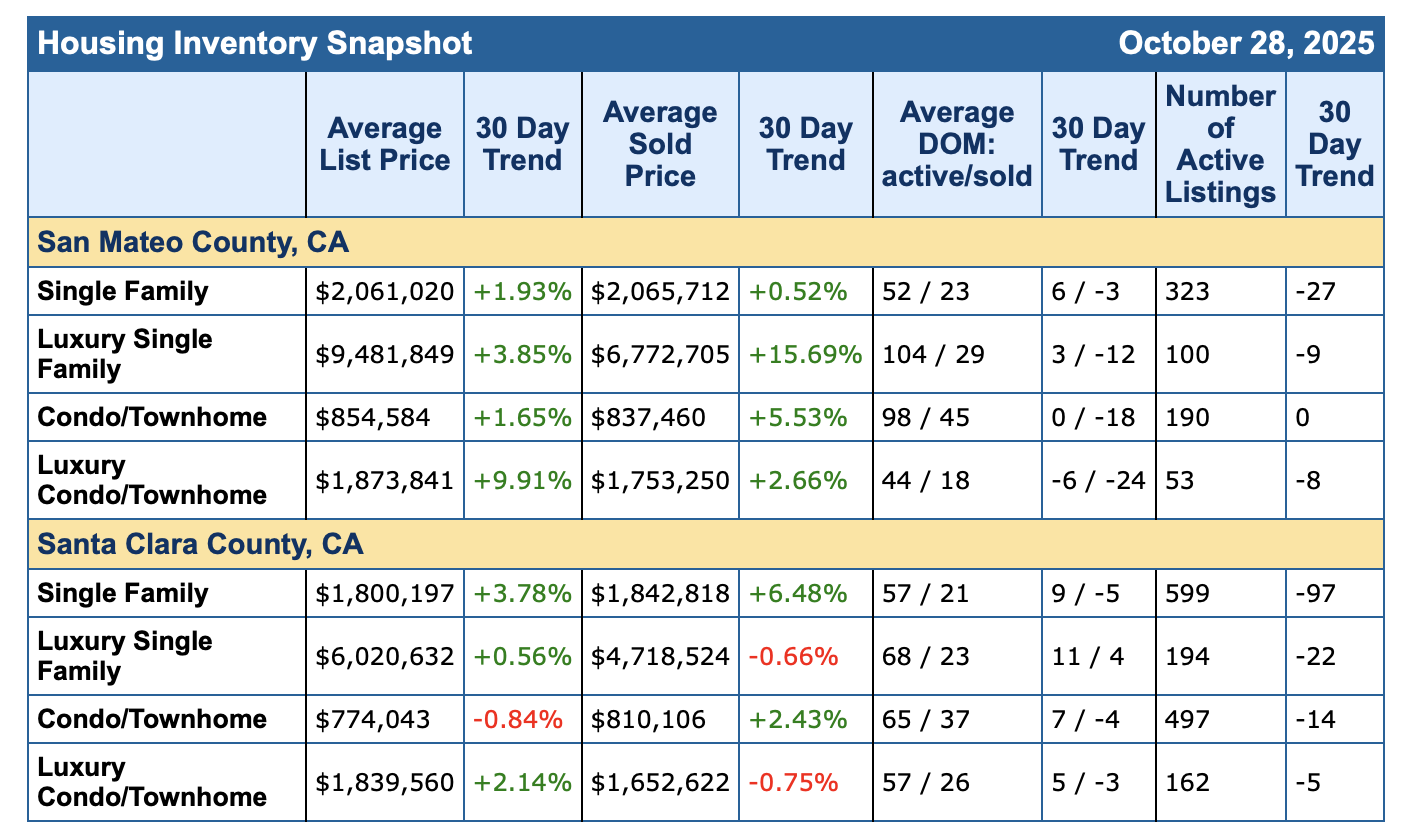

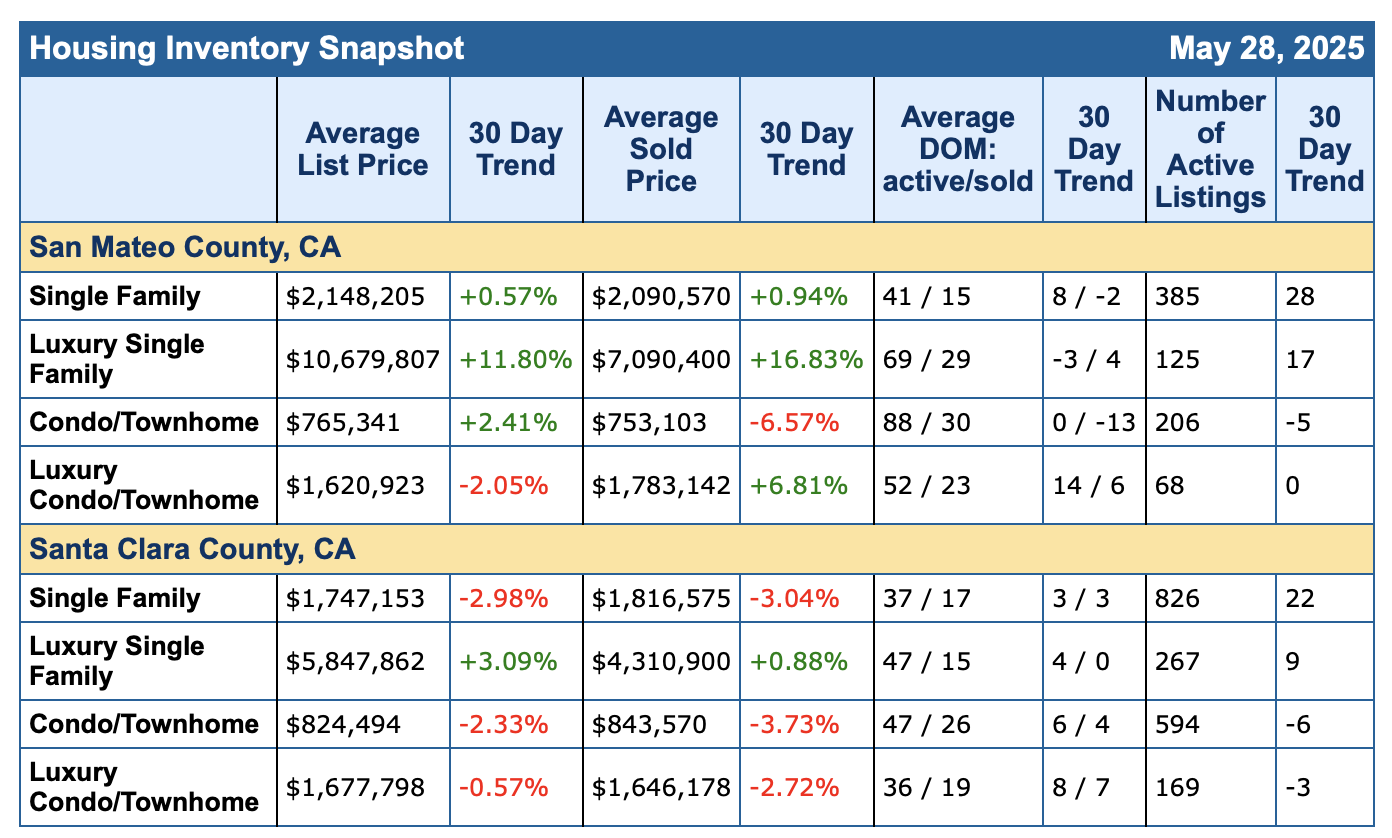

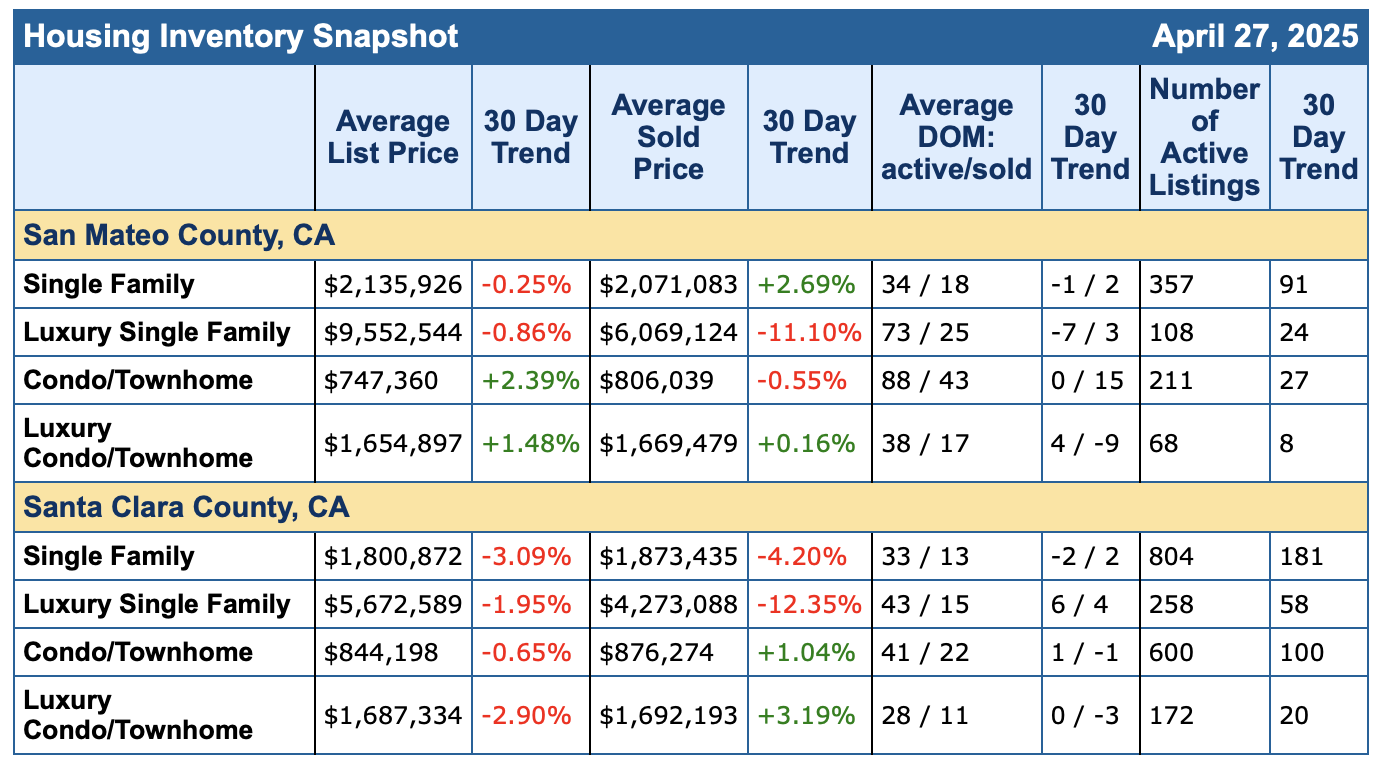

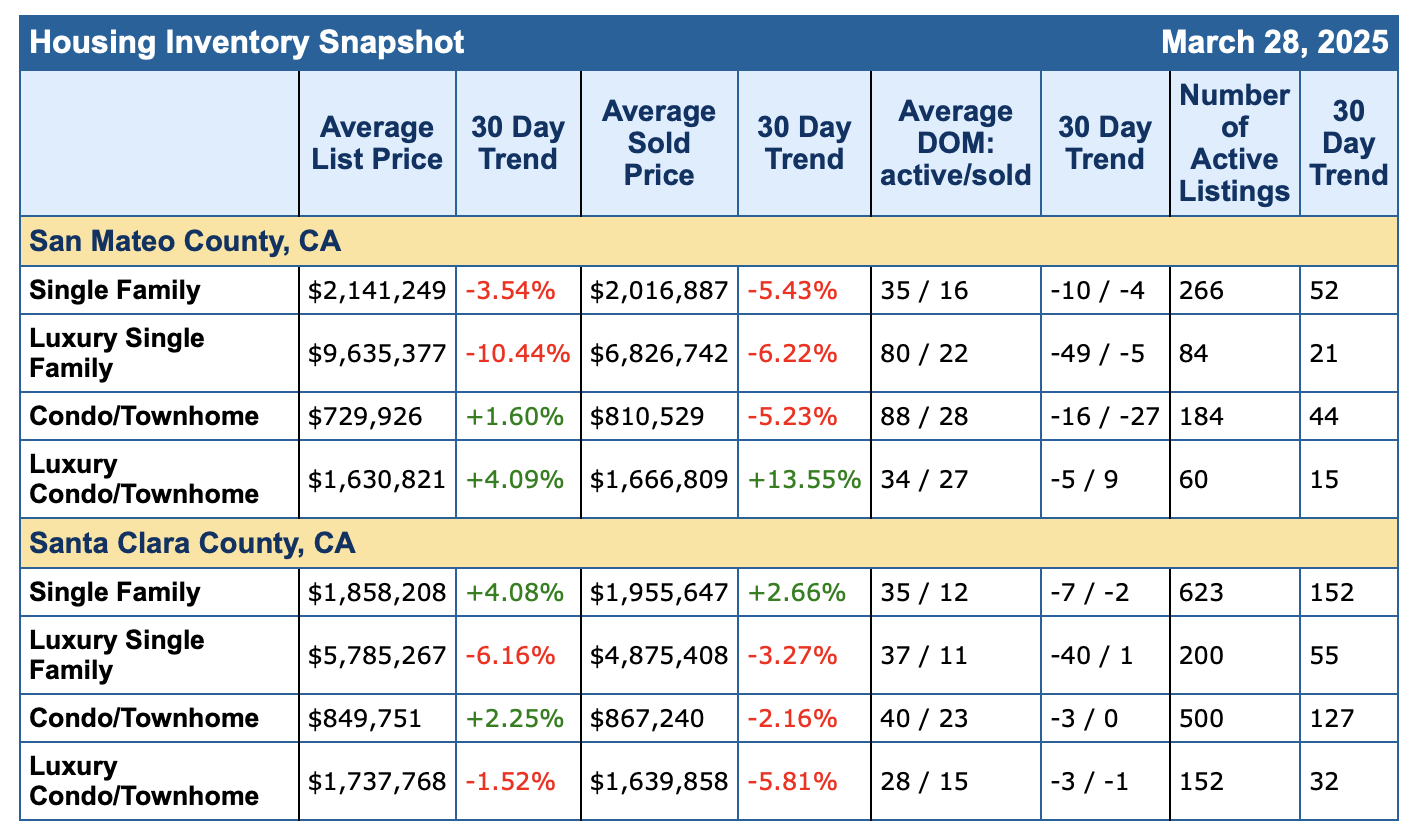

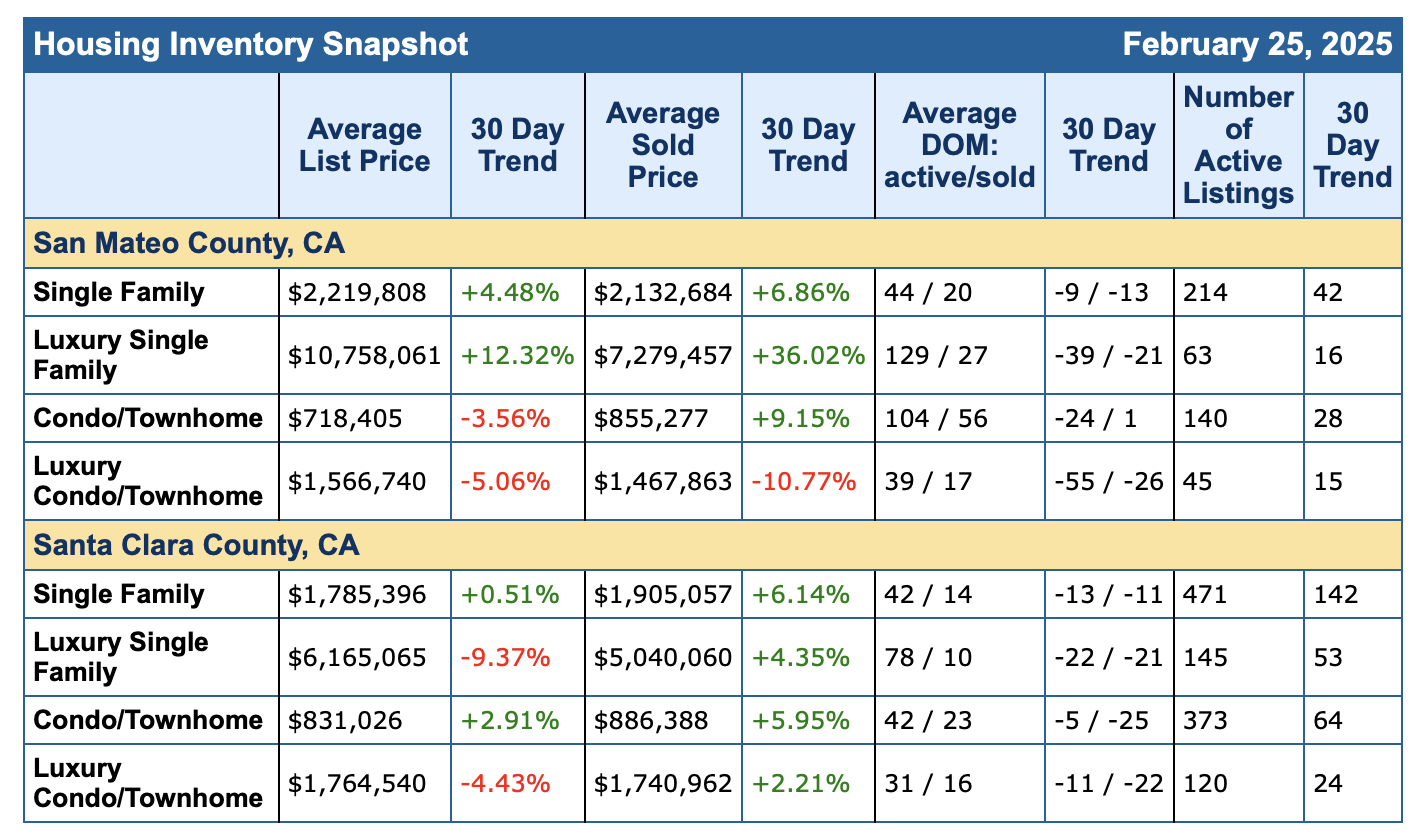

