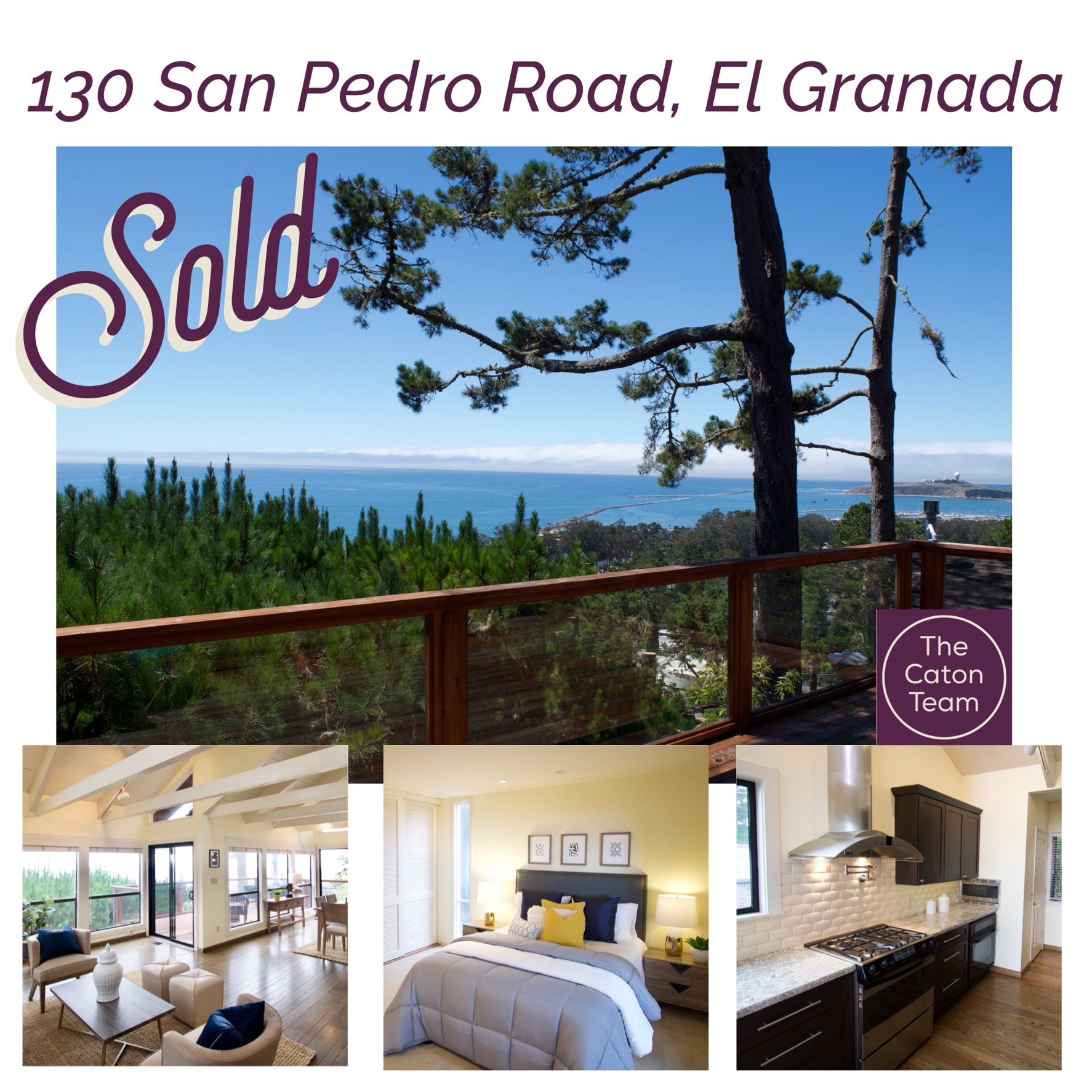

Welcome to 1035 Cherry Street in the heart of San Carlos. From the inviting living room with gas log insert fireplace, the floor-plan seamlessly flows into the open kitchen/dining area and to the back deck. This chefs delight kitchen w/ ample granite countertops, gas range and abundant cabinetry is a vibrant entertaining spot. Step out to the deck and calm backyard for an easy BBQ party or tranquil siesta in the tree shade. The front bedroom is adjacent to an updated bath with shower over tub. The bright primary ensuite retreat includes an updated bath with shower and a reading nook and looks out and opens to the deck and yard. There is abundant potential in the converted garage, now a home office, for additional living or bedroom space. The adjacent laundry room includes a hidden ladder to access attic storage space. Upgrades include on-grid owned solar, tankless water heater, whole house AC, whole house air purifier with UV, attic insulation, crawl space encapsulation and sump pump, replaced sewer lateral, heater, and 2014 roof. Additional features include Nest thermostat & doorbell, hardwood floors, new carpet, double pane windows & door, and back yard storage shed. Prestigious San Carlos District. The home is conveniently located minutes away from exciting Laurel St, parks, Caltrain station and Hwy 101.

Upgrades include:

On-grid owned solar

Tankless water heater

Whole house AC

Whole house air purifier with UV

Attic insulation

Duck Work / Balancing

Crawl space encapsulation and sump pump

Replaced sewer lateral,

Replaced heater

2014 roof

Italian Stone Pine Tree

Drought Tolerant Front Yard Garden

Anderson Poppy Stained Glass Door in Primary

Additional features include:

Nest thermostat & doorbell

Hardwood floors,

New carpet

Double pane windows & door

Back yard storage shed.

Prestigious San Carlos District.

Located minutes away from exciting Laurel St, parks, Caltrain station and Hwy 101.

Call| Text | Sabrina 650.799.4333 |Susan 650.796.0654 | EMAIL | WEB| BLOG

We love what we do and would love to help you navigate your sale or purchase of Residential Real Estate. Please reach out for a personal consultation. Please enjoy our free resources below and get to know our team from our TESTIMONIALS.

Effective. Efficient. Responsive. The Caton Team 🏡 How can The Caton Team help You?

Got Real Estate Questions? The Caton Team is here to help.

We strive to be more than just Realtors – we are also your home resource. If you have any real estate questions, concerns, need a referral, or some guidance – we are here for you. Contact us at your convenience – we are but a call, text or click away!

The Caton Team believes, in order to be successful in the San Fransisco | Peninsula | Bay Area | Silicon Valley Real Estate Market we have to think and act differently. We do this by positioning our clients in the strongest light, representing them with the utmost integrity, while strategically maneuvering through negotiations and contracts. Together we make dreams come true.

A mother and daughter-in-law team with over 35 years of combined, local Real Estate experience and knowledge – wouldn’t you like The Caton Team to represent you? Let us know how we can be of service. Contact us any time.

Call| Text | Sabrina 650.799.4333 | Susan 650.796.0654 | EMAIL | WEB | BLOG

The Caton Team – Susan & Sabrina A Family of Realtors Effective. Efficient. Responsive. What can we do for you?

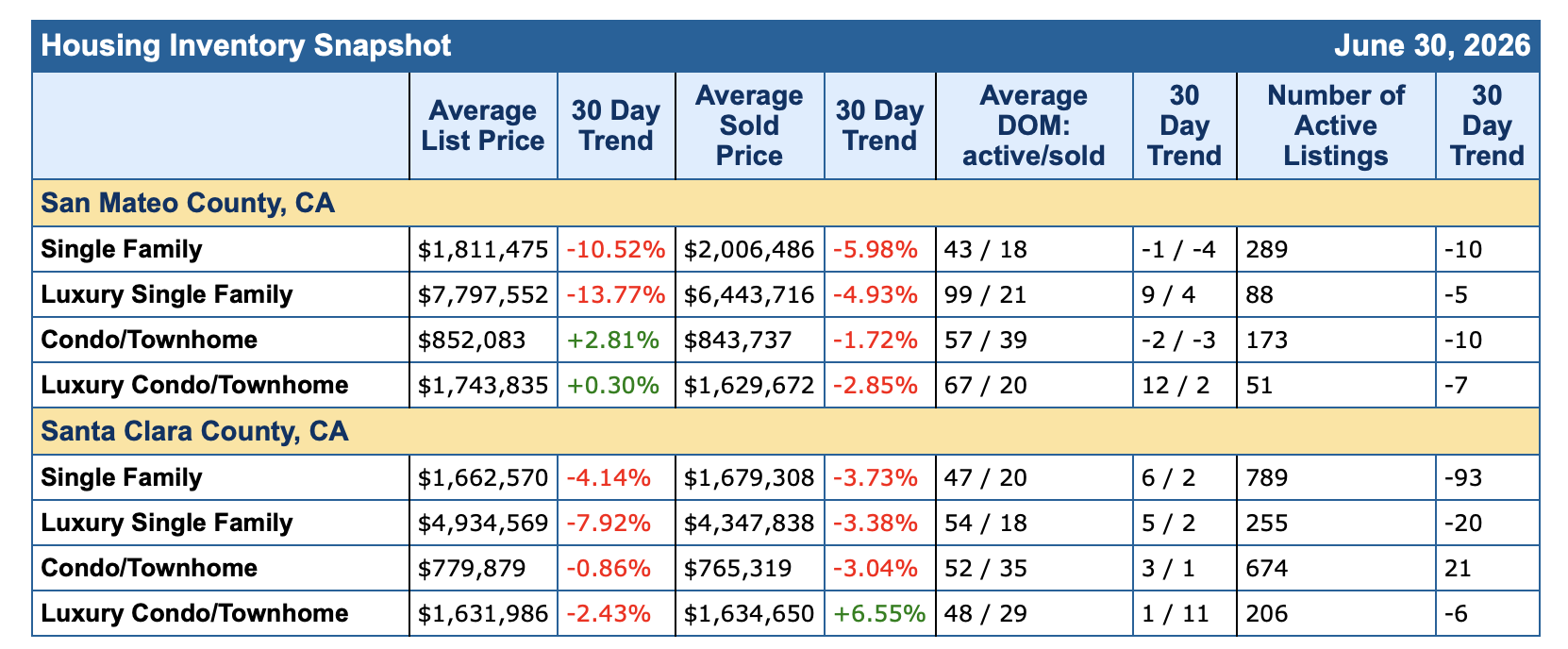

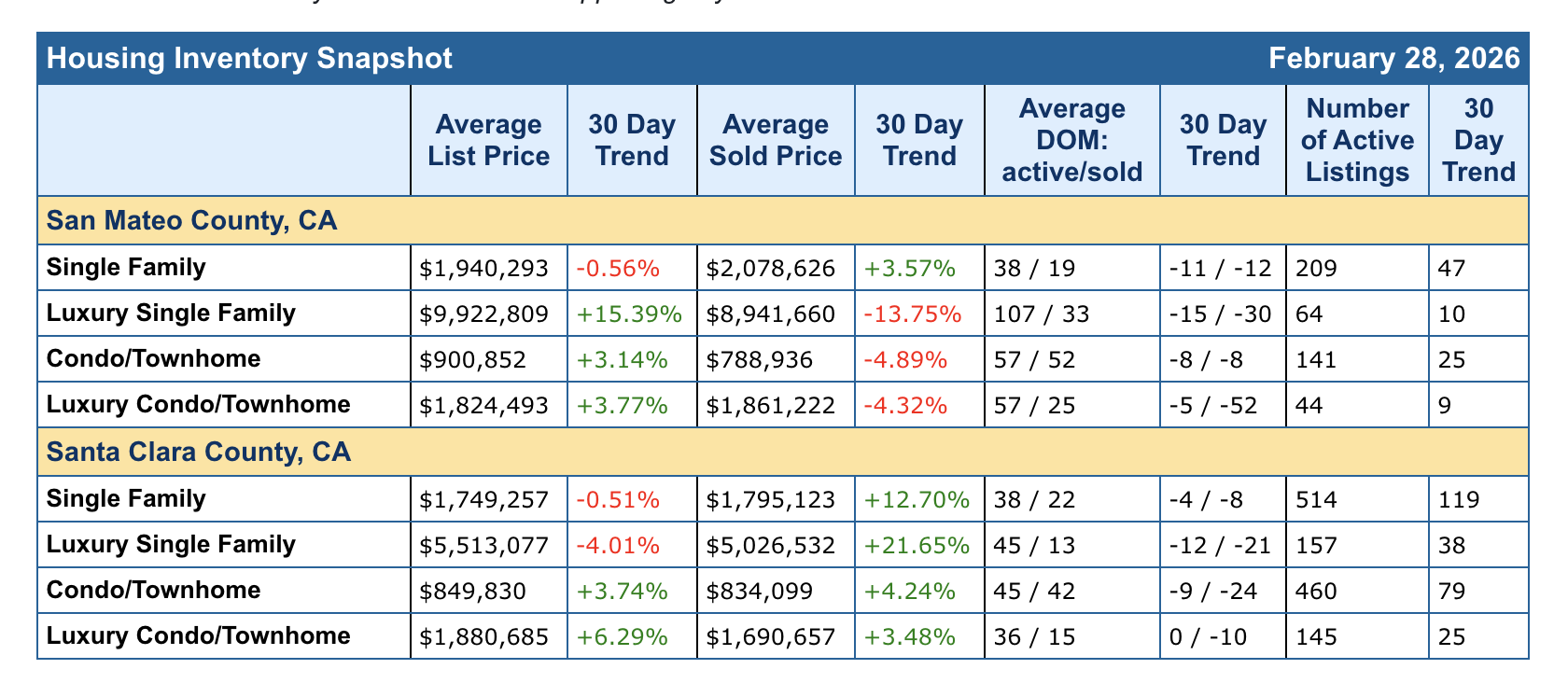

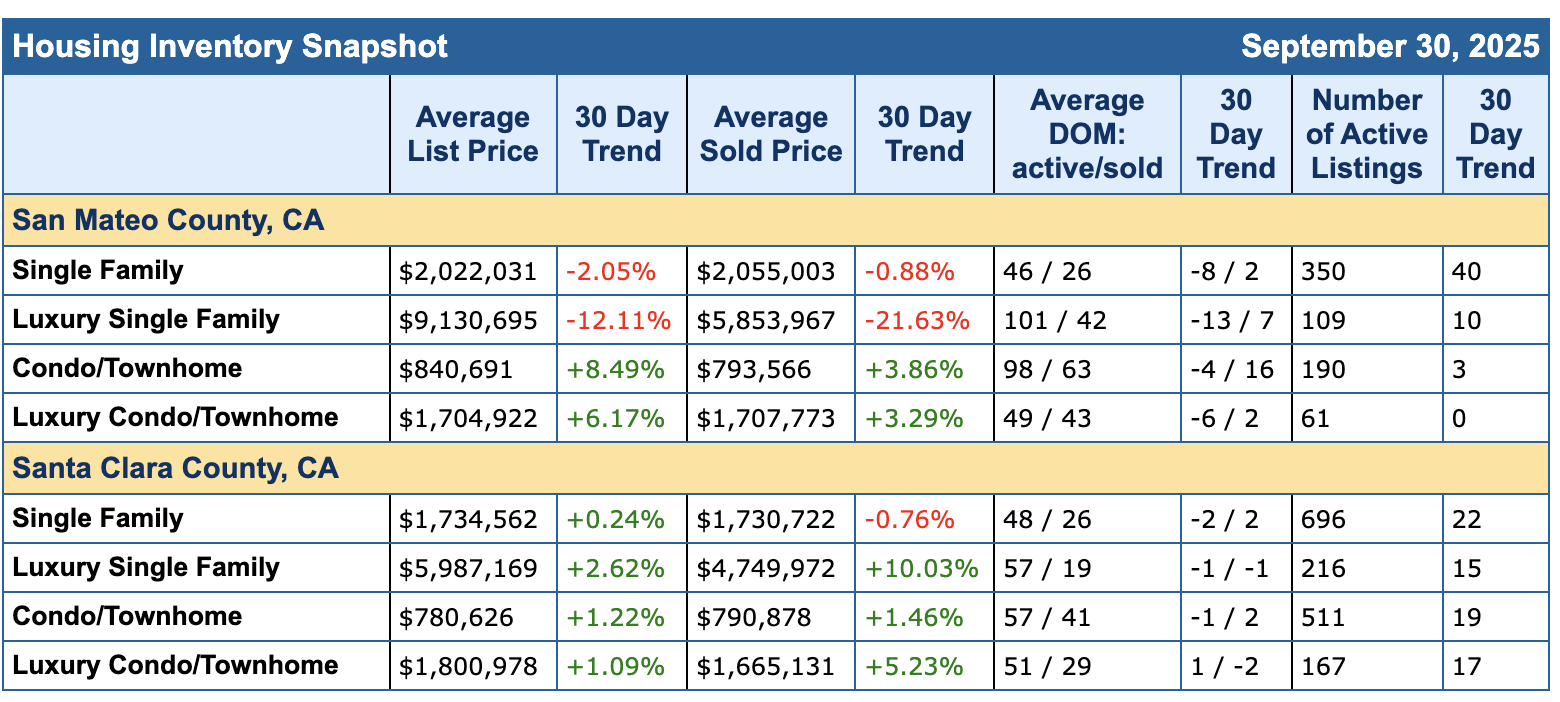

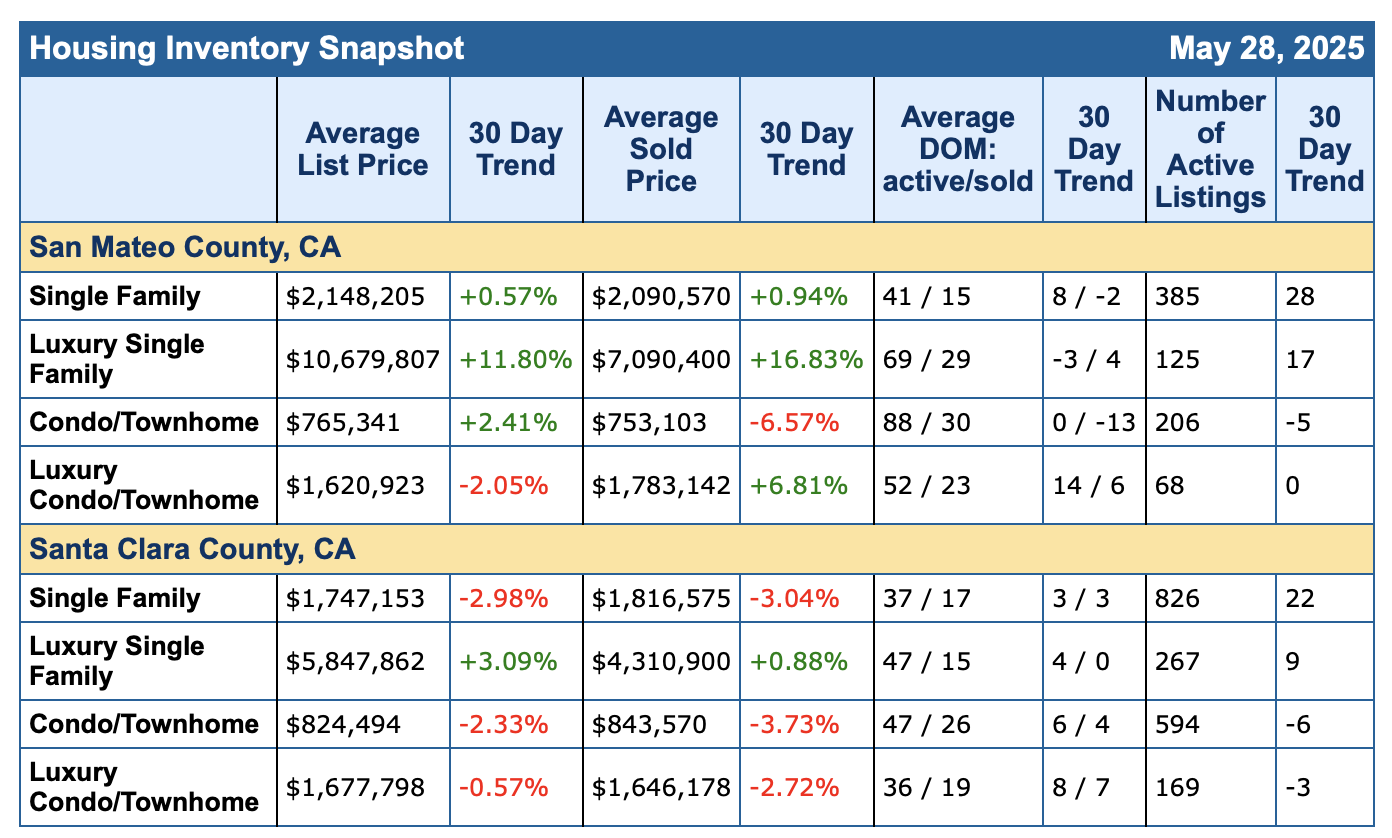

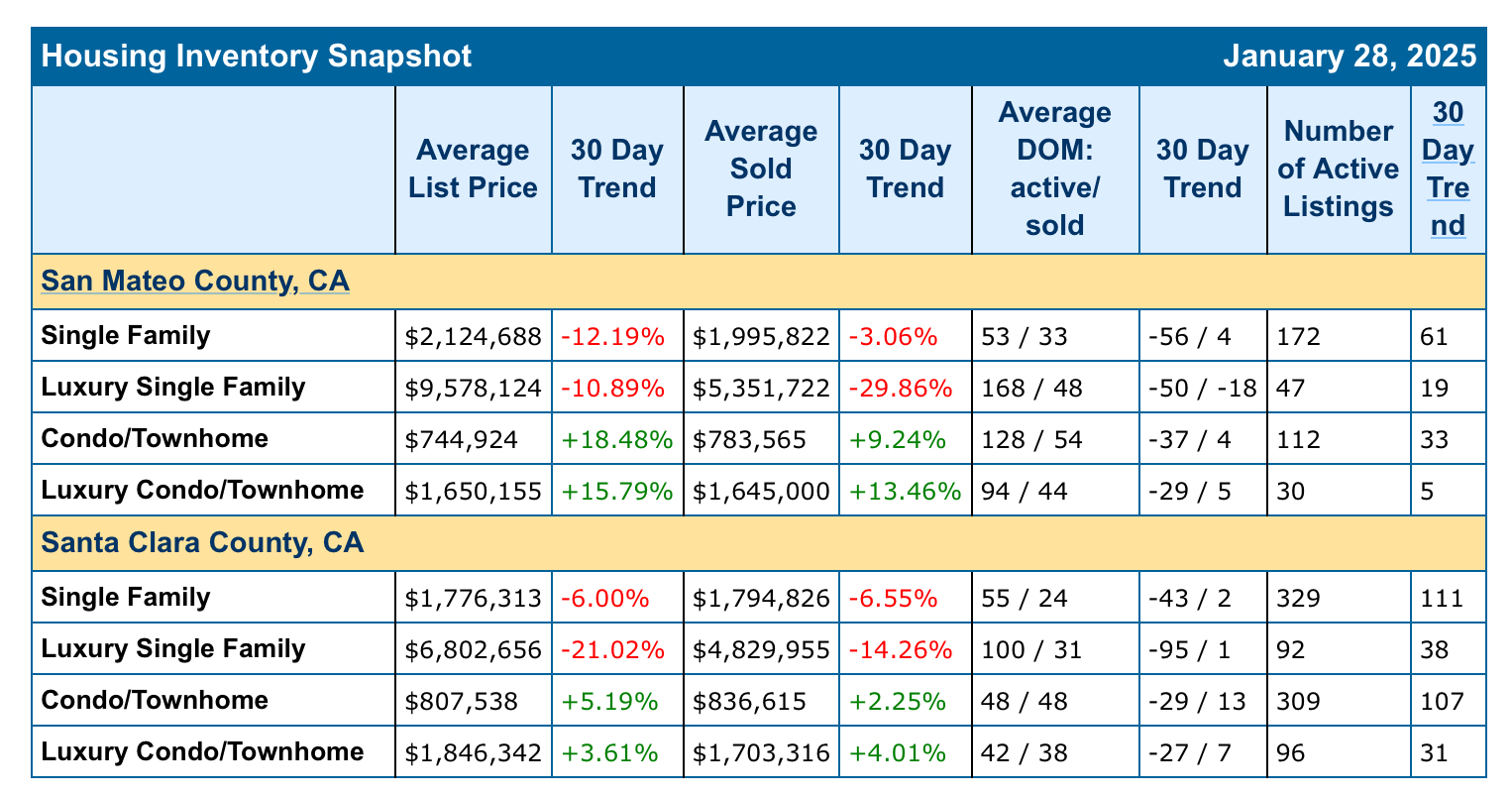

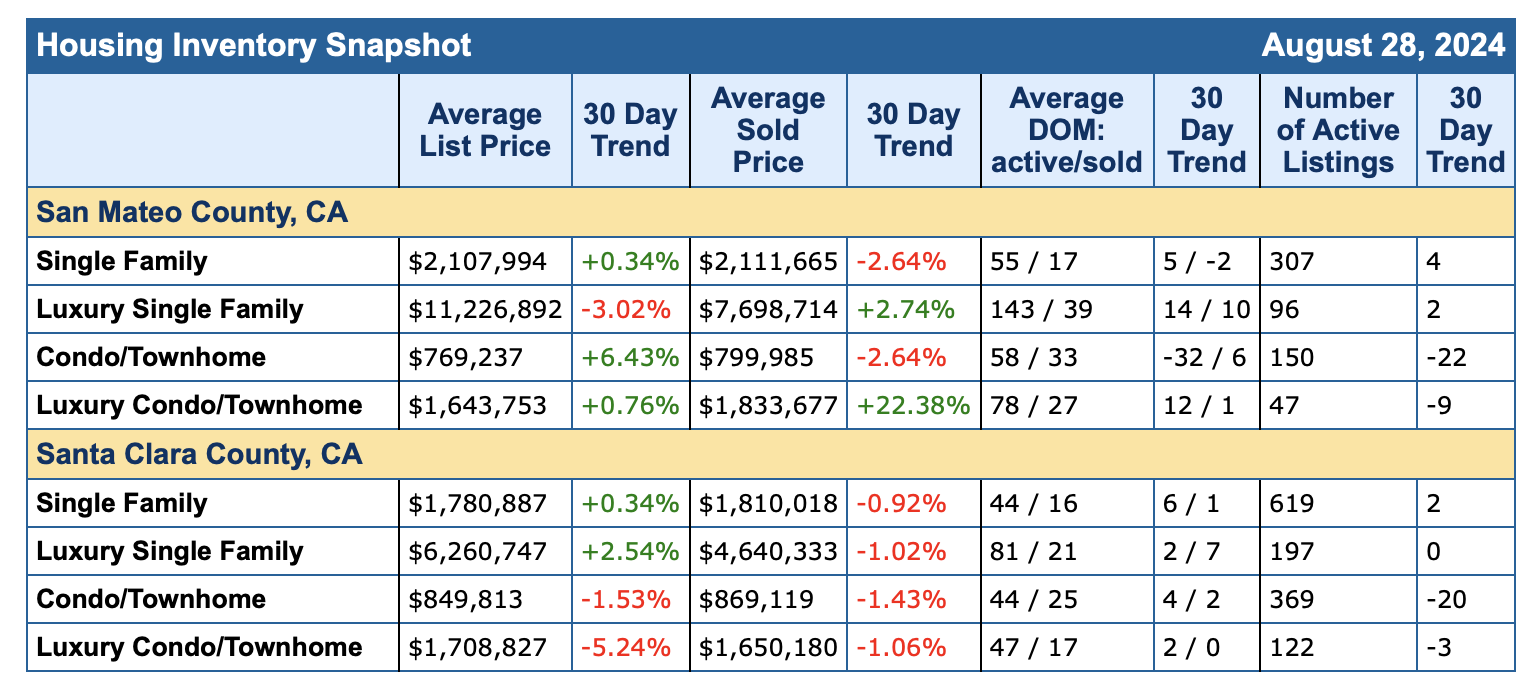

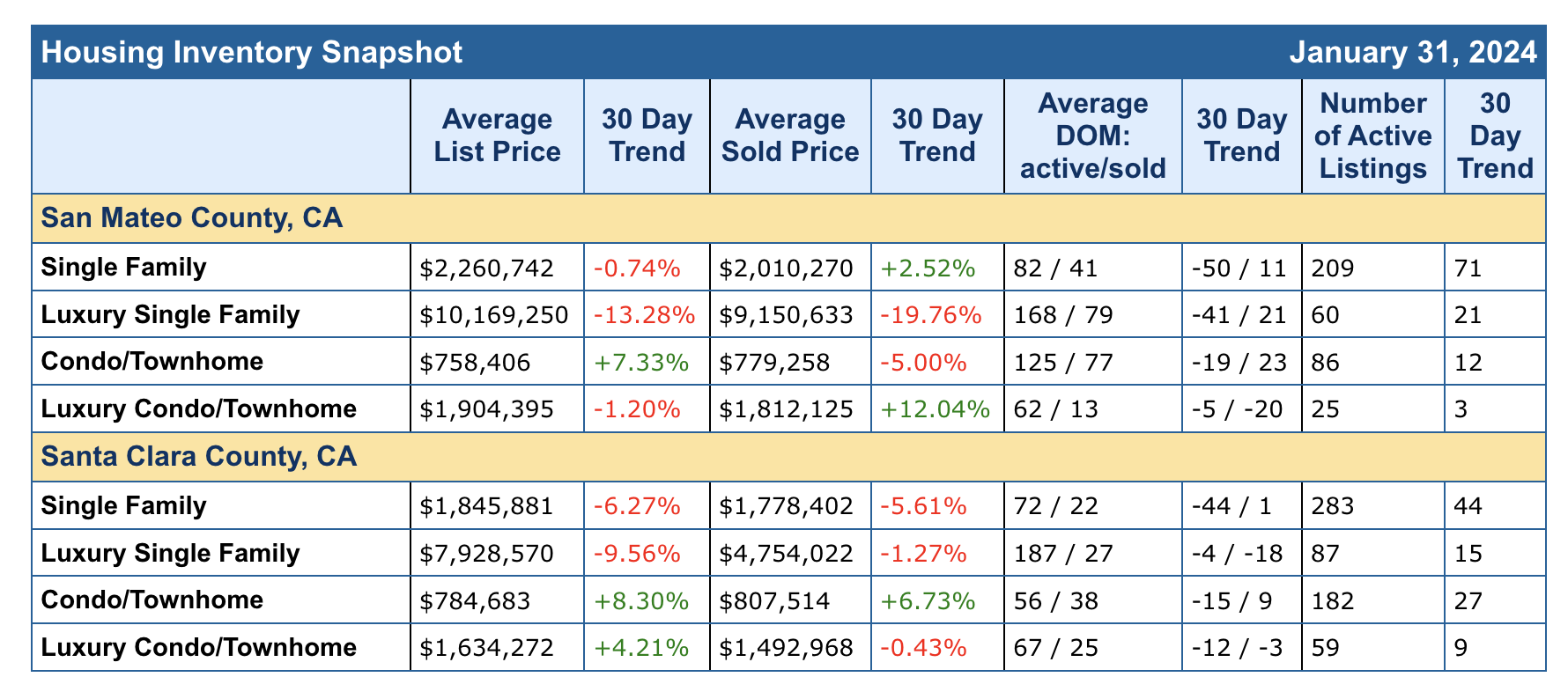

Thank you for tuning in. The stats are in for May and June 2026.

Welp – in May we saw all market points take a dip. With a slight rise in May and June for Condos / Townhomes. Across the board we are seeing a dip in sales. Is it seasonal? Doesn’t feel that way – we often see a good boost in sales each May – as that is the start of selling season and June often holds steady but this year is a bit different. There is so much going on in the world, economically and socially.

With no expected drop in interest rates and the cost of gas and groceries at an all time high. Folks are feeling it. When fear prevails, or concern, we see a dip in sales, and a dip in active buyers. Oddly enough – this sort of data makes the market ripe for buyers but not everyone feels they can take the plunge.

When the market is weird, it is actually a great time to buy in the Bay Area. Some homes still get multiple offers but some do not – and instead of waiting for a price drop – when you work with professional Realtors like The Caton Team – we search those over looked properties – and show them. Don’t wait for a price drop – if you’ve watched a home and it has not sold in 2 -3 weeks – have your agent contact their agent and get the whole picture. We do not wait for price reductions – we are proactive and will see if there is middle ground a buyer and seller can stand on.

With values dipping .8% – 13% – that is a market for buyers! Sellers are not seeing the demand we once had when rates were lower and if a seller has to sell, they are taking a moment to grieve their lost value and hopefully moving forward. The market is the people and what the people are feeling.

If you want to live in the Bay Area, if you have a steady job here and want to grow roots here – NOW – is a great time to buy. There are properties sitting, there are price reductions – this is an opportunity for a buyer to get a house, even under list with contingencies! As long as you see yourself here for about 7-10 years – that is the normal time it takes to see appriciation. The longer you hold onto a home, the better. So when the market is soft and you have long terms goals here – let’s jump in.

The Caton Team provides free buying and selling consultations – to determine the current value of your home if you are selling or if you’re in the market to buy – where you get the most bang for your buck.

Remember, each neighborhood is different, if you are considering a purchase – let us guide you through this and help you find your way home.

If you’re in the market to sell – each area and price point has it’s own pros and cons – let us help you figure out your next steps.

What are your thoughts for the year ahead?

For my selling clients, life changes everyday and if you need to sell your home – let’s come up with a strategy to get you sold! Even in an odd market The Caton Team can help you strategically sell your home. We have before and we will again. We move with the market.