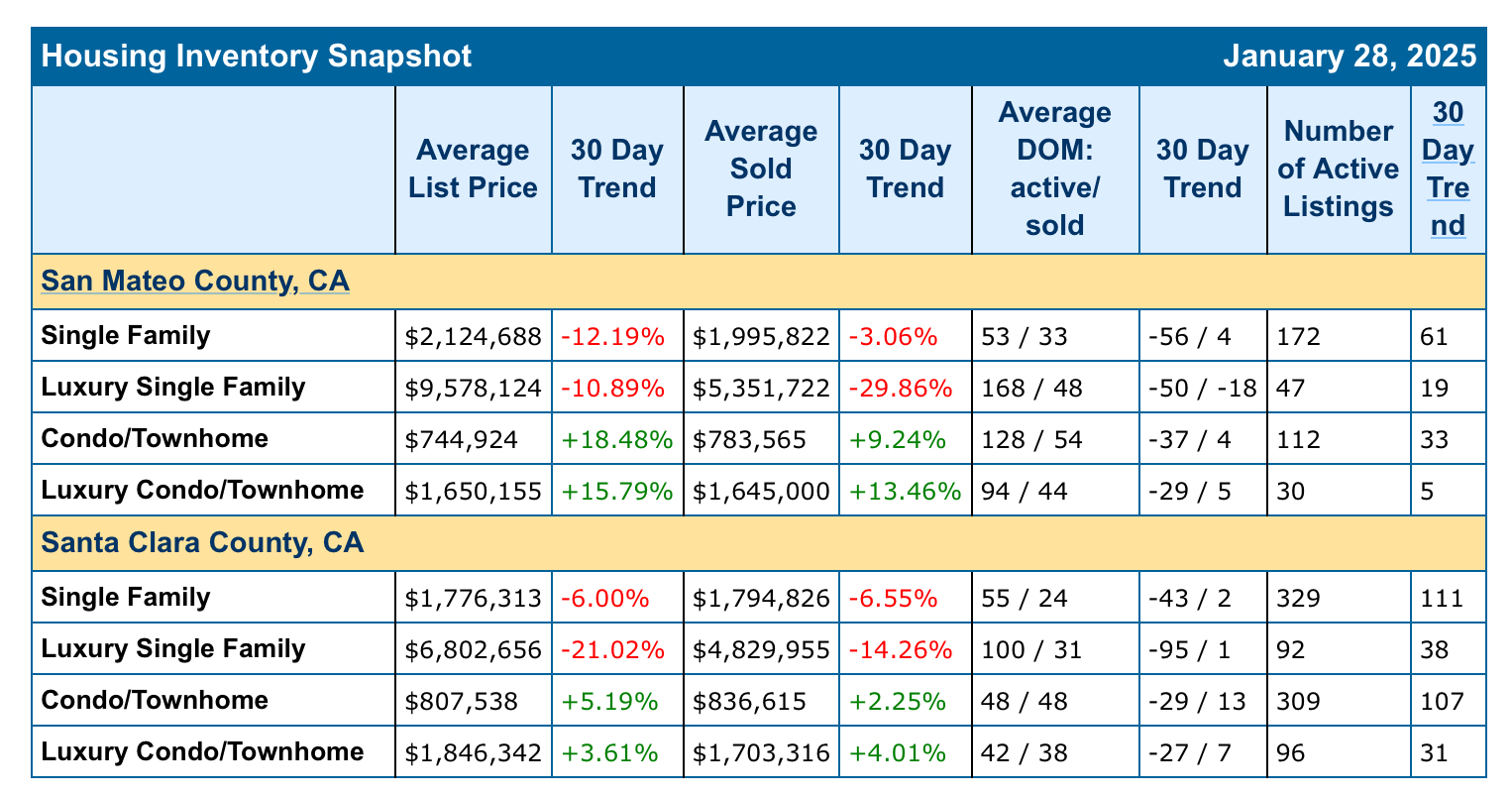

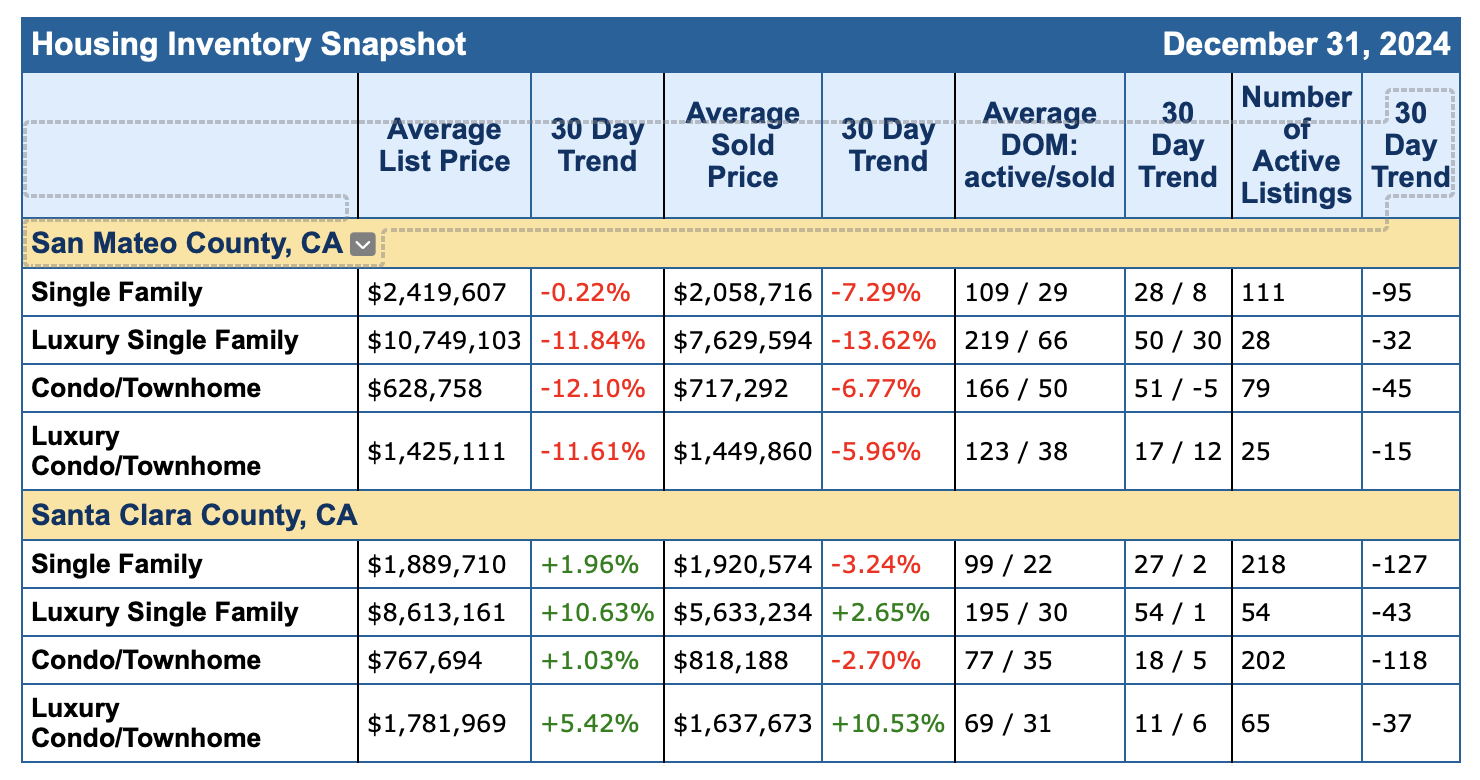

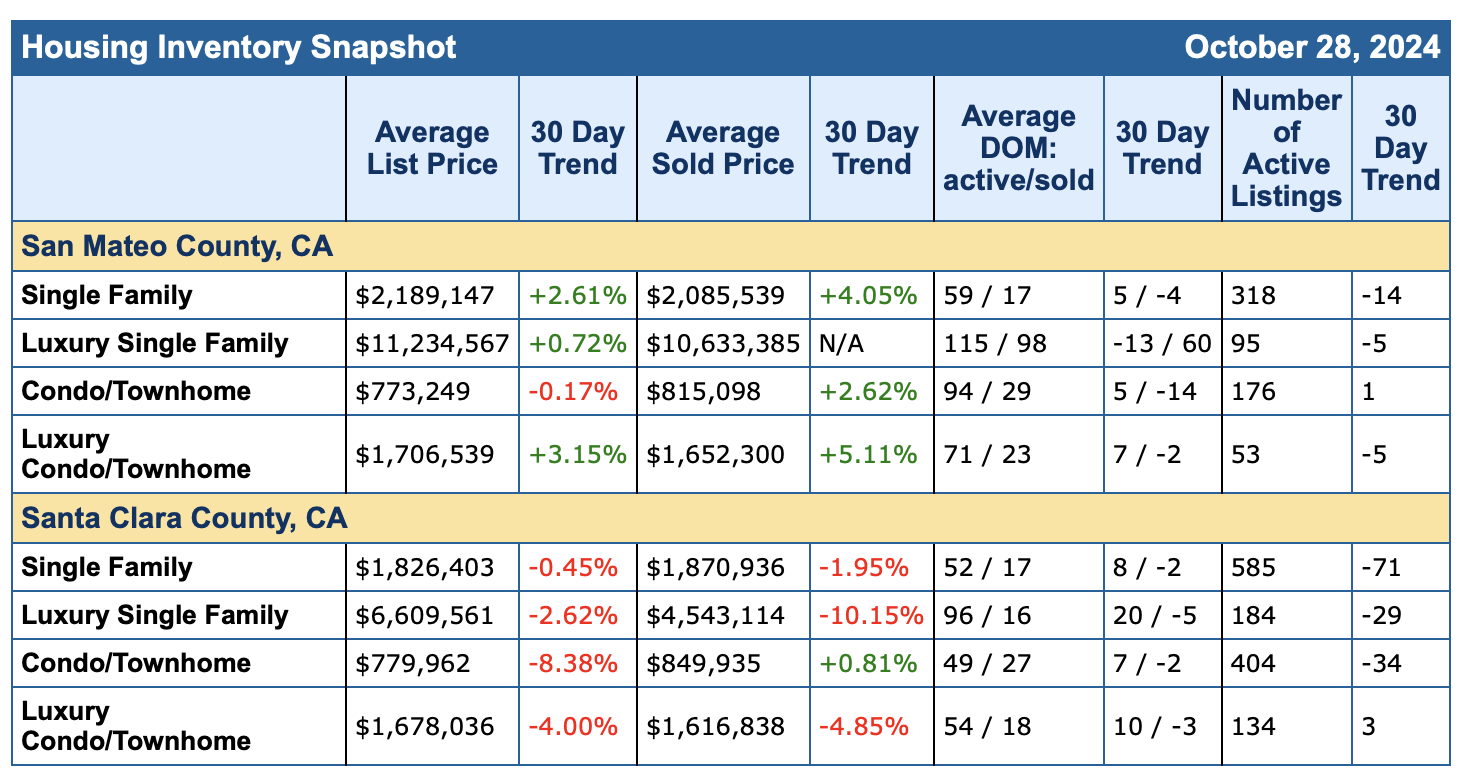

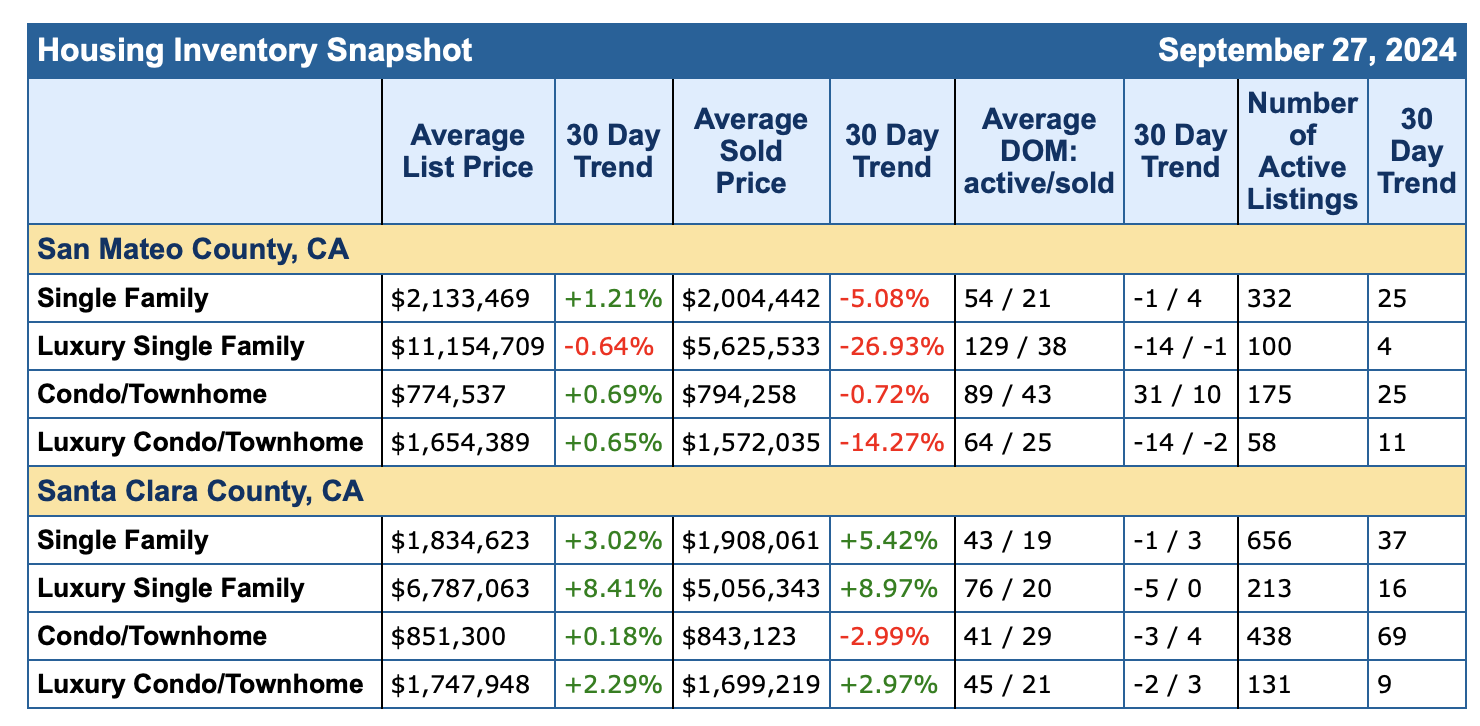

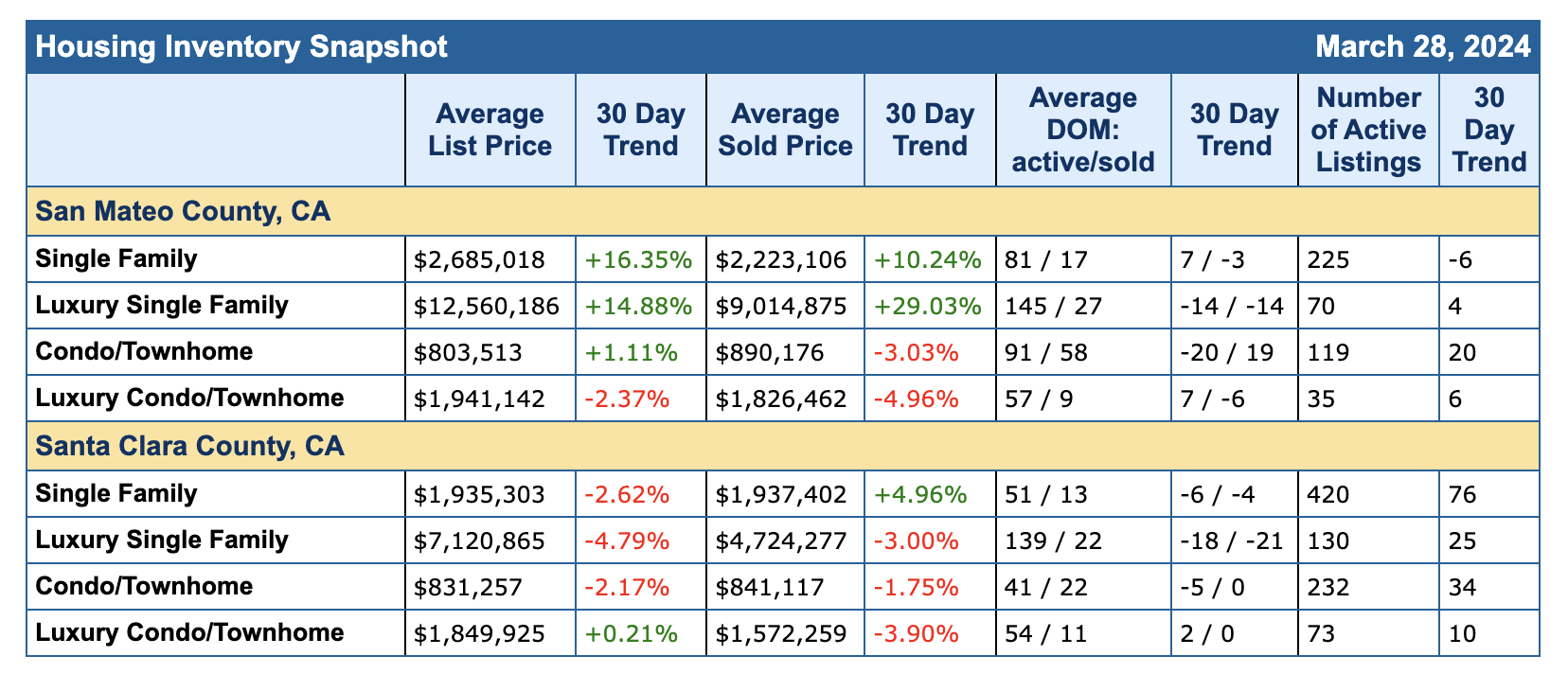

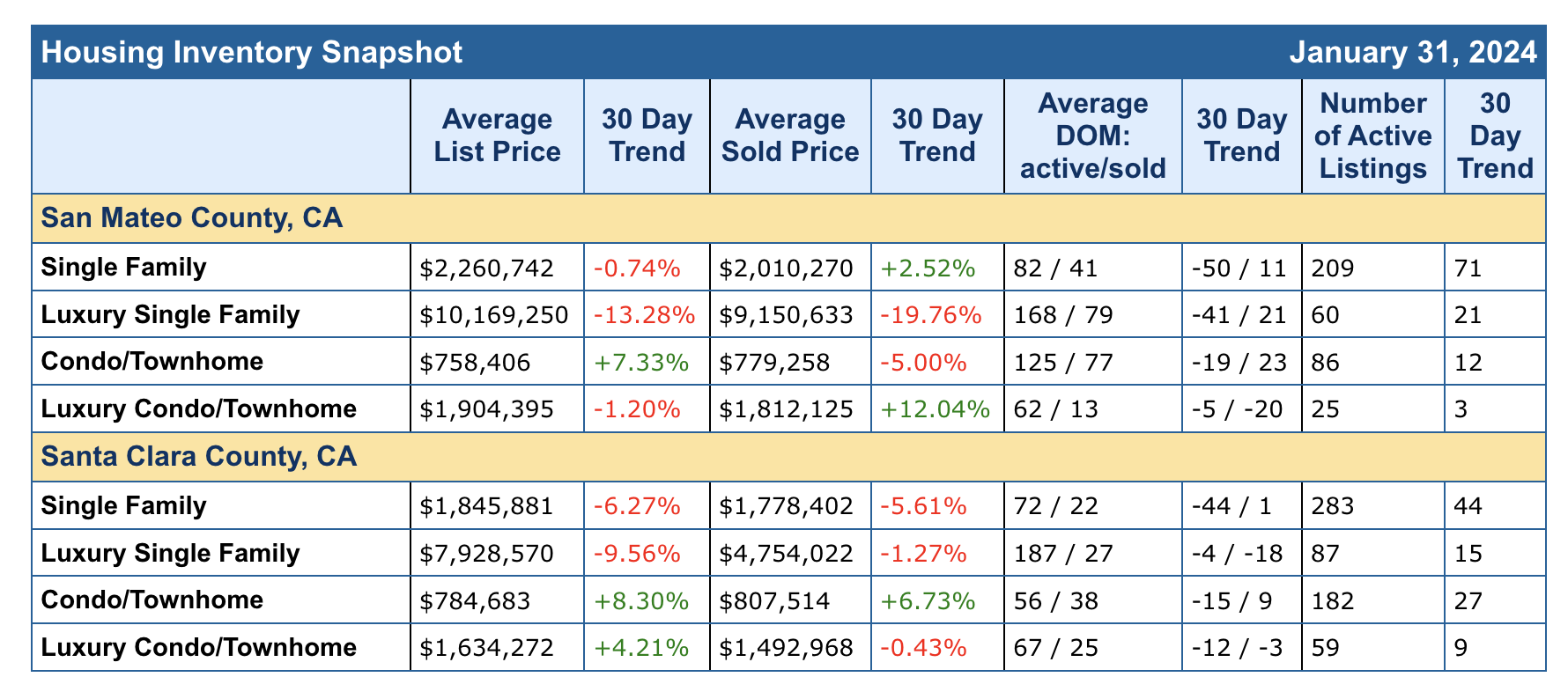

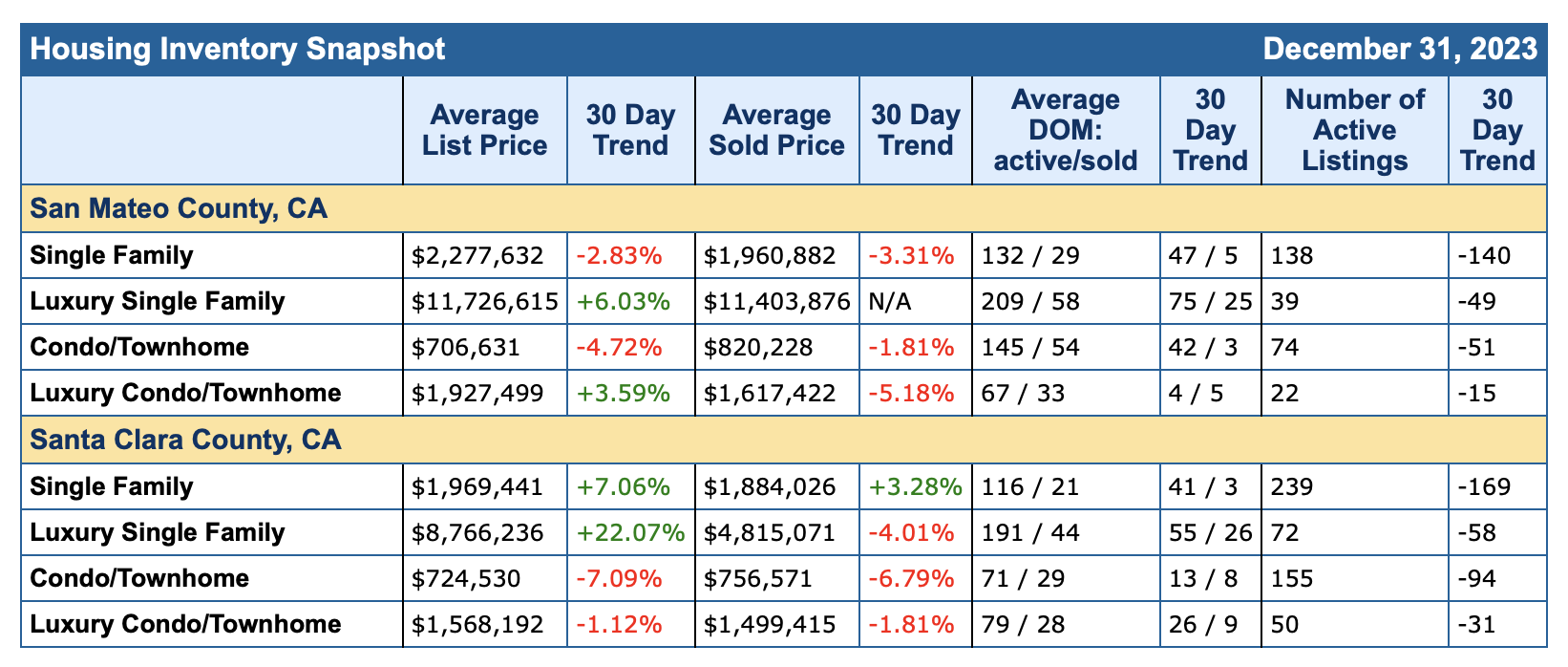

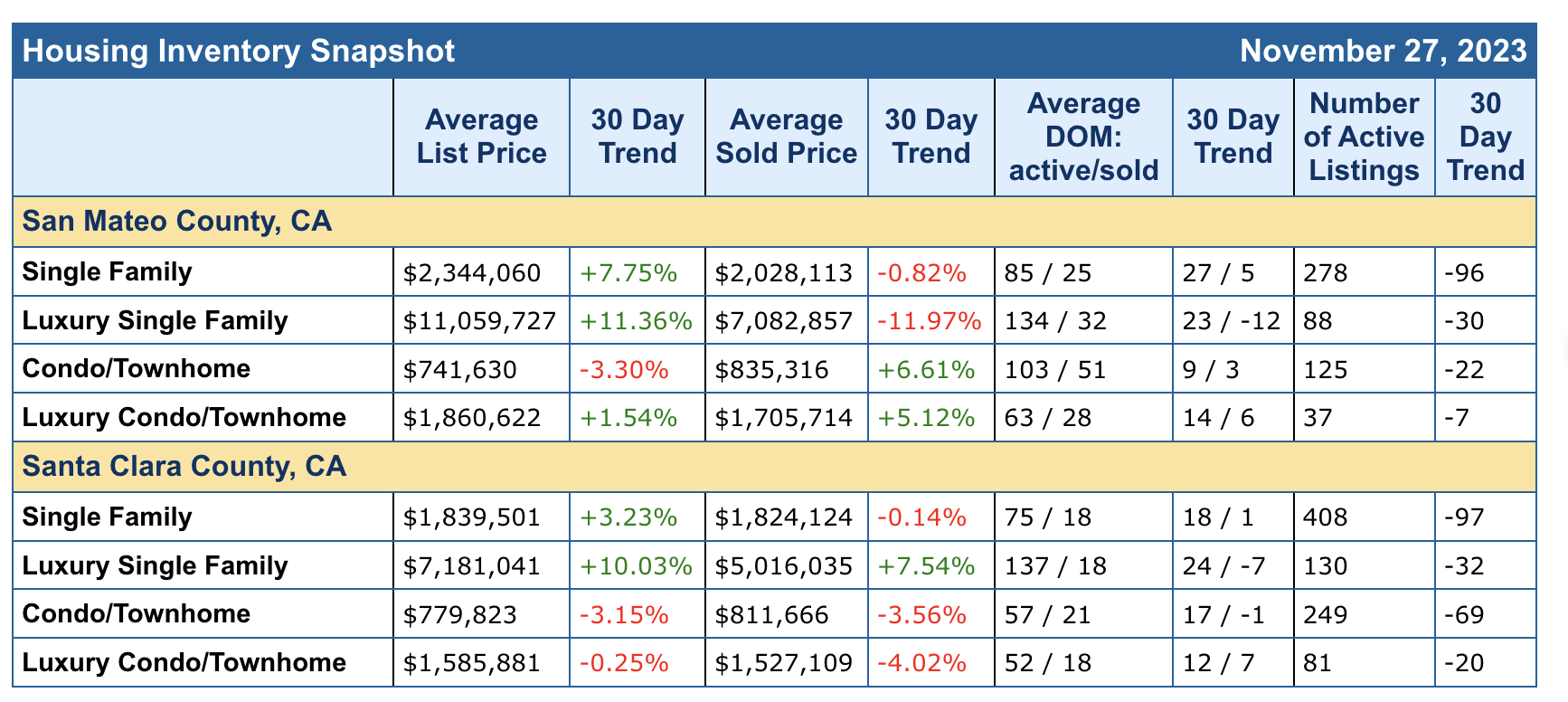

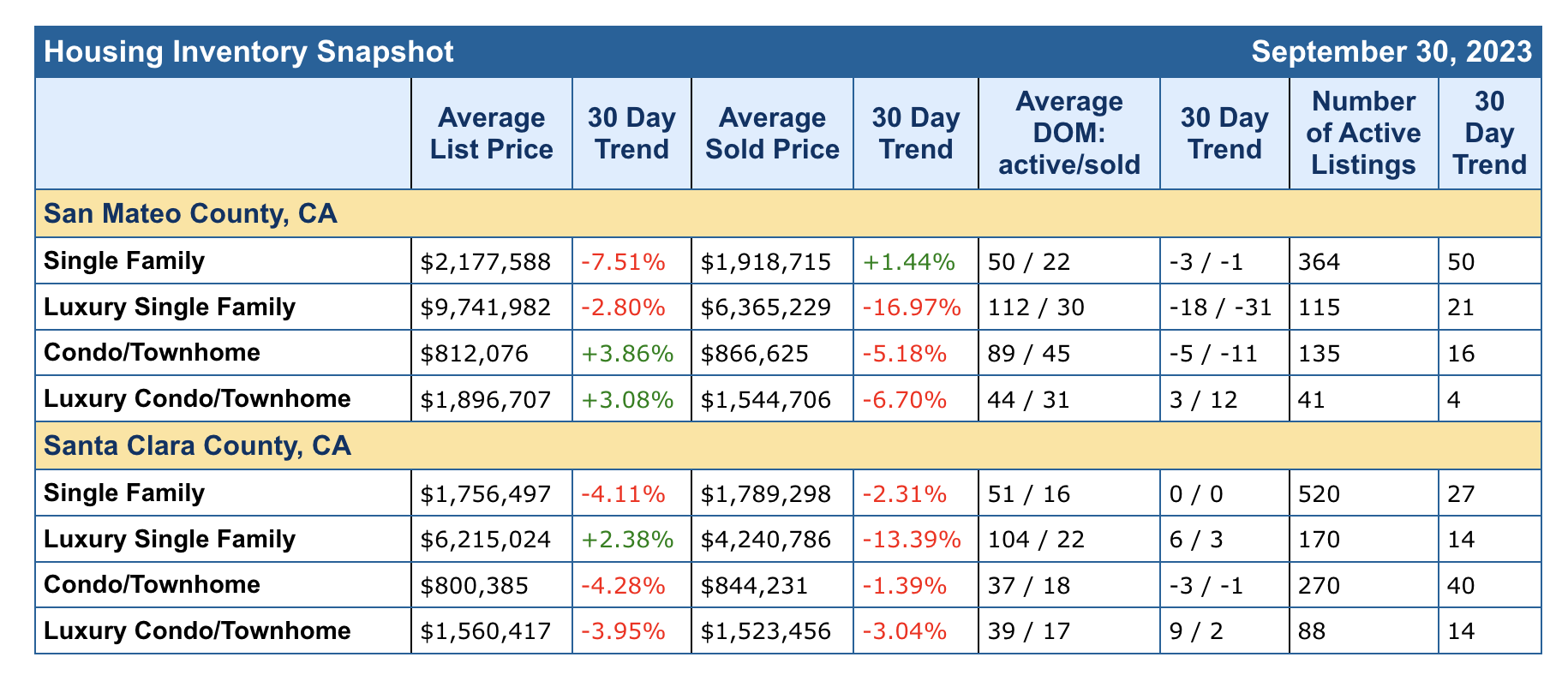