For my buyers, some homes are garnering multiple offers, but some are overlooked. With a little legwork, a buyer can truly find some great opportunities when they align with the market.

If you’re considering a Real Estate move, contact The Caton Team for a free consultation. With over 45+ years of combined Real Estate experience, we have the knowledge and know-how to guide you to your goal. Call us at 650.799.4333 or email us at sabrina_caton@yahoo.com.

Whether you are selling or buying – today or tomorrow – contact The Caton Team – we’re happy to help you achieve your Real Estate goals.

Effective. Efficient. Responsive. The Caton Team 🏡

Each market is unique and with over 45 years of combined Real Estate experience, The Caton Team is more than happy to be of service if and when you are considering a move. Contact us anytime during your journey, together we’ll help you achieve your Real Estate goals.

Got Questions? The Caton Team is here to help.

Call| Text | Sabrina 650.799.4333 |EMAIL | WEB| BLOG

We love what we do and would love to help you navigate your sale or purchase of Residential Real Estate. Please reach out for a personal consultation. Please enjoy our free resources below and get to know our team TESTIMONIALS.

Got Real Estate Questions? The Caton Team is here to help.

We strive to be more than just Realtors – we are also your home resource. If you have any real estate questions, concerns, need a referral, or need some guidance – we are here for you. Contact us at your convenience – we are but a call, text or click away!

The Caton Team believes, in order to be successful in the San Fransisco | Peninsula | Bay Area | Silicon Valley Real Estate Market we have to think and act differently. We do this by positioning our clients in the strongest light, representing them with the utmost integrity, while strategically maneuvering through negotiations and contracts. Together we make dreams come true.

A mother and daughter-in-law team with over 35 years of combined, local Real Estate experience and knowledge – wouldn’t you like The Caton Team to represent you? Let us know how we can be of service. Contact us any time.

Call| Text | Sabrina 650.799.4333 | Susan 650.796.0654 |EMAIL | WEB| BLOG

The Caton Team – Susan & Sabrina A Family of Realtors Effective. Efficient. Responsive. What can we do for you?

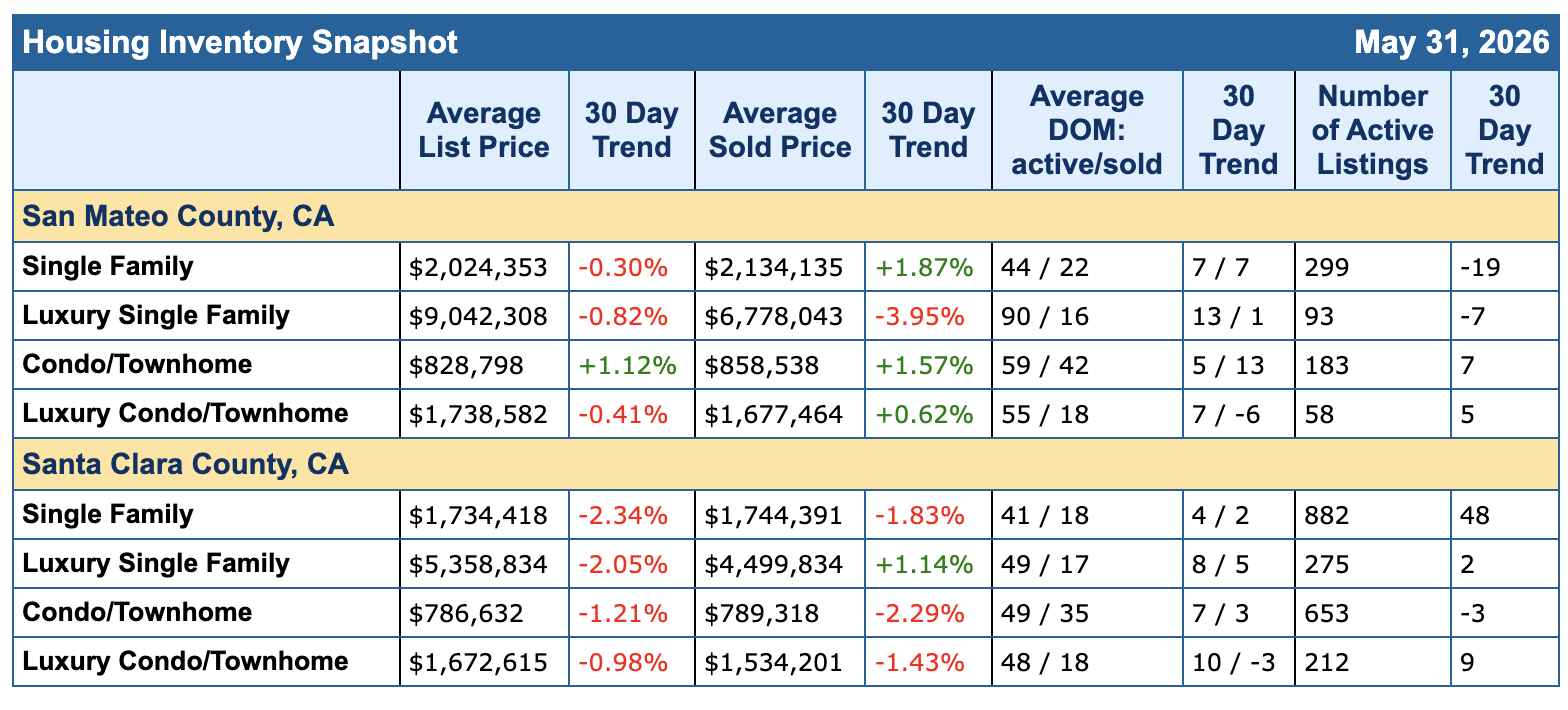

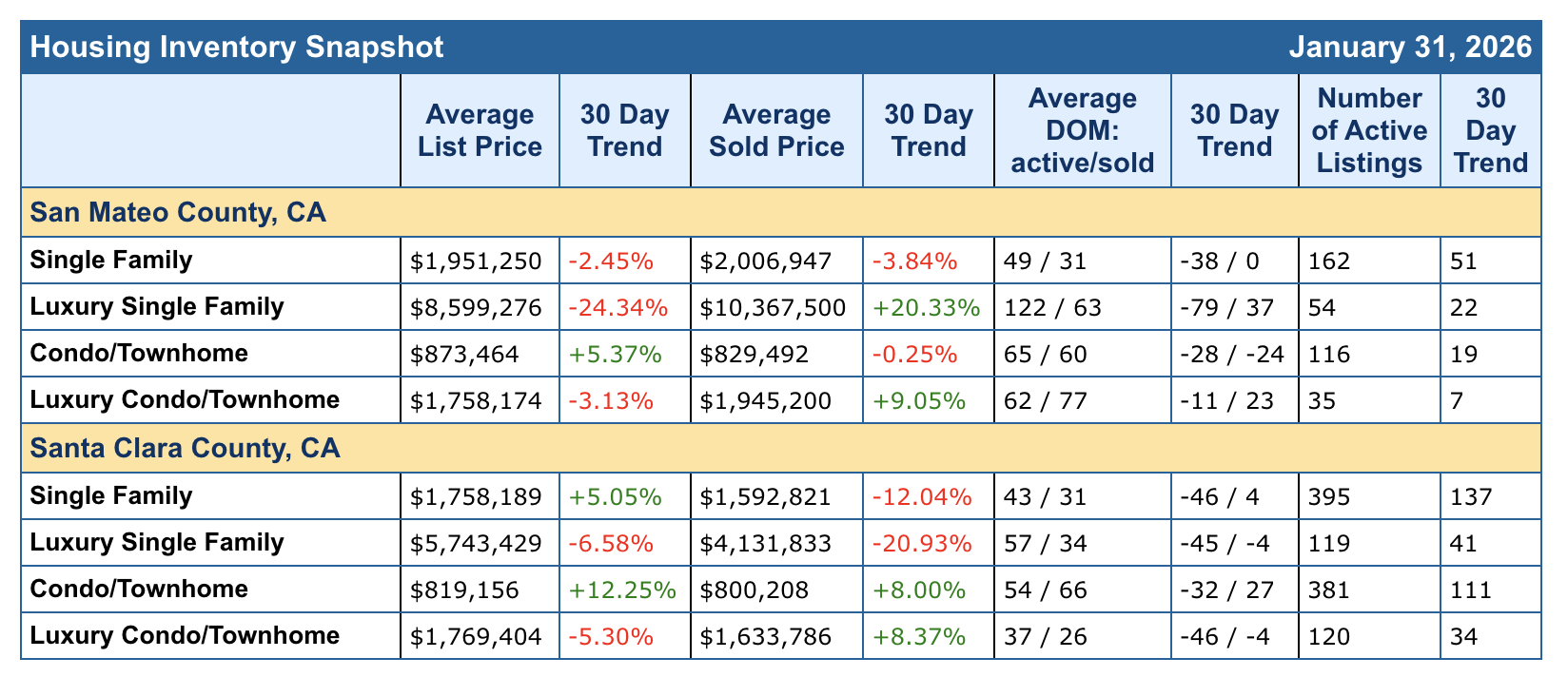

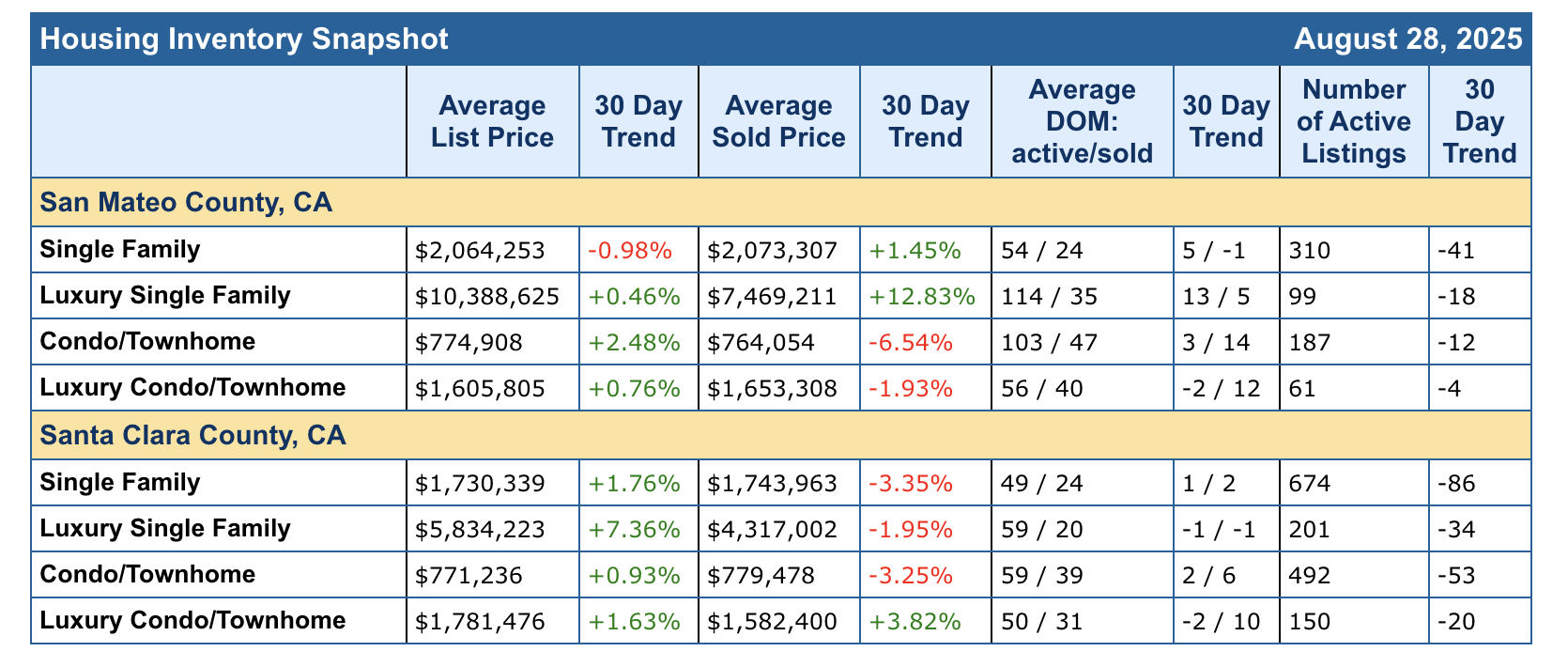

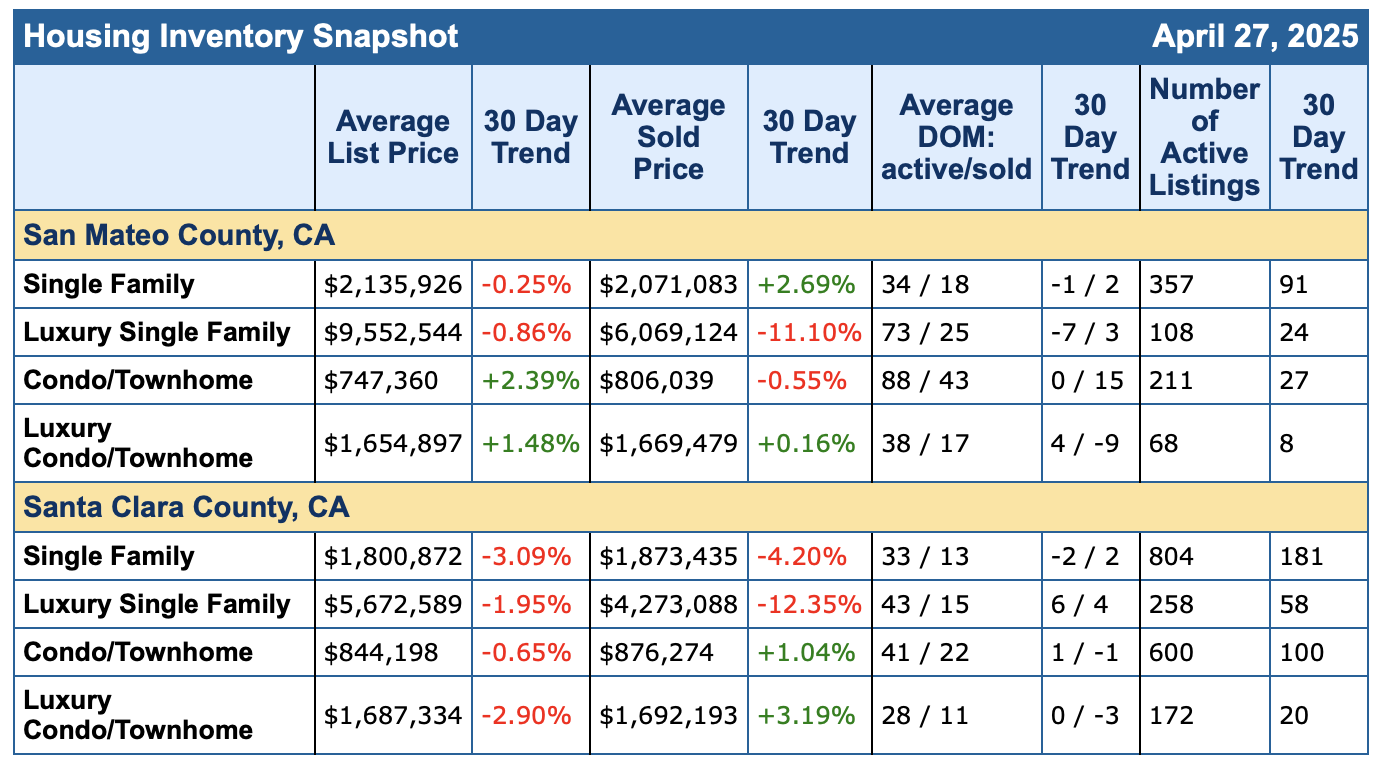

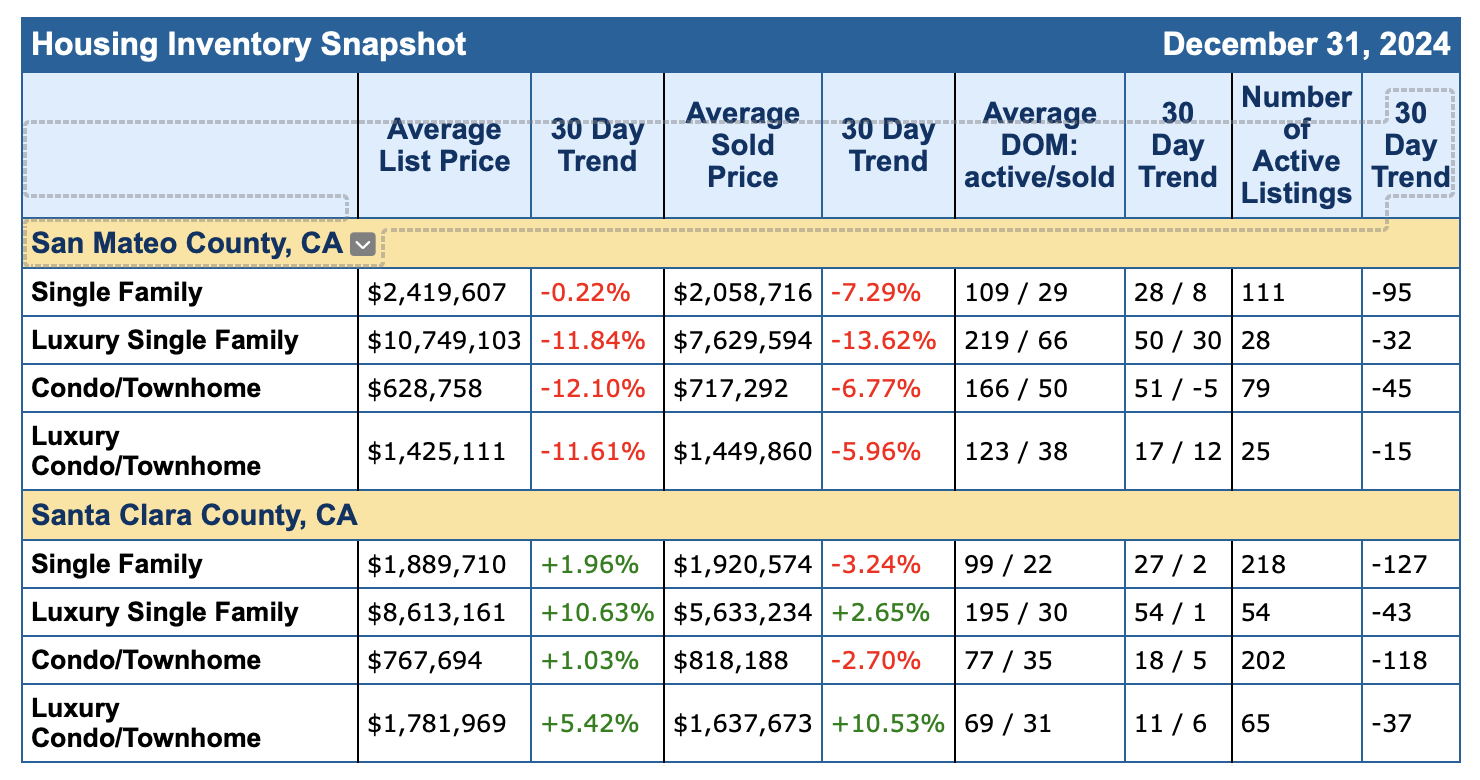

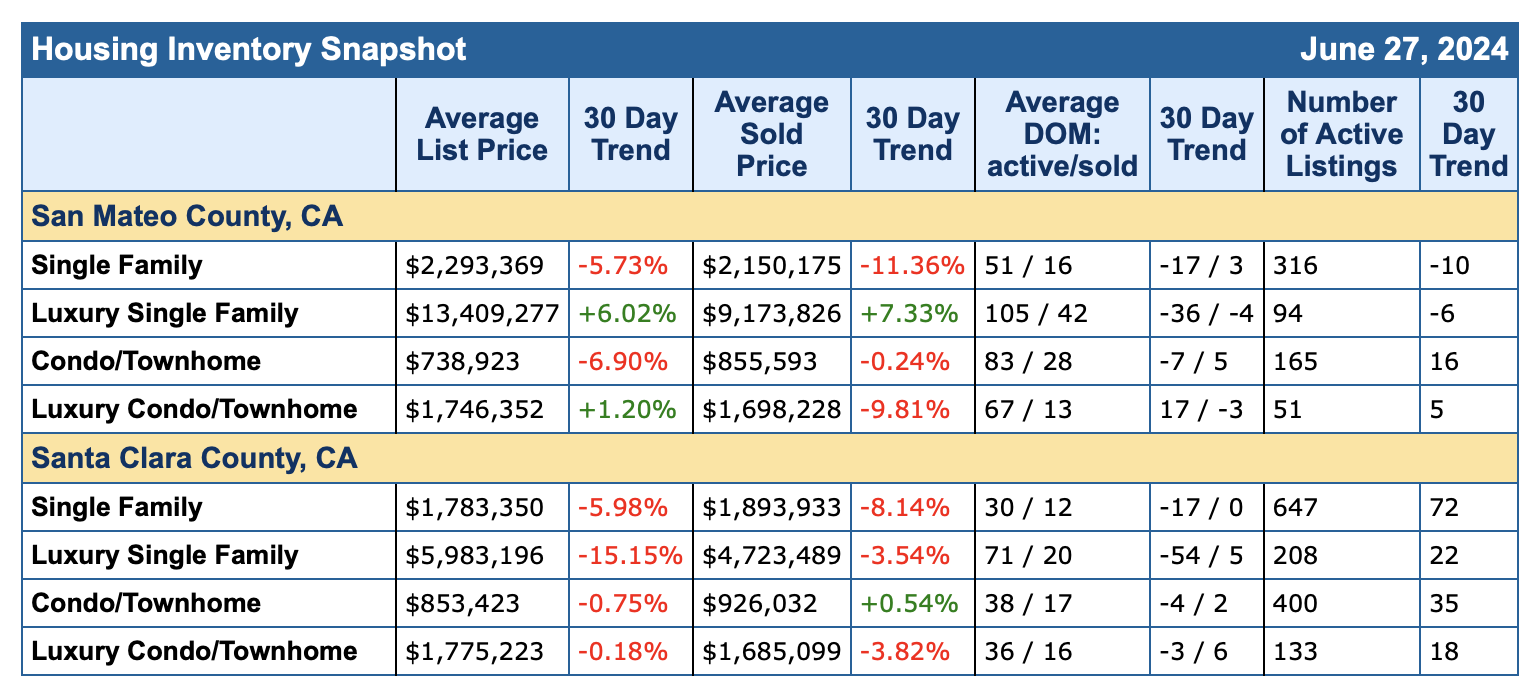

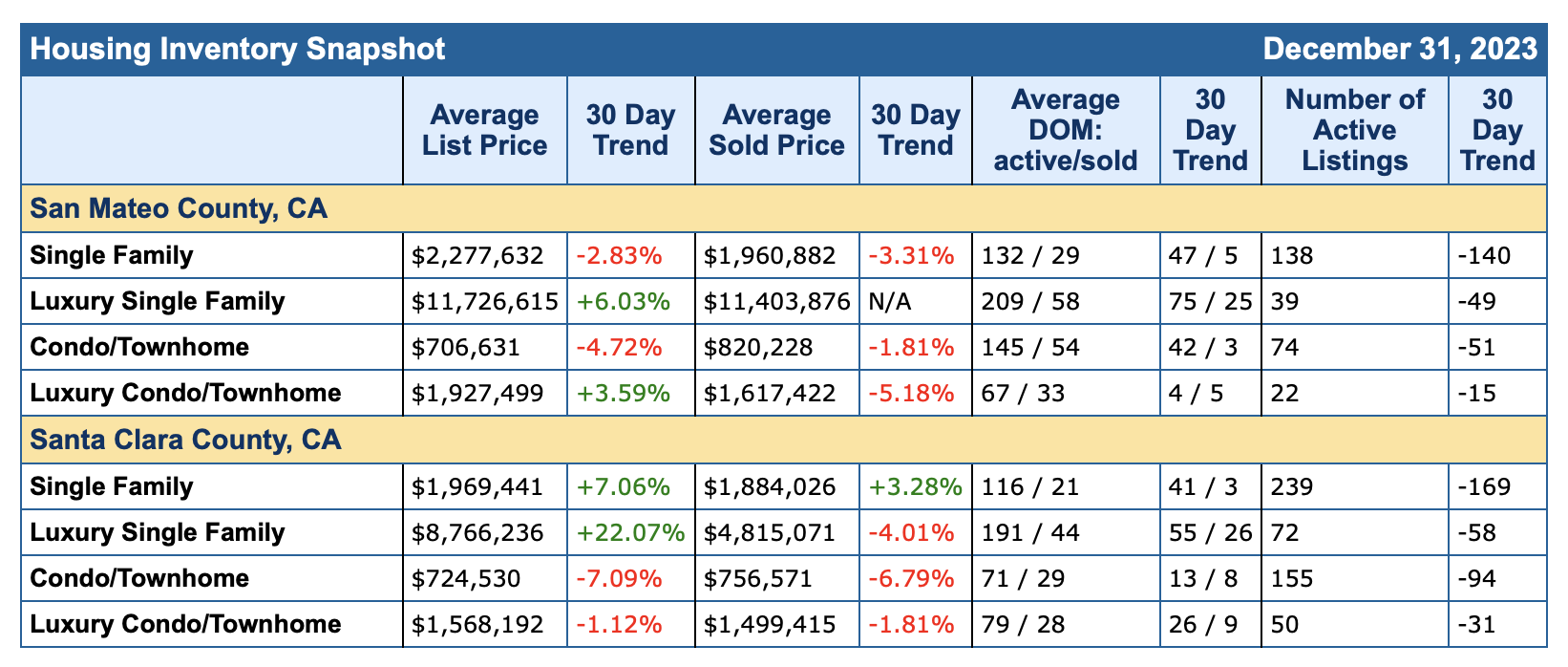

Oddly enough – the high-end sector is doing great! Homes above 2 million are selling and with multiple offers.

However – with the cost of gas and groceries – we’re seeing some adjustment in the market. Interest rates are holding where they are – so no relief in sight for the buyers on that front. Which oddly enough makes it a bit of a buyers market. So keep saving, keep looking and if you are in the market to buy – each neighborhood is different, so let us guide you through this and help you find your way home.

If you’re in the market to sell – each area and price point has it’s own pros and cons – let us help you figure out your next steps.

What are your thoughts for the year ahead?

For my selling clients, life changes everyday and if you need to sell your home – let’s come up with a strategy to get you sold! Even in an odd market The Caton Team can help you strategically sell your home.

For my buyers, some homes are garnering multiple offers, but some are overlooked. With a little legwork, a buyer can truly find some great opportunities when they align with the market.

If you’re considering a Real Estate move, contact The Caton Team for a free consultation. With over 45+ years of combined Real Estate experience, we have the knowledge and know-how to guide you to your goal. Call us at 650.799.4333 or email us at info@TheCatonTeam.com.

Whether you are selling or buying – today or tomorrow – contact The Caton Team – we’re happy to help you achieve your Real Estate goals.

Effective. Efficient. Responsive. The Caton Team 🏡

Each market is unique and with over 40 years of combined Real Estate experience, The Caton Team is more than happy to be of service if and when you are considering a move. Contact us anytime during your journey, together we’ll help you achieve your Real Estate goals.

Got Questions? The Caton Team is here to help.

Call| Text | Sabrina 650.799.4333 |EMAIL | WEB| BLOG

We love what we do and would love to help you navigate your sale or purchase of Residential Real Estate. Please reach out for a personal consultation. Please enjoy our free resources below and get to know our team TESTIMONIALS.

Got Real Estate Questions? The Caton Team is here to help.

We strive to be more than just Realtors – we are also your home resource. If you have any real estate questions, concerns, need a referral, or need some guidance – we are here for you. Contact us at your convenience – we are but a call, text or click away!

The Caton Team believes, in order to be successful in the San Fransisco | Peninsula | Bay Area | Silicon Valley Real Estate Market we have to think and act differently. We do this by positioning our clients in the strongest light, representing them with the utmost integrity, while strategically maneuvering through negotiations and contracts. Together we make dreams come true.

A mother and daughter-in-law team with over 35 years of combined, local Real Estate experience and knowledge – wouldn’t you like The Caton Team to represent you? Let us know how we can be of service. Contact us any time.

Call| Text | Sabrina 650.799.4333 | Susan 650.796.0654 |EMAIL | WEB| BLOG

The Caton Team – Susan & Sabrina A Family of Realtors Effective. Efficient. Responsive. What can we do for you?

Renting is cheaper than buying a home, according to senior housing economists.

“Rent continues to fall in many of the major metros across the United States for a variety of reasons,” explains Joel Berner, a senior economist at Realtor.com®. “The biggest one is that rent is still correcting itself from the dramatic run-up of 2021 and 2022, when several years’ worth of rent gains were seen over the span of a few months.”

Why is renting cheaper than buying?

The national average rent across the top 50 metro areas fell to $1,672—$85 (-4.8%) lower than its summer 2022 peak but $221 (15.2%) higher than its pre-pandemic level.

While renting remains cheaper than buying, with a median mortgage payment of $2,040 versus $1,672 for rent, the gap is narrowing due to lower mortgage rates, making homeownership more appealing for some buyers.

National median asking rent by unit size

In January 2026, the median asking rent for studios fell by -1.2%, marking the 29th consecutive month of annual declines. The median rent of studios was $1,393 in January, down by $86 (-5.8%) from its peak seen in October 2022. Nevertheless, the median asking rent for studios was still $128 (10.1%) higher than six years ago. Realtor.com

Rents on studio units haven’t fallen much, down just 1.2%, indicating that more people are renting solo.

Meanwhile, one- and two-bedroom units have seen a slightly larger drop, around 1.4% to 1.7%.

Mortgage vs. rent calculator

If you’re still renting but looking to buy a home, a good place to start evaluating your finances is by using a mortgage vs. rent calculator.

The tool will allow you to compare your current rent versus what you have saved for a down payment and what your mortgage payments would be.

“By offering personalized insights, the calculator empowers consumers to evaluate not only the best option for their current situation but also how the decision could impact their finances in the years to come,” says Realtor.com economist Jiayi Xu.

We love what we do and would love to help you navigate your sale or purchase of Residential Real Estate. Please reach out for a personal consultation. Please enjoy our free resources below and get to know our team from our TESTIMONIALS.

Effective. Efficient. Responsive. The Caton Team 🏡

Got Real Estate Questions? The Caton Team is here to help.

We strive to be more than just Realtors – we are also your home resource. If you have any real estate questions, concerns, need a referral, or some guidance – we are here for you. Contact us at your convenience – we are but a call, text, or click away!

The Caton Team believes, in order to be successful in the San Francisco | Peninsula | Bay Area | Silicon Valley Real Estate Market, we have to think and act differently. We do this by positioning our clients in the strongest light, representing them with the utmost integrity, while strategically maneuvering through negotiations and contracts. Together we make dreams come true.

A mother and daughter-in-law team with over 35 years of combined local Real Estate experience and knowledge – wouldn’t you like The Caton Team to represent you? Let us know how we can be of service. Contact us any time.

Cell | Sabrina 650.799.4333 | Susan 650.796.0654 | EMAIL | WEB| BLOG

The Caton Team – Susan & Sabrina A Family of Realtors Effective. Efficient. Responsive. What can we do for you?

Berkshire Hathaway HomeServices – Drysdale Properties, Redwood City Ca.

DRE # | Sabrina 01413526 | Susan 01238225 | Team 70000218 | Office 01499008

The Caton Team does not receive compensation for any posts. Information is deemed reliable but not guaranteed. Third-party information not verified. We are licensed to assist our clients with their Real Estate needs. We do not provide legal or financial advice, directly or implied. Please seek the appropriate counsel.

Hello Readers – I wanted to share that effective December 2025 – California homeowners need to think ahead about fire safety.

Defensible Space is crucial for your home’s wildfire safety. It’s the buffer zone you create between your property and the surrounding wildland area. This space is key to slowing or stopping wildfire spread and protecting your home from embers, flames, or heat. It also gives firefighters a safer area to defend your property.

The first five feet from your home is the most important. Keeping the area closest to buildings, structures, and decks clear will prevent embers from igniting materials that can spread the fire to your home.

Why? Learn more about the importance of Zone 0 and the scientific research that demonstrates the importance of this zone with the (Zone 0 At-A-Glance)

What to do:

Use hardscape like gravel, pavers, or concrete. No combustible bark or mulch.

Remove all dead and dying plants, weeds, and debris (leaves, needles, etc.) from your roof, gutter, deck, porch, stairways, and under any areas of your home.

Remove all branches within 10 feet of any chimney or stovepipe outlet.

Limit combustible items (like outdoor furniture and planters) on top of decks.

Relocate firewood and lumber to Zone 2.

Replace combustible fencing, gates, and arbors attached to the home with noncombustible alternatives.

Consider relocating garbage and recycling containers outside this zone.

Consider relocating boats, RVs, vehicles, and other combustible items outside this zone.

Regularly clear dead or dry vegetation and create space between trees. During times of drought when watering is limited, pay special attention to clearing dead or dying material.

Why? Removing dead plants and creating space between trees and shrubs creates a buffer for your property and reduces potential fuel for fire.

What to do:

Remove all dead plants, grass, and weeds.

Remove dead or dry leaves and pine needles.

Trim trees regularly to keep branches a minimum of 10 feet from other trees.

Create a separation between trees, shrubs, and items that could catch fire, such as patio furniture, wood piles, swing sets, etc.

Continue reducing potential fuel within 100 feet or the property line.

Why? 100 feet of defensible space is required by law. Public Resources Code (PRC) 4291

What to do:

Cut or mow annual grass down to a maximum height of four inches.

Create horizontal space between shrubs and trees. (See diagram)

Create vertical space between grass, shrubs and trees. (See diagram)

Remove fallen leaves, needles, twigs, bark, cones, and small branches. However, they may be permitted to a depth of three inches.

Keep 10 feet of clearance around exposed wood piles, down to bare mineral soil, in all directions.

Clear areas around outbuildings and propane tanks. Keep 10 feet of clearance to bare mineral soil and no flammable vegetation for an additional 10 feet around their exterior.

Maintain space between the lowest tree branches and the ground or shrubs.

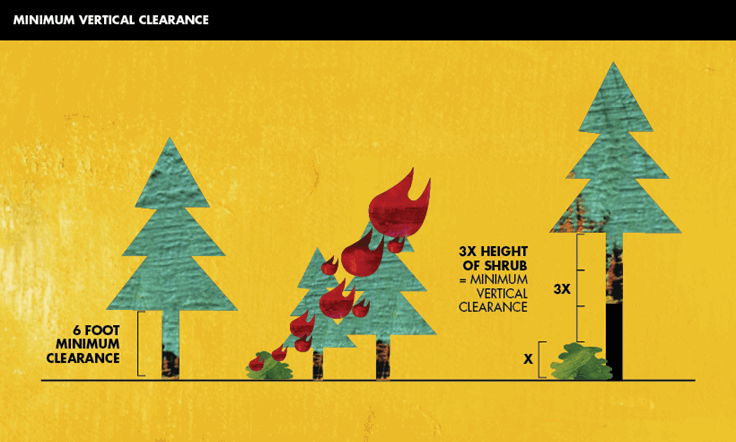

Remove all tree branches at least six feet from the ground.

Allow extra vertical space between shrubs and trees. Lack of vertical space can allow a fire to move from the ground to the brush to the treetops like a ladder. This leads to more intense fire closer to your home.

Keep at least three times the height of any shrubs between the shrubs and the lowest branches of trees.

Example: A 5-foot shrub is growing near a tree. 15 feet of clearance is needed between the top of the shrub and the lowest tree branch.

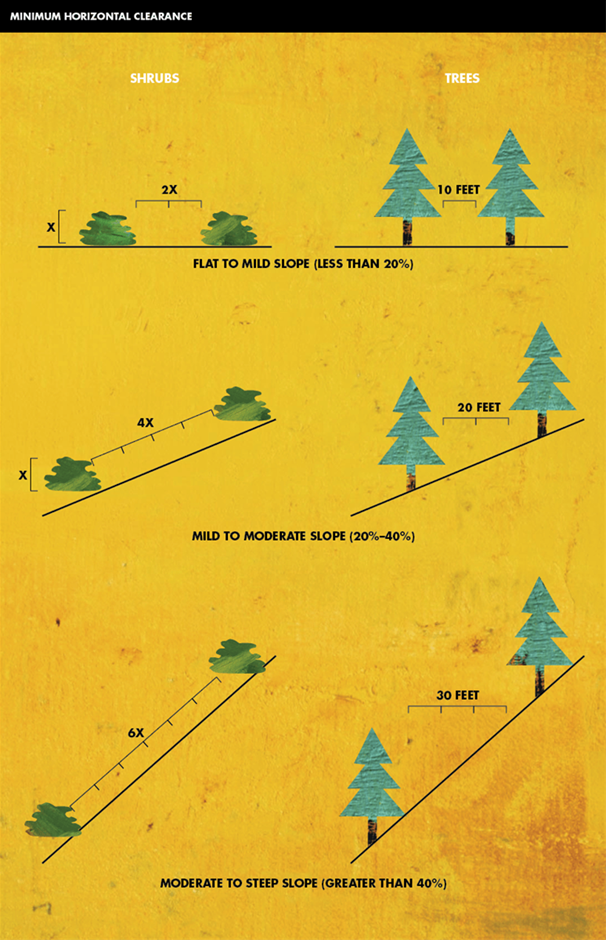

How much space should you leave between trees or shrubs?

Horizontal space depends on the slope of the land and the height of the shrubs or trees. Leave more space between vegetation on bigger slopes. Refer to the chart below to determine spacing distance.

Space between shrubs:

Flat or mild slope (less than 20%): Two times the height of the shrub.

Mild to moderate slope (20-40%): Four times the height of the shrub

Moderate to steep slope (greater than 40%): Six times the height of the shrub

Space between trees:

Flat or mild slope (less than 20%): 10 feet.

Mild to moderate slope (20-40%): 20 feet.

Moderate to steep slope (greater than 40%): 30 feet.

We love what we do and would love to help you navigate your sale or purchase of Residential Real Estate. Please reach out for a personal consultation. Please enjoy our free resources below and get to know our team from our TESTIMONIALS.

Effective. Efficient. Responsive. The Caton Team 🏡

Got Real Estate Questions? The Caton Team is here to help.

We strive to be more than just Realtors – we are also your home resource. If you have any real estate questions, concerns, need a referral, or some guidance – we are here for you. Contact us at your convenience – we are but a call, text, or click away!

The Caton Team believes, in order to be successful in the San Francisco | Peninsula | Bay Area | Silicon Valley Real Estate Market, we have to think and act differently. We do this by positioning our clients in the strongest light, representing them with the utmost integrity, while strategically maneuvering through negotiations and contracts. Together we make dreams come true.

A mother and daughter-in-law team with over 35 years of combined local Real Estate experience and knowledge – wouldn’t you like The Caton Team to represent you? Let us know how we can be of service. Contact us any time.

Cell | Sabrina 650.799.4333 | Susan 650.796.0654 | EMAIL | WEB| BLOG

The Caton Team – Susan & Sabrina A Family of Realtors Effective. Efficient. Responsive. What can we do for you?

Berkshire Hathaway HomeServices – Drysdale Properties, Redwood City Ca.

DRE # | Sabrina 01413526 | Susan 01238225 | Team 70000218 | Office 01499008

The Caton Team does not receive compensation for any posts. Information is deemed reliable but not guaranteed. Third-party information not verified. We are licensed to assist our clients with their Real Estate needs. We do not provide legal or financial advice, directly or implied. Please seek the appropriate counsel.

I am sharing this article from Malwarebytes as tech security is so important these days. I read this article HERE. by Pieter Arntz

Scammers have found a way to abuse legitimate Apple account notification emails to trick targets into calling fake tech support numbers.

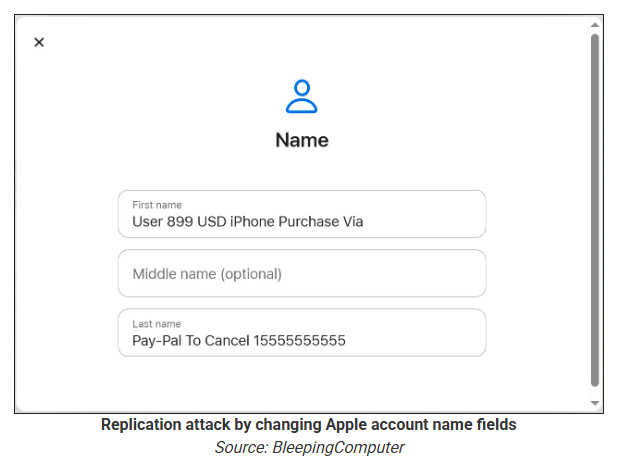

According to a report from BleepingComputer, scammers create an Apple account and insert a phishing message into the personal information fields, then modify the account so that Apple sends a genuine security alert about the change to the target.

BleepingComputer was able to replicate the attack.

The attacker creates an Apple ID they control, then stuffs the phishing message into the personal information fields (first name, last name, possibly address), splitting it across fields because they will not fit into just one.

To launch the phish, the attacker changes something benign on their specially created Apple account, such as shipping information, which causes Apple’s systems to send a “Your Apple account was updated” security email.

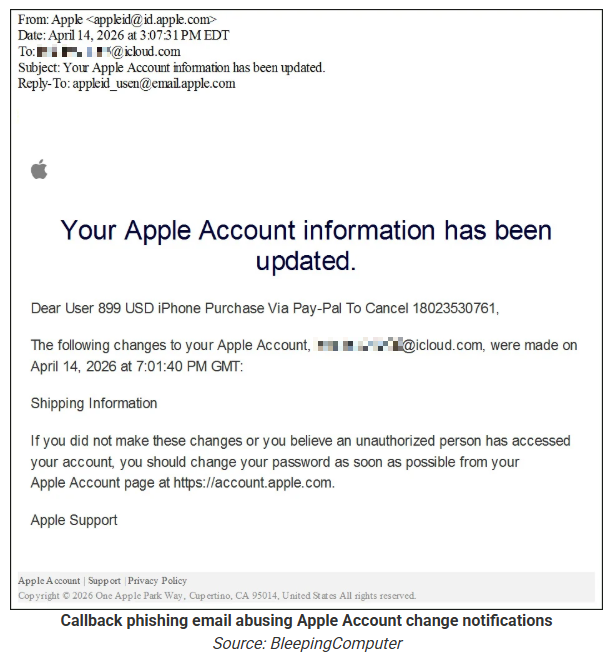

While the original alert is addressed to the attacker’s iCloud email, they are then able to redistribute it to a wider victim list, for example through a mailing list.

In the copy the targets receive, the email headers still show a legitimate Apple sender, and the presence of the attacker’s iCloud address can even make it look like “someone else” has gained access to the account.

Because Apple includes those user-supplied fields in the security email, the phishing text is delivered inside a legitimate message sent from Apple’s own infrastructure.

This method, called call-back phishing, filters out suspicious users, so the scammers can focus on the people who fell for the first part.

The emails come from a legitimate source, sail through every security filter because of that, and look convincing enough to scare the receiver into thinking someone spent $899 from their PayPal account.

But the structure of the email does not make sense.

“Dear User” is immediately followed by the scam message where your name should have been. The header says it’s about account information rather than a purchase. And the iCloud account does not belong to the recipient. So, once you know how it’s done, they’re not impossible to spot. Which is why we wrote this blog.

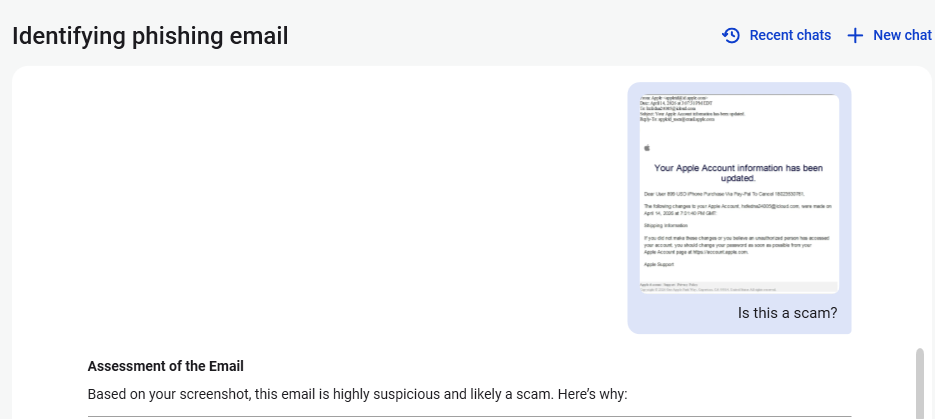

And when in doubt, you can always ask Malwarebytes Scam Guard.

Scam or legit? Scam Guard knows.

Asking Scam Guard

Scam Guard identified the screenshot as a scam and guides users through the next steps.

Scams like these work, because many users still view phone calls as more trustworthy than email, especially if the email itself passed all the usual technical authenticity checks and they initiated the call themselves.

How to stay safe

Tech support scammers will try to convince callers to install some kind of remote desktop application to steal data from your computer, or ask for financial details so they can steal your money.

To stay safe from these scammers:

Be wary of unexpected alerts about high‑value purchases you do not recognize. They are suspicious even if they come from a real domain.

Never call a number sent to you by unsolicited means or even found in sponsored search results.

Carefully read emails and text messages, even if they come form trustworthy addresses. Does the email make sense from a structural and linguistic point of view?

If someone claiming to be support for a legitimate company asks for remote access or payment details during a call, hang up and contact the company through official channels.

Use Malwarebytes Scam Guard to analyze any kind of message that alarms you or urges you to take immediate action.

We love what we do and would love to help you navigate your sale or purchase of Residential Real Estate. Please reach out for a personal consultation. Please enjoy our free resources below and get to know our team from our TESTIMONIALS.

Effective. Efficient. Responsive. The Caton Team 🏡

Got Real Estate Questions? The Caton Team is here to help.

We strive to be more than just Realtors – we are also your home resource. If you have any real estate questions, concerns, need a referral, or some guidance – we are here for you. Contact us at your convenience – we are but a call, text, or click away!

The Caton Team believes, in order to be successful in the San Francisco | Peninsula | Bay Area | Silicon Valley Real Estate Market, we have to think and act differently. We do this by positioning our clients in the strongest light, representing them with the utmost integrity, while strategically maneuvering through negotiations and contracts. Together we make dreams come true.

A mother and daughter-in-law team with over 35 years of combined local Real Estate experience and knowledge – wouldn’t you like The Caton Team to represent you? Let us know how we can be of service. Contact us any time.

Cell | Sabrina 650.799.4333 | Susan 650.796.0654 | EMAIL | WEB| BLOG

The Caton Team – Susan & Sabrina A Family of Realtors Effective. Efficient. Responsive. What can we do for you?

Berkshire Hathaway HomeServices – Drysdale Properties, Redwood City Ca.

DRE # | Sabrina 01413526 | Susan 01238225 | Team 70000218 | Office 01499008

The Caton Team does not receive compensation for any posts. Information is deemed reliable but not guaranteed. Third-party information not verified. We are licensed to assist our clients with their Real Estate needs. We do not provide legal or financial advice, directly or implied. Please seek the appropriate counsel.

Cybercriminals using the so-called “spray and pray” tactic love to impersonate well-known brands. Especially ones with huge customer bases.

Amazon reportedly has around 310 million active customers, so they certainly qualify as a brand worth impersonating. And it shows in the sheer volume of scams that use its name.

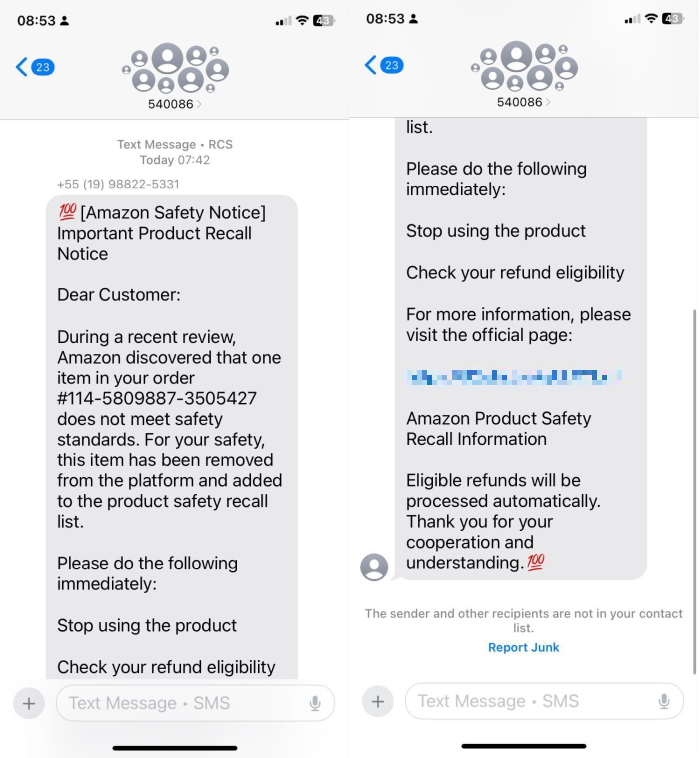

Amazon account take-over (ATO) scams were numerous during the holiday season, and they haven’t gone away. The scammers have ported the “product recall due to safety concerns” text message scam over to email.

The fake product recall message is one of scammers’ most popular lures, and we’ve reported on in the past.

“Dear Customer, we are writing to inform you of a product recall affecting an item from your March 2026 order due to a design defect that may pose a potential safety risk. We apologise for any inconvenience this may cause and appreciate your prompt attention to this important safety matter. Thank you for your continued trust in Amazon.”

Following the link takes the target to a fake login page designed to steal their Amazon username and password.

These messages are intentionally vague about the nature of the product or the exact issue they’re being recalled for. The less specific they are, the more likely it is that someone will think, “This could be me.” If you’ve recently ordered something from Amazon, you’re more likely to fall for it.

How to avoid falling for Amazon phishing scams

If you get a recall notice, don’t click any links. Instead, go straight to Amazon using the app or by typing the website into your browser. Then check the Message Centre in your account. Legitimate messages from Amazon will appear there.

If you’ve fallen for this, change your Amazon password straight away and anywhere else you use that password. Monitor your bank statements for any unfamiliar charges, and contact your bank immediately if you see anything suspicious.

Report the scam to Amazon itself, whether you’ve fallen for it or not.

In the US, forward scam texts to 7726 (SPAM) or use the “Report Junk” option. For emails, report them as spam in your inbox.

Install web protection that can warn you of phishing sites, card skimmers, and other nasties that could lead to your data being taken.

Scammers sometimes use information they’ve found online to personalize their scam messages. Check what information is already out there about you using our free Digital Footprint scanner and then remove or change as much of it as you can.

Pro tip:Malwarebytes Scam Guard can help you spot scams and guide you through what to do next.

We love what we do and would love to help you navigate your sale or purchase of Residential Real Estate. Please reach out for a personal consultation. Please enjoy our free resources below and get to know our team from our TESTIMONIALS.

Effective. Efficient. Responsive. The Caton Team 🏡

Got Real Estate Questions? The Caton Team is here to help.

We strive to be more than just Realtors – we are also your home resource. If you have any real estate questions, concerns, need a referral, or some guidance – we are here for you. Contact us at your convenience – we are but a call, text, or click away!

The Caton Team believes, in order to be successful in the San Francisco | Peninsula | Bay Area | Silicon Valley Real Estate Market, we have to think and act differently. We do this by positioning our clients in the strongest light, representing them with the utmost integrity, while strategically maneuvering through negotiations and contracts. Together we make dreams come true.

A mother and daughter-in-law team with over 35 years of combined local Real Estate experience and knowledge – wouldn’t you like The Caton Team to represent you? Let us know how we can be of service. Contact us any time.

Cell | Sabrina 650.799.4333 | Susan 650.796.0654 | EMAIL | WEB| BLOG

The Caton Team – Susan & Sabrina A Family of Realtors Effective. Efficient. Responsive. What can we do for you?

Berkshire Hathaway HomeServices – Drysdale Properties, Redwood City Ca.

DRE # | Sabrina 01413526 | Susan 01238225 | Team 70000218 | Office 01499008

The Caton Team does not receive compensation for any posts. Information is deemed reliable but not guaranteed. Third-party information not verified. We are licensed to assist our clients with their Real Estate needs. We do not provide legal or financial advice, directly or implied. Please seek the appropriate counsel.

Today, more than 24 million U.S. households have a net worth above $1 million, according to a Bloomberg analysis of Federal Reserve data, and one-third of those millionaire households have been minted since 2017.

That tracks closely with housing: From 2017 to 2023, the national median home price rose 35%, and by 2025, a simple starter home cost $1 million or more in more than half of all states, according to data from Realtor.com®.

“Millionaire status is closely tied to homeownership and resultant home equity,” explains Joel Berner, senior economist at Realtor.com. “Building home equity is the mechanism by which those accumulating wealth can put away some of their income each month and see that money grow with the value of their home.”

But as the typical age for a first-time homebuyer stretches to 40, it poses a complication: More Americans may be reaching millionaire status through housing, even as fewer have the runway to build that kind of wealth themselves.

Once households get into ownership, the wealth effect compounds. The report found that median home equity rises from about $180,000 within the first five years after purchase to more than $340,000 by years six through 10, then continues climbing with longer tenure.

That helps explain why so many households can cross the seven-figure net-worth threshold without looking or feeling especially affluent—they just keep living in the same house, and over time, their equity stake in that house can swell.

It also helps explain why the old idea of the “millionaire next door” may be even more relevant today than when it was first popularized in 1996 by the bestselling book of the same name.

The book challenged the image of a millionaire as someone who struck it rich in stocks or business, instead portraying millionaires as ordinary-looking households (like your neighbors) whose wealth was real but understated—people who spent carefully and built net worth steadily over time.

It’s what Realtor.com Chief Economist Danielle Hale calls the “get rich slow scheme” of homeownership, and Berner says that’s exactly the dynamic playing out for many millionaires today.

“These figures suggest that those who become millionaires do so with high-growth investments rather than simply piling up cash, and that most of them own homes rather than rent,” he says. “These are long-term approaches to wealth building, so these newly minted millionaires may not have major positive cash flows during their years of working, saving, and building up home equity.”

But Berner adds there are other sneaky ways that homeownership can build wealth.

“We showed that homeownership correlates with higher rates of saving, even on top of home equity building,” he says, pointing to recent research from Realtor.com on generational wealth and homeownership. “This level of financial acumen and discipline leads some to become millionaires and others to be left behind.”

Over time, that combination can produce a very large balance-sheet effect. Homeowners’ median net worth has typically been 30 to 50 times that of renters since 1989, according to a Realtor.com analysis of Federal Reserve Survey of Consumer Finances data.

It’s a clear illustration of why homeownership remains one of the clearest paths to millionaire status. It also offers an important reframing of homeownership today: While high prices have recast homeownership as the end goal of wealth creation, the data instead points to it as where real wealth creation begins.

The same market creating millionaires is locking others out

That poses a material problem for younger and first-time buyers today. The same housing market that has helped many owners build seven-figure net worth is also making it harder for others to get on the ladder in the first place.

The median age of first-time homebuyers has climbed from 30 in 1990 to 40 in 2025, while the time needed to save for a down payment has stretched from three years to nearly 10, according to recent research from Realtor.com on generational wealth.

Buyers who purchase early accumulate a higher net worth in middle age, the Realtor.com Generational Wealth study has found.Realtor.com

That delay matters because time is such an important variable in compounding home equity into wealth. Buying by age 32 is associated with roughly 22.5% higher net worth by age 50, or about $119,000 more, compared with buying in one’s 40s, according to the analysis from Realtor.com.

Federal Reserve data also shows how this matters for millionaire status. Average household net worth doesn’t climb above $1 million until ages 55 to 64, meaning households that buy later have less time to let home equity compound before reaching the years when wealth typically peaks.

As Berner put it, “Homeownership is certainly a path to the upper middle class, and the fact that it is so hard to achieve for first-time buyers right now is creating serious inequity.”

Millionaire status under pressure

As the American millionaire class has grown, the material meaning of that status has changed. In 1995, for perspective, there were only 1.6 million millionaires in the U.S., according to a report from the IRS.

Today, that threshold is far less exclusive and far more tied up in illiquid assets like home equity—meaning that it hasn’t necessarily translated into obvious abundance or day-to-day financial freedom.

So as more households have moved further up the balance-sheet ladder, they haven’t necessarily transcended into old (often liquid) ideas of affluence.

That’s why millionaire status is under more pressure today. The assets are real, but for many households they’re embedded in the home they live in or the retirement account they are not yet ready to draw from. What has grown is not only the number of millionaires, but the gap between looking wealthy on paper and feeling wealthy in practice.

We love what we do and would love to help you navigate your sale or purchase of Residential Real Estate. Please reach out for a personal consultation. Please enjoy our free resources below and get to know our team from our TESTIMONIALS.

Effective. Efficient. Responsive. The Caton Team 🏡

Got Real Estate Questions? The Caton Team is here to help.

We strive to be more than just Realtors – we are also your home resource. If you have any real estate questions, concerns, need a referral, or some guidance – we are here for you. Contact us at your convenience – we are but a call, text, or click away!

The Caton Team believes, in order to be successful in the San Francisco | Peninsula | Bay Area | Silicon Valley Real Estate Market, we have to think and act differently. We do this by positioning our clients in the strongest light, representing them with the utmost integrity, while strategically maneuvering through negotiations and contracts. Together we make dreams come true.

A mother and daughter-in-law team with over 35 years of combined local Real Estate experience and knowledge – wouldn’t you like The Caton Team to represent you? Let us know how we can be of service. Contact us any time.

Cell | Sabrina 650.799.4333 | Susan 650.796.0654 | EMAIL | WEB| BLOG

The Caton Team – Susan & Sabrina A Family of Realtors Effective. Efficient. Responsive. What can we do for you?

Berkshire Hathaway HomeServices – Drysdale Properties, Redwood City Ca.

DRE # | Sabrina 01413526 | Susan 01238225 | Team 70000218 | Office 01499008

The Caton Team does not receive compensation for any posts. Information is deemed reliable but not guaranteed. Third-party information not verified. We are licensed to assist our clients with their Real Estate needs. We do not provide legal or financial advice, directly or implied. Please seek the appropriate counsel.

Today, as many as 15.2 million adults ages 55 and older are childless, according to the latest estimate available from the U.S. Census Bureau. Of these adults, about 40% live alone—double the rate of similarly aged adults with children.

“We’re kind of in a troubling situation,” Ronald Lee, a UC Berkeley demographer and economist, tells Realtor.com®. “We’re stuck with these values and institutions that haven’t really adjusted to the fact that we live much longer and we’re having many fewer kids.”

That’s creating a historic paradox: On the one hand, $19 trillion in baby boomer home equity is preparing to move. On the other, the vertical flow of family legacy is being rerouted laterally to nieces, nephews, charities, and the high cost of the American health care system.

That introduces a slew of questions for the population, and uniquely, the housing market.

As steep competition has put more pressure on the role of family help for younger house hunters to become homeowners, children raised in homeowner households are 18.4 percentage points more likely to become homeowners by age 35, according to a Realtor.com analysis of data from the Panel Study of Income Dynamics.

So as the Great Wealth Transfer collides with the baby bust, the $124 trillion question is what happens to the American dream when the ladder of inheritance runs out of rungs?

The rise of ‘solo agers’ and ‘orphan-elders’

“There’s so many of us that are growing older without family support and structure,” Carol Marak, a financial educator who is aging on her own at 74 years old, tells Realtor.com. “I initially started out just wanting to build awareness about this, but it’s going to take more than building awareness. We need to put systems in place.”

In her work, she leads peer groups and workshops with other solo-agers to help them plan for the later stages of life. That includes financial, health care, and estate planning as well as social networking.

“We all have our own preferences for how we want to age, how we want to live, how we want to address these issues. I give [solo-agers] the tools for how to start thinking through these issues,” she says.

When asked where most of the solo-agers she works with plan on leaving their wealth, Marak says that many “don’t really care where it goes.”

“Most of us will leave it to a charity,” she adds, also citing nieces and nephews, as well as caretakers of beloved pets.

Some heirs may get more—but fewer people may benefit

As wealth moves laterally, it upends what Jay Zigmont, a certified financial planner who specializes in working with child-free clients, calls the “traditional life script.”

This script assumes a vertical flow: You build wealth and pass it on to direct heirs.

Baby boomers alone are estimated to transfer roughly $84 trillion in wealth through 2048, with millennials standing to inherit the lion’s share, according to projections from Cerulli Associates.

But as families shrink, that flow is narrowing and colliding with a long and established trend of wealth inequality.

“Since there are fewer children, that means for each old person, those inherited assets are going to be concentrated on a smaller number of people,” Lee explains.

So instead of spreading, wealth is at risk of pooling—more than it already is. Cerulli’s estimates suggest that 2% of households will control over 50% of the Great Wealth Transfer’s transfers. Add in fewer people (or just one person) to divide the assets among and the individual lift can be massive.

Zigmont describes one 29-year-old client whose inheritance from her grandmother was so significant “she doesn’t have to work again in her life.”

That concentration risks super-charging long entrenched wealth divides. Today, the homeownership rate for white households is 75.1%, compared with 44.2% for Black households and 48.7% for Hispanic households.

Even for the lucky heirs, the timing is at risk of being a mismatch. As people live longer, they’re bequeathing wealth to their inheritors later.

“The age of inheriting is going to be in the 50s, something like that,” Lee says—long after the critical window where buying a home can maximize a person’s lifetime net worth. “It comes too late to really help you with your life.”

Even for the lucky heirs, the timing is at risk of being a mismatch. As people live longer, they’re bequeathing wealth to their inheritors later.

“The age of inheriting is going to be in the 50s, something like that,” Lee says—long after the critical window where buying a home can maximize a person’s lifetime net worth. “It comes too late to really help you with your life.”

Long-term care may be the biggest heir of all

Even when there is significant wealth to pass on, there is no guarantee that it will survive the high cost of aging.

As of 2026, the nationwide average annual cost for a shared room in a nursing home has climbed to roughly $120,000, while private rooms now exceed $136,000, according to the American Council on Aging.

It’s a sum few can afford out of pocket; and for those with children, the gap is often closed by familial care—an informal support system that costs adult children an estimated $144,000 to $201,000 over a two year period, according to one study.

But for those aging solo, that unpaid labor isn’t baked in. To make matters harder, there isn’t the same social safety net that there once was.

The problem, Lee explains, comes back to the changing population: Older generations are living longer with higher care needs and fewer younger workers to fund the programs that provide a backstop.

Lee’s research shows that public transfers like these (i.e., Social Security and Medicaid) historically play a larger role in high-income countries like the U.S. than any massive transfer of private wealth.

“The transfers older people get … are often the only thing standing between an elderly person and poverty,” he says.

This structural void is exactly what Marak recognized in her 50s.

While she owned her home outright, she realized she had little liquidity to fund the professional support she would eventually need as a solo-ager. To bridge that gap, she spent five years saving aggressively before selling her suburban house and downsizing to a high-rise in downtown Dallas, where she’s closer to public transit, her doctors, and community.

Her goal—a lesson she now imparts to her senior groups—is to maximize quality of life while ensuring her money outlasts her. In this new landscape, leaving wealth behind isn’t about ensuring a windfall for an heir; it is a final level of financial security that guarantees these seniors will be taken care of.

We love what we do and would love to help you navigate your sale or purchase of Residential Real Estate. Please reach out for a personal consultation. Please enjoy our free resources below and get to know our team from our TESTIMONIALS.

Effective. Efficient. Responsive. The Caton Team 🏡

Got Real Estate Questions? The Caton Team is here to help.

We strive to be more than just Realtors – we are also your home resource. If you have any real estate questions, concerns, need a referral, or some guidance – we are here for you. Contact us at your convenience – we are but a call, text, or click away!

The Caton Team believes, in order to be successful in the San Francisco | Peninsula | Bay Area | Silicon Valley Real Estate Market, we have to think and act differently. We do this by positioning our clients in the strongest light, representing them with the utmost integrity, while strategically maneuvering through negotiations and contracts. Together we make dreams come true.

A mother and daughter-in-law team with over 35 years of combined local Real Estate experience and knowledge – wouldn’t you like The Caton Team to represent you? Let us know how we can be of service. Contact us any time.

Cell | Sabrina 650.799.4333 | Susan 650.796.0654 | EMAIL | WEB| BLOG

The Caton Team – Susan & Sabrina A Family of Realtors Effective. Efficient. Responsive. What can we do for you?

Berkshire Hathaway HomeServices – Drysdale Properties, Redwood City Ca.

DRE # | Sabrina 01413526 | Susan 01238225 | Team 70000218 | Office 01499008

The Caton Team does not receive compensation for any posts. Information is deemed reliable but not guaranteed. Third-party information not verified. We are licensed to assist our clients with their Real Estate needs. We do not provide legal or financial advice, directly or implied. Please seek the appropriate counsel.

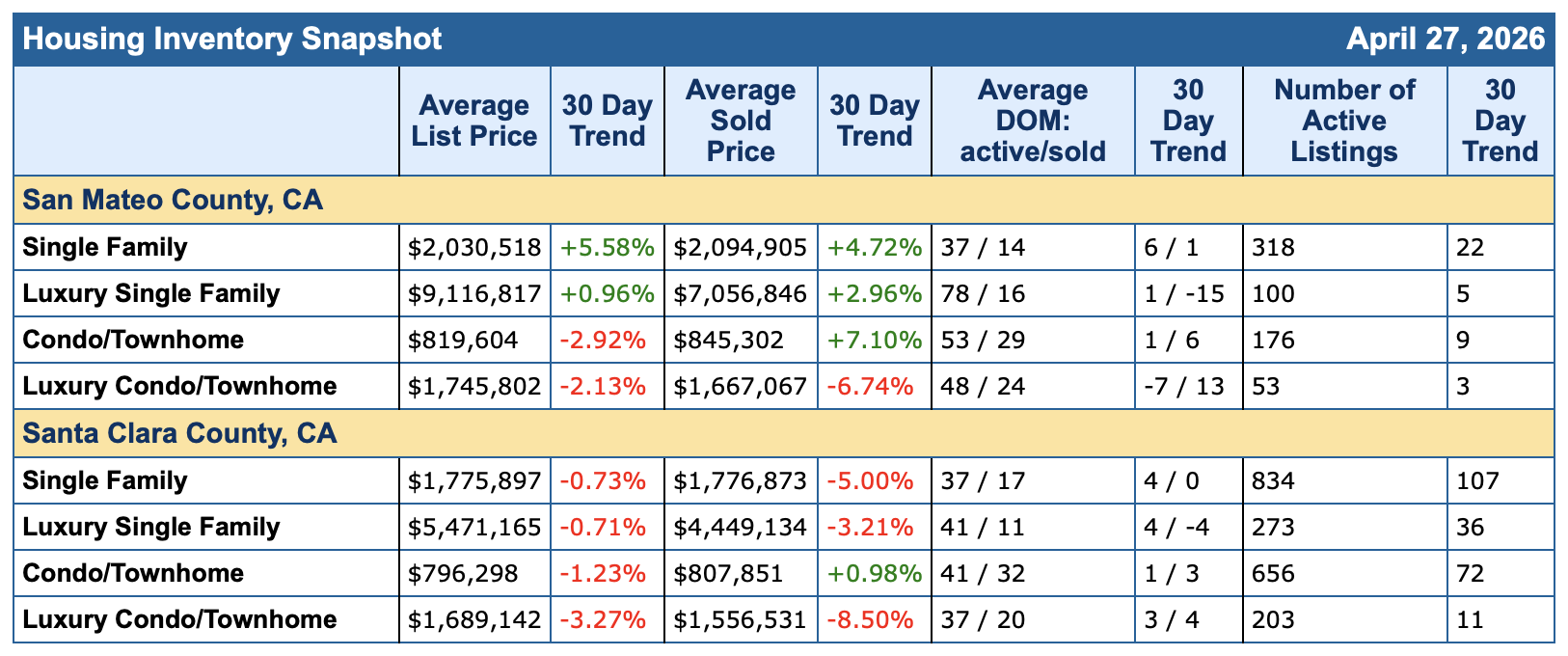

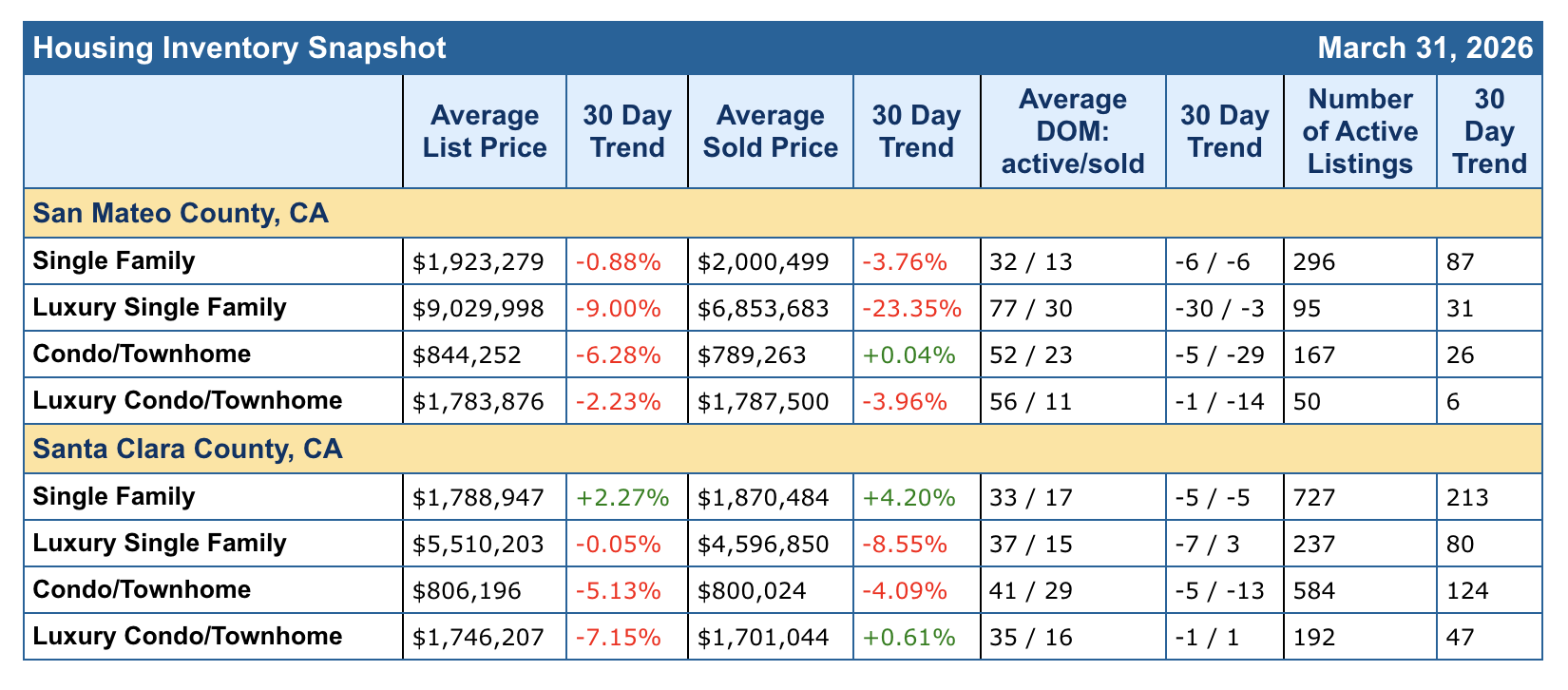

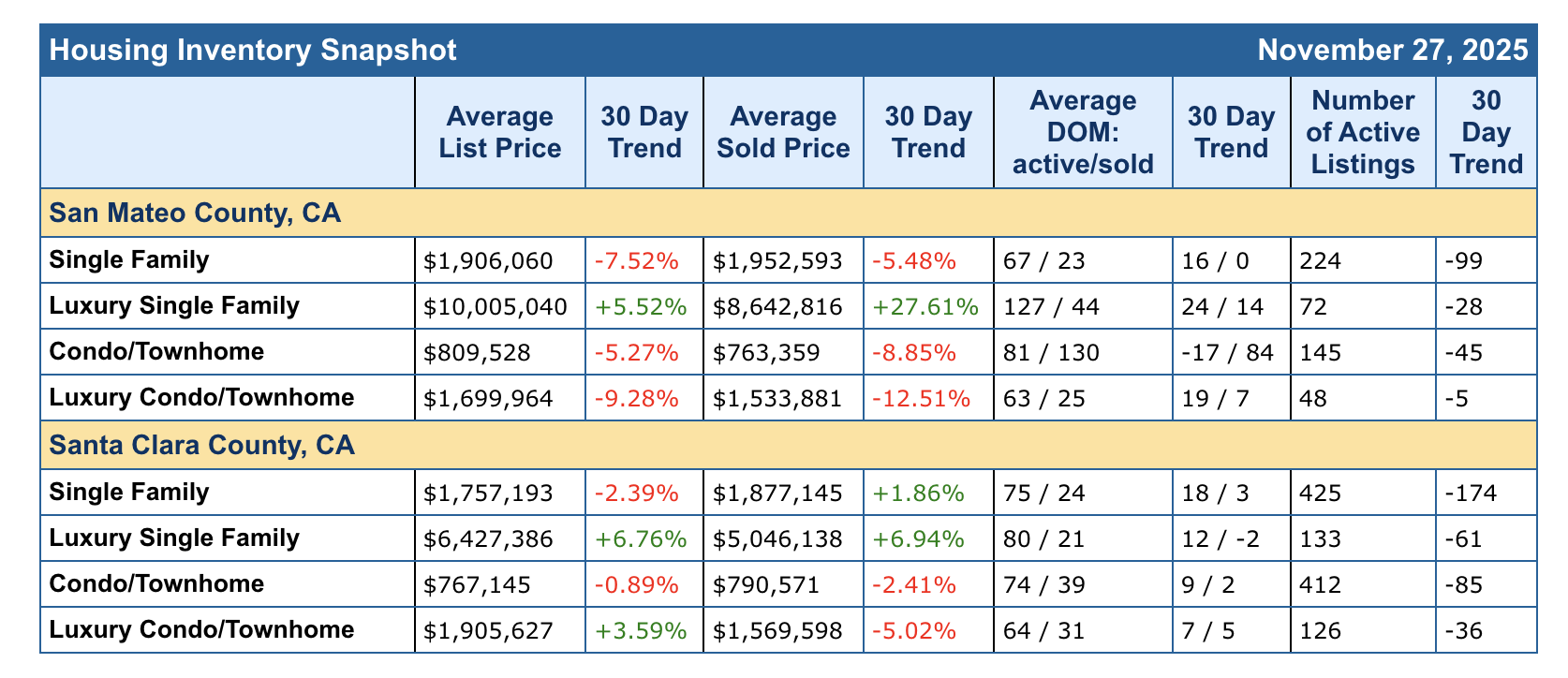

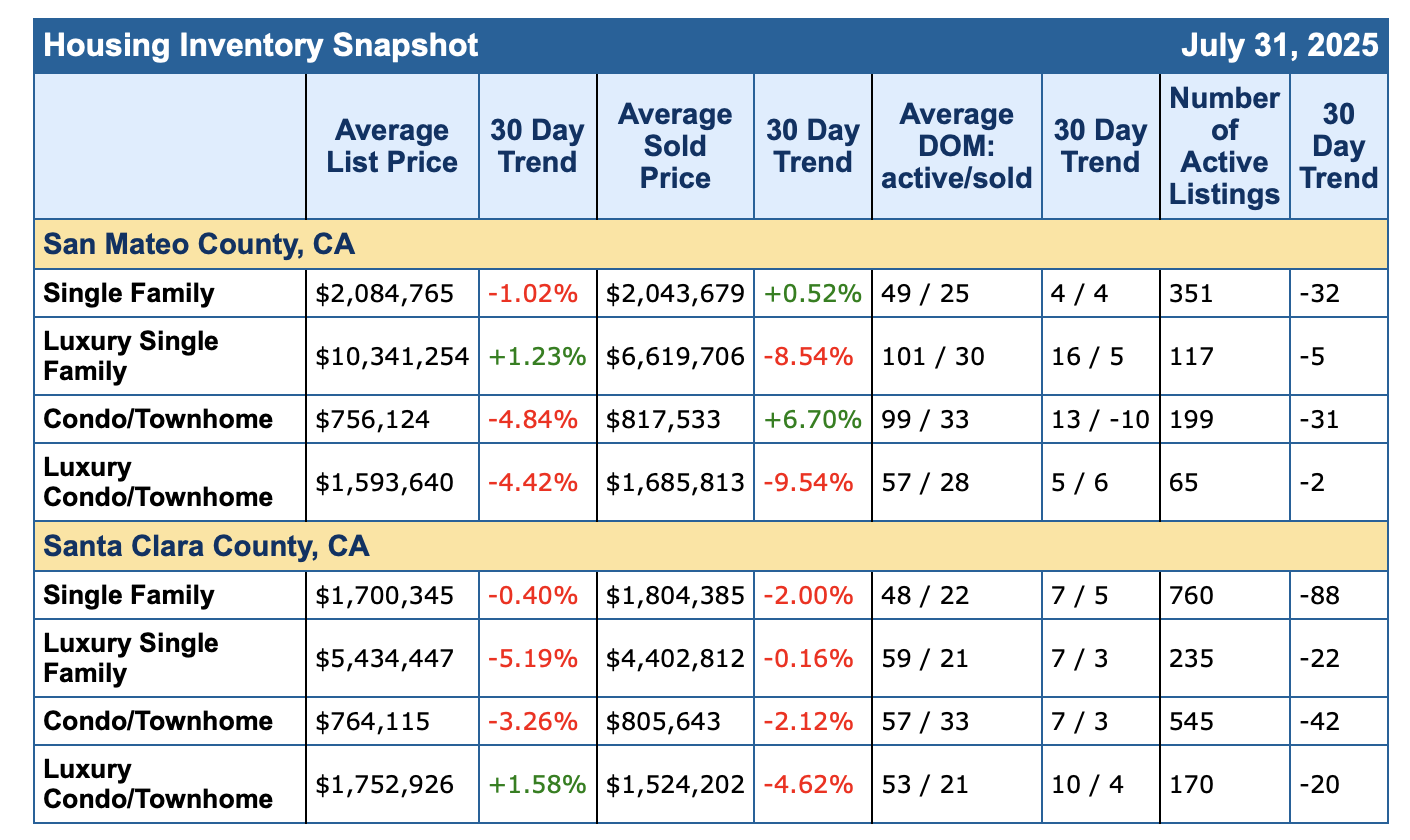

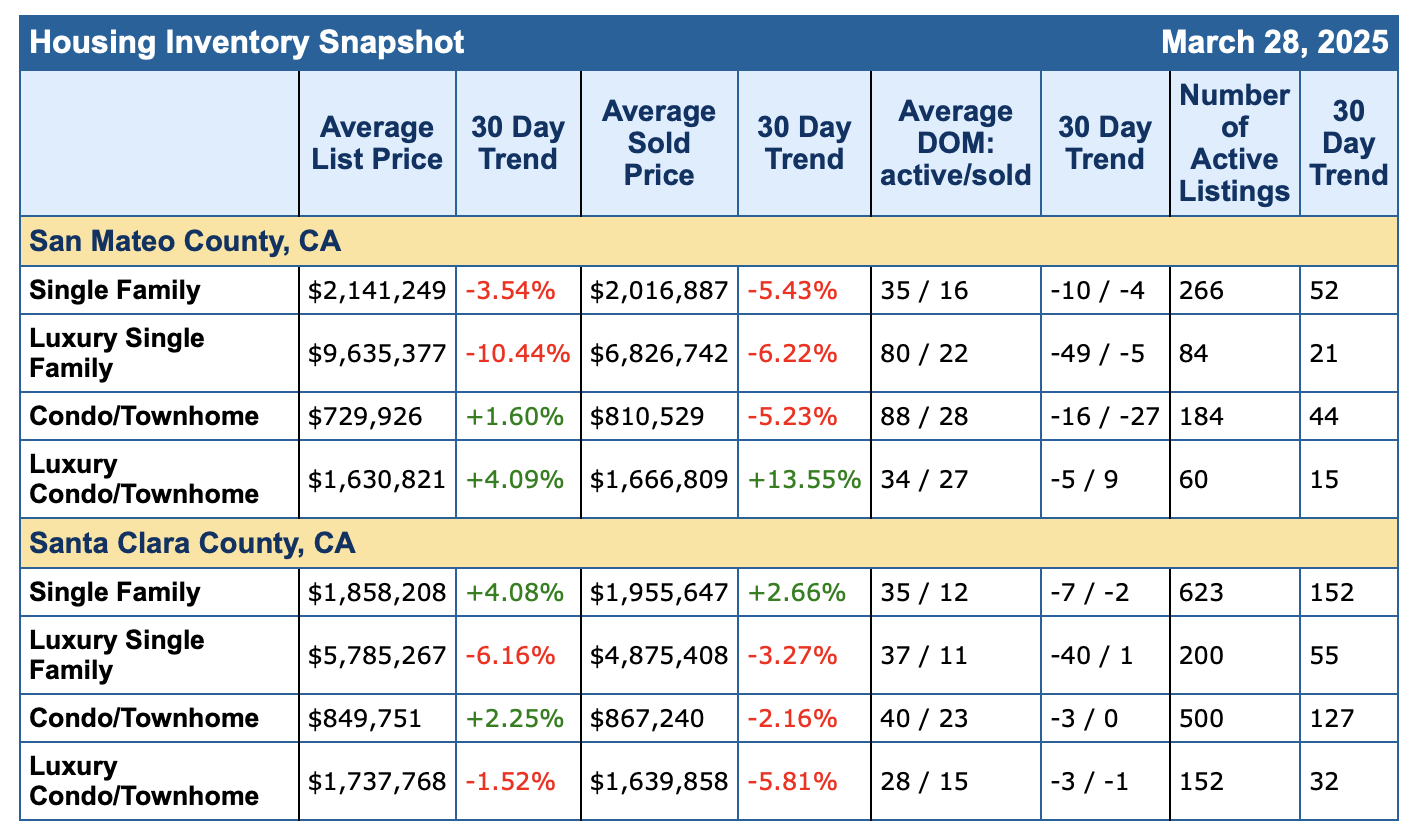

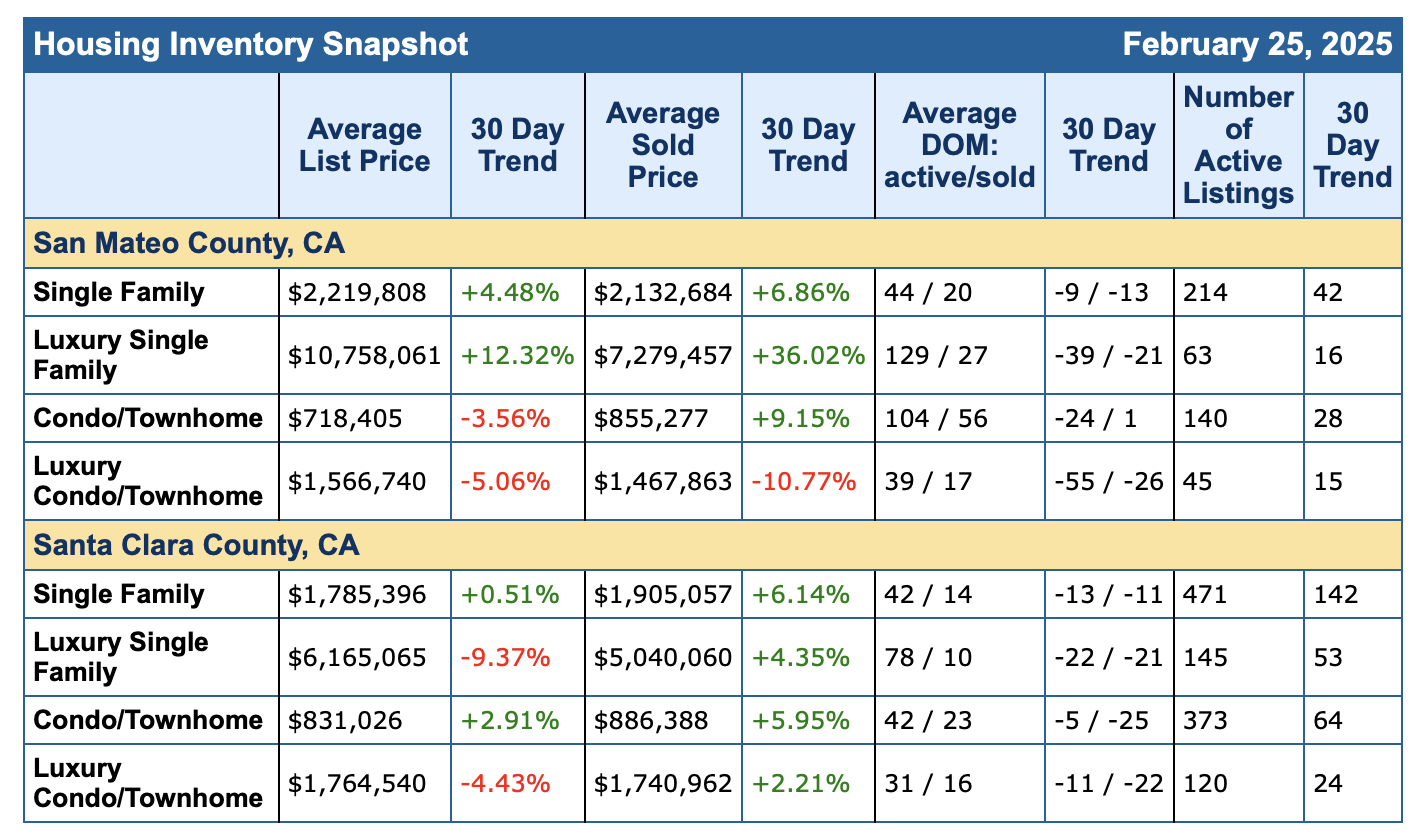

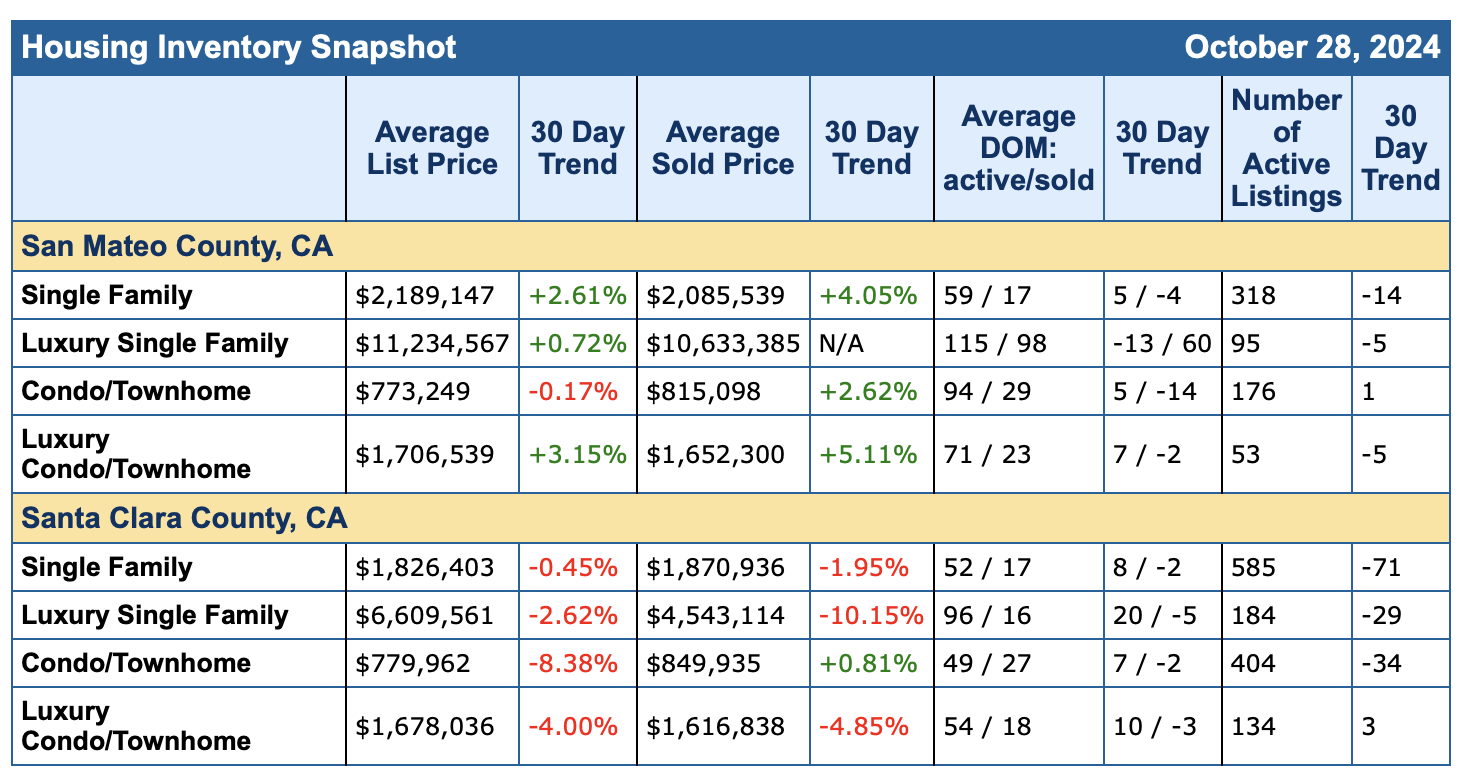

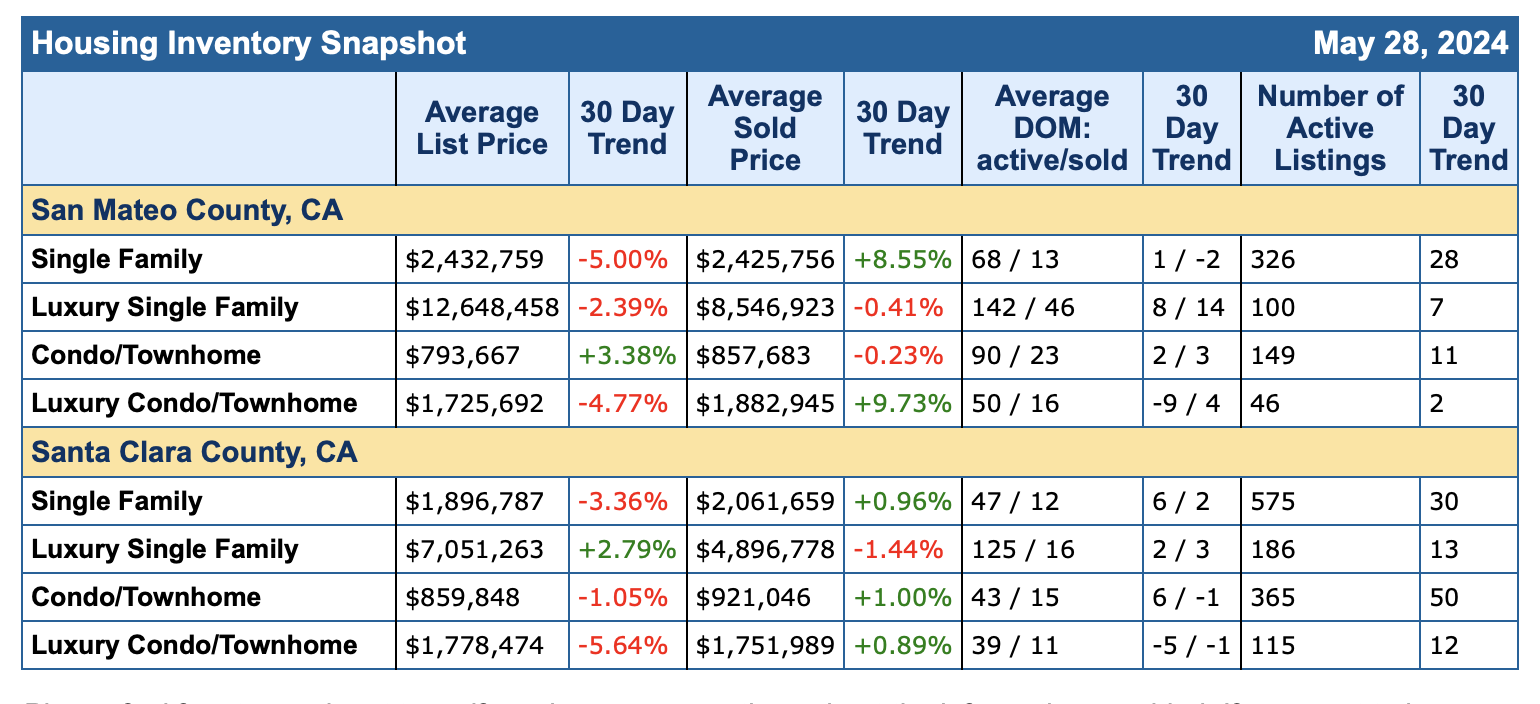

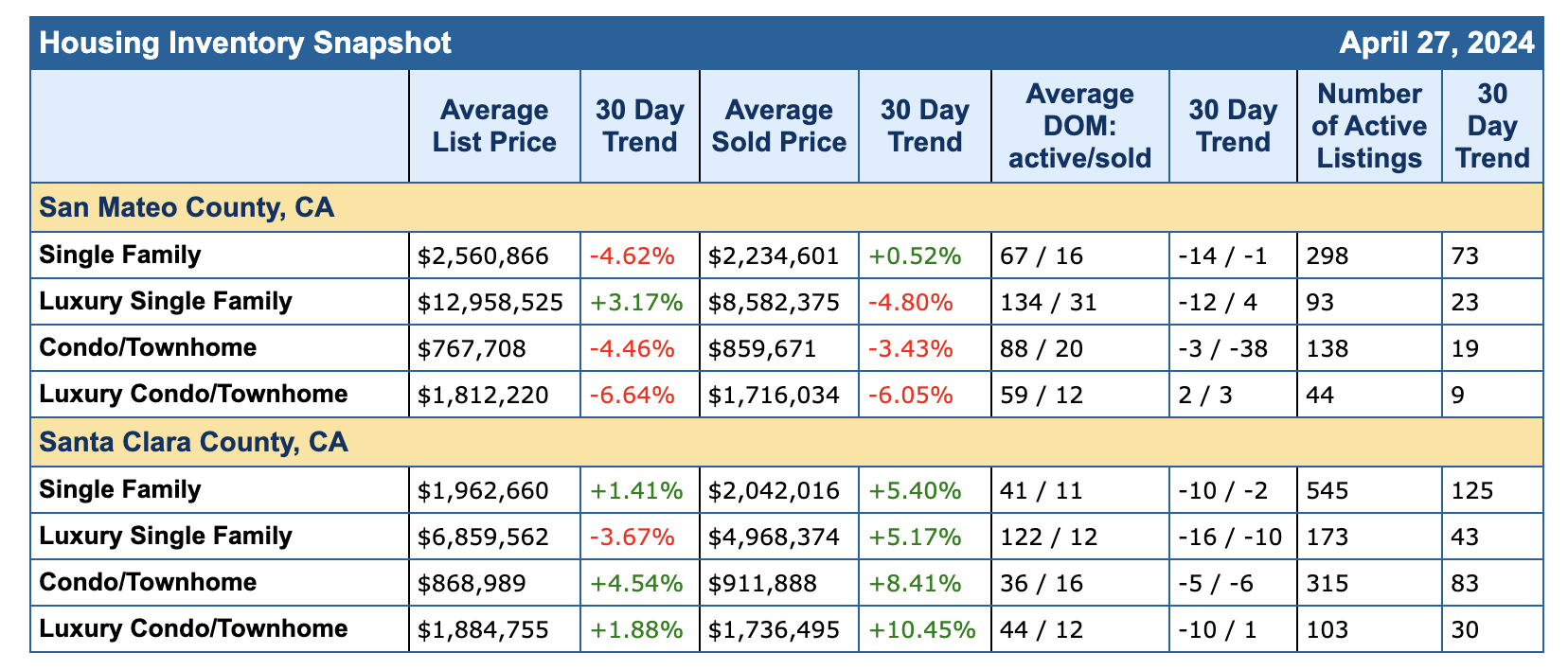

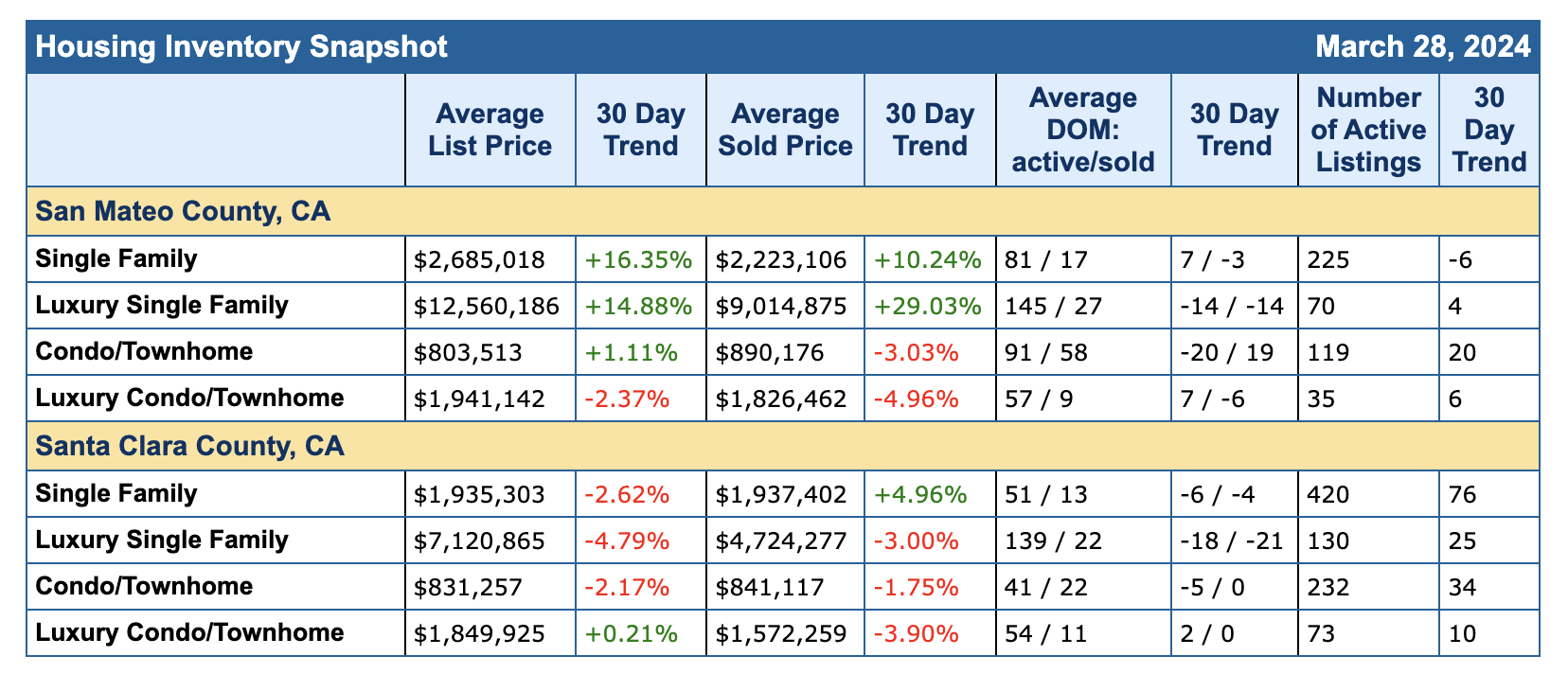