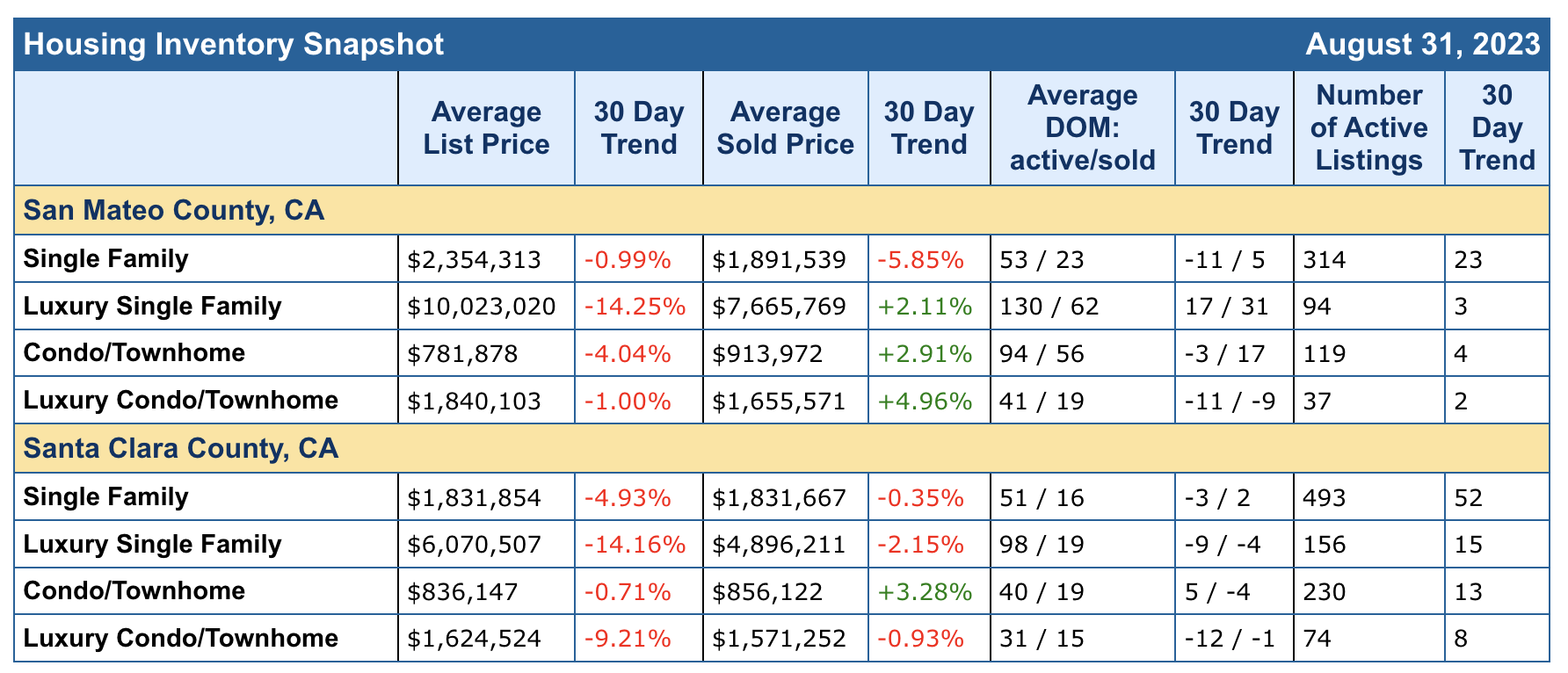

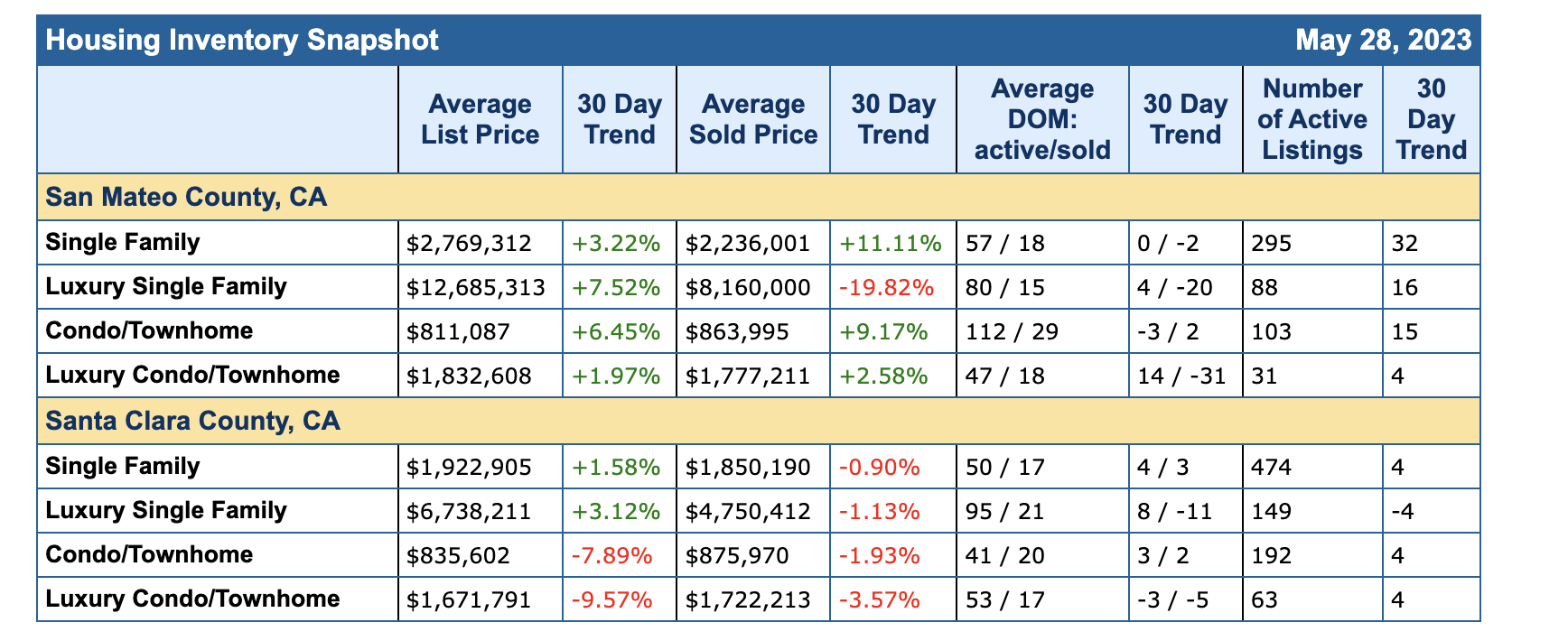

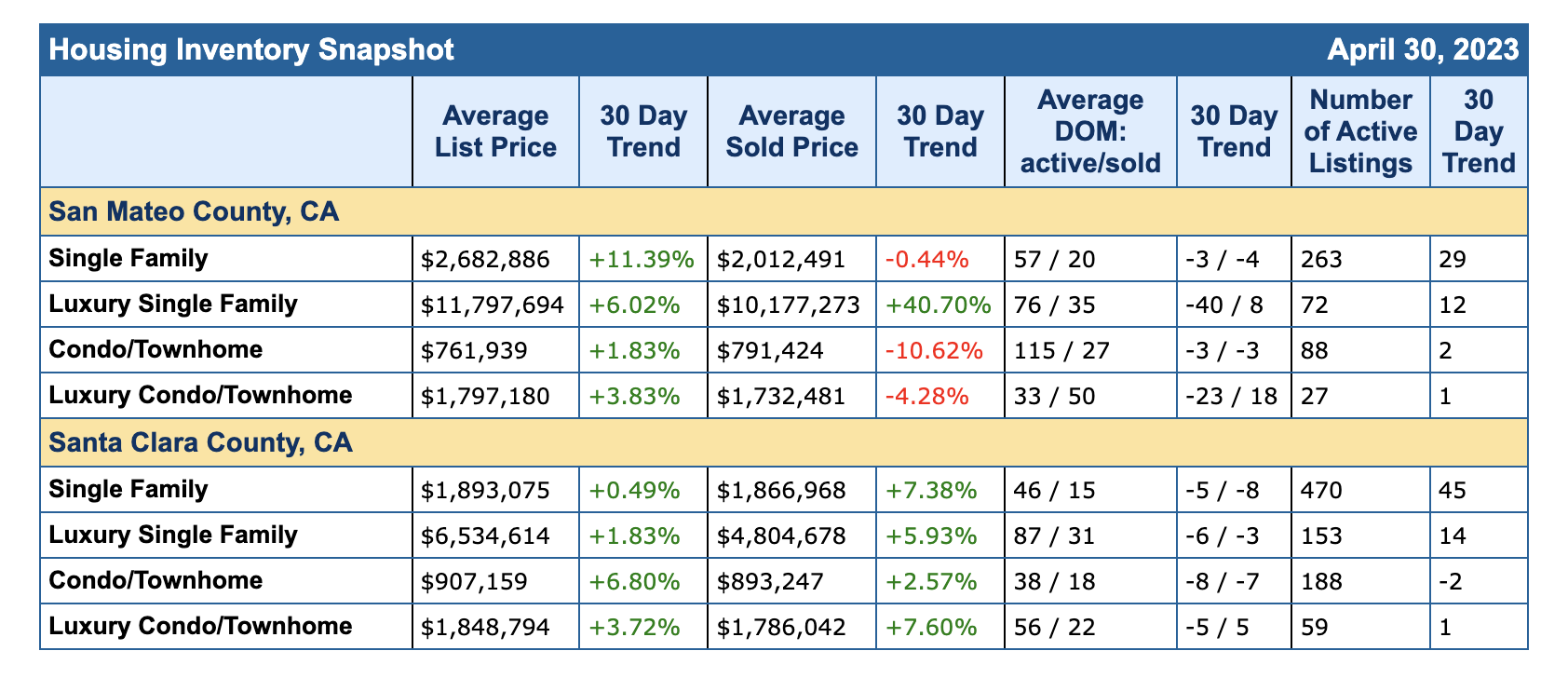

Let’s see our month over month…

How can The Caton Team Help You?

Contact The Caton Team 650.799.4333 | Email Info@TheCatonTeam.com

Whether you are selling or buying – today or tomorrow – contact The Caton Team – we’re happy to help you achieve your Real Estate goals.

Effective. Efficient. Responsive. The Caton Team 🏡

Each market is unique and with over 45 years of combined Real Estate experience, The Caton Team is more than happy to be of service if and when you are considering a move. Contact us anytime during your journey, together we’ll help you achieve your Real Estate goals.

Got Questions? The Caton Team is here to help.

Call | Text | Sabrina 650.799.4333 | EMAIL | WEB | BLOG

We love what we do and would love to help you navigate your sale or purchase of Residential Real Estate. Please reach out for a personal consultation. Please enjoy our free resources below and get to know our team TESTIMONIALS.

| HOW TO SELL | VIRTUAL STAGING | A GUIDE TO BUYING | BUYING INFO | MOVING | TESTIMONIALS |

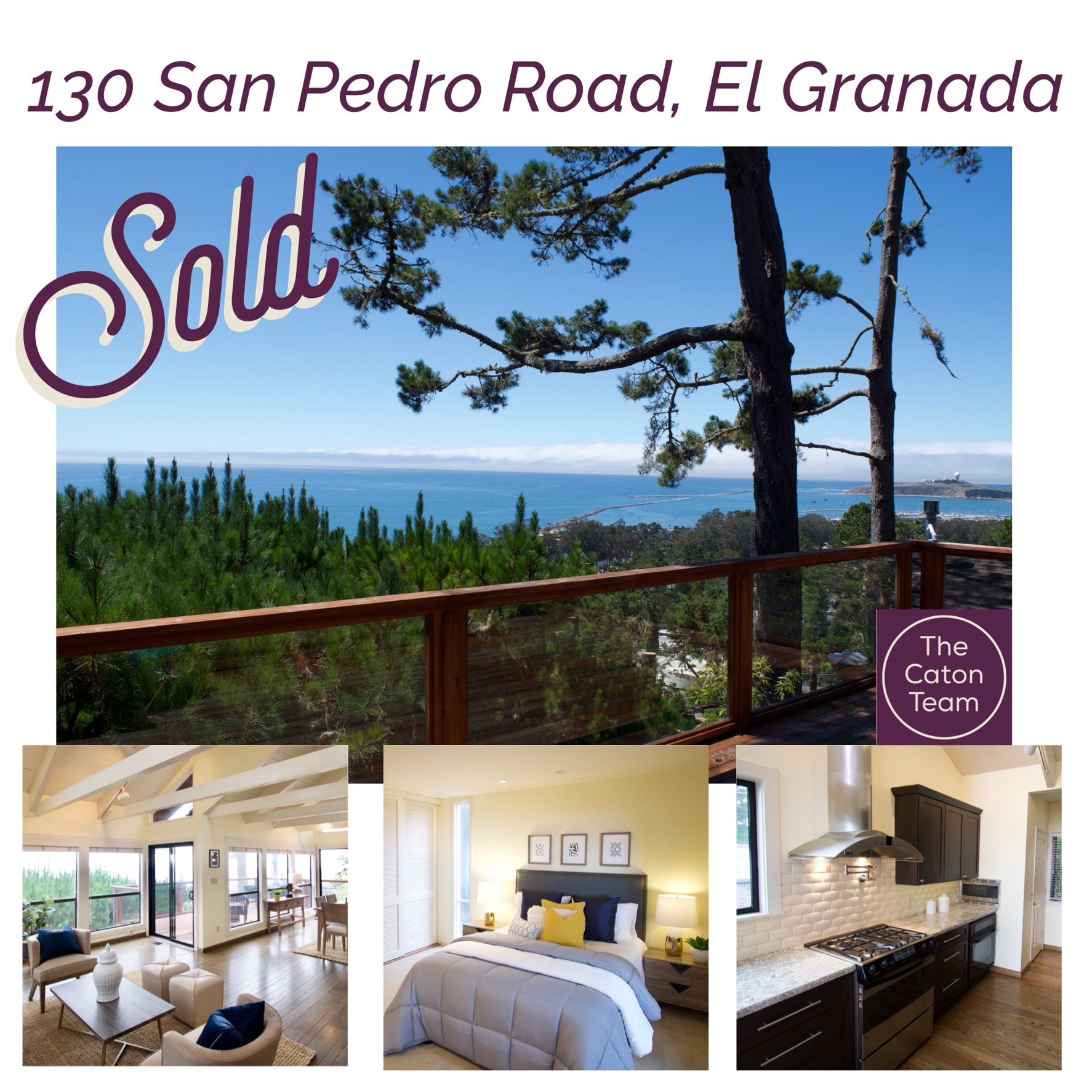

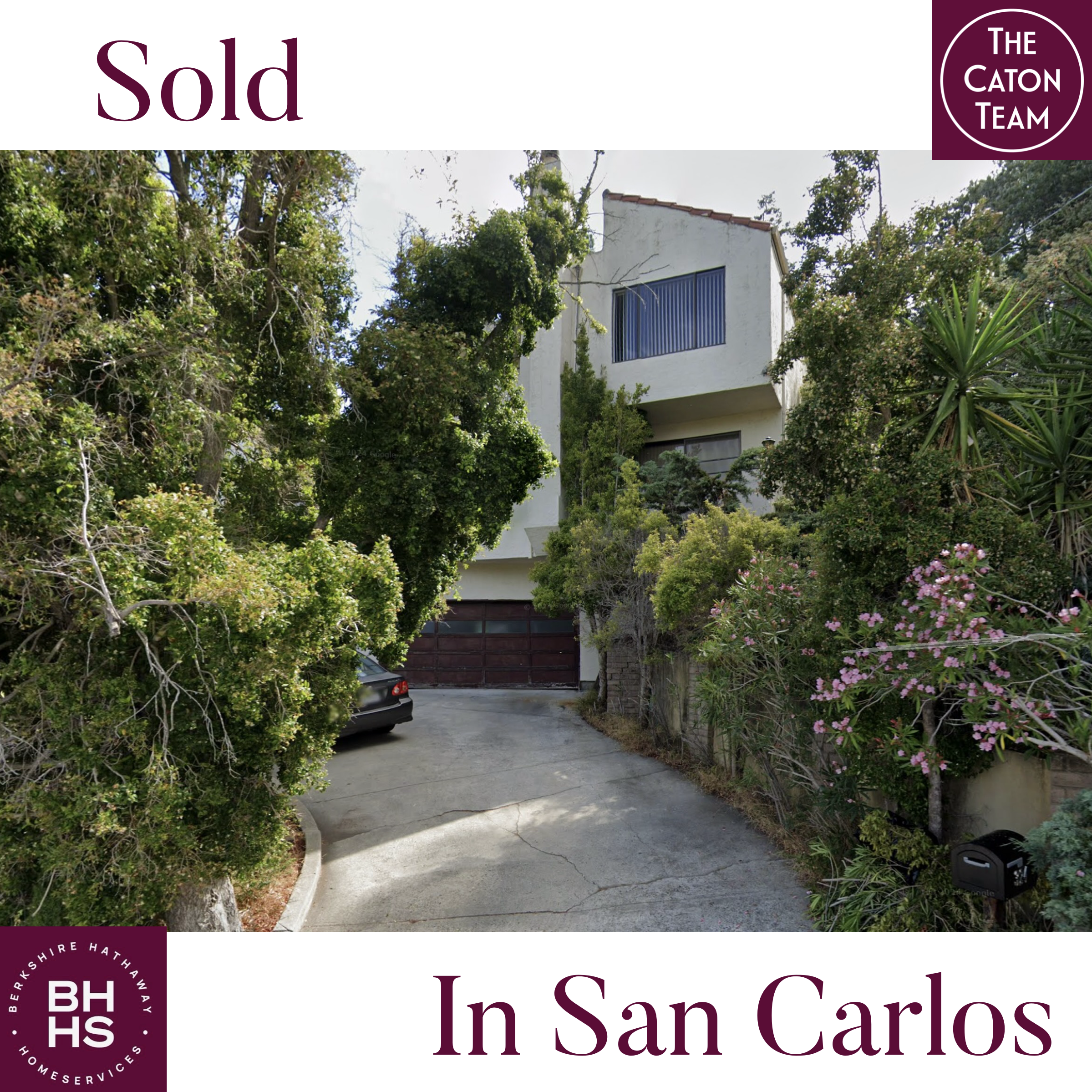

RECENTLY SOLD by THE CATON TEAM

Homes Sold by The Caton Team | Helping Our Buyers Find Their Way Home

Get exclusive inside access when you follow us on Facebook & Instagram

| HOW TO SELL | GET READY CAPITAL – Loans to Prep for Sale | VIRTUAL STAGING | A GUIDE TO BUYING | BUYING INFO | MOVING | TESTIMONIALS |

Got Real Estate Questions? The Caton Team is here to help.

We strive to be more than just Realtors – we are also your home resource. If you have any real estate questions, concerns, need a referral, or need some guidance – we are here for you. Contact us at your convenience – we are but a call, text or click away!

The Caton Team believes, in order to be successful in the San Fransisco | Peninsula | Bay Area | Silicon Valley Real Estate Market we have to think and act differently. We do this by positioning our clients in the strongest light, representing them with the utmost integrity, while strategically maneuvering through negotiations and contracts. Together we make dreams come true.

A mother and daughter-in-law team with over 35 years of combined, local Real Estate experience and knowledge – wouldn’t you like The Caton Team to represent you? Let us know how we can be of service. Contact us any time.

Call | Text | Sabrina 650.799.4333 | Susan 650.796.0654 |EMAIL | WEB| BLOG

The Caton Team – Susan & Sabrina

A Family of Realtors

Effective. Efficient. Responsive.

What can we do for you?

The Caton Team Testimonials | Blog – The Real Estate Beat | TheCatonTeam.com | Facebook | Instagram | HomeSnap | Pinterest | LinkedIn Sabrina

Berkshire Hathaway HomeServices – Drysdale Properties

DRE # |Sabrina 01413526 | Susan 01238225 | Team 70000218 |Office 01499008

The Caton Team does not receive compensation for any posts. Information is deemed reliable but not guaranteed. Third-party information not verified.

You must be logged in to post a comment.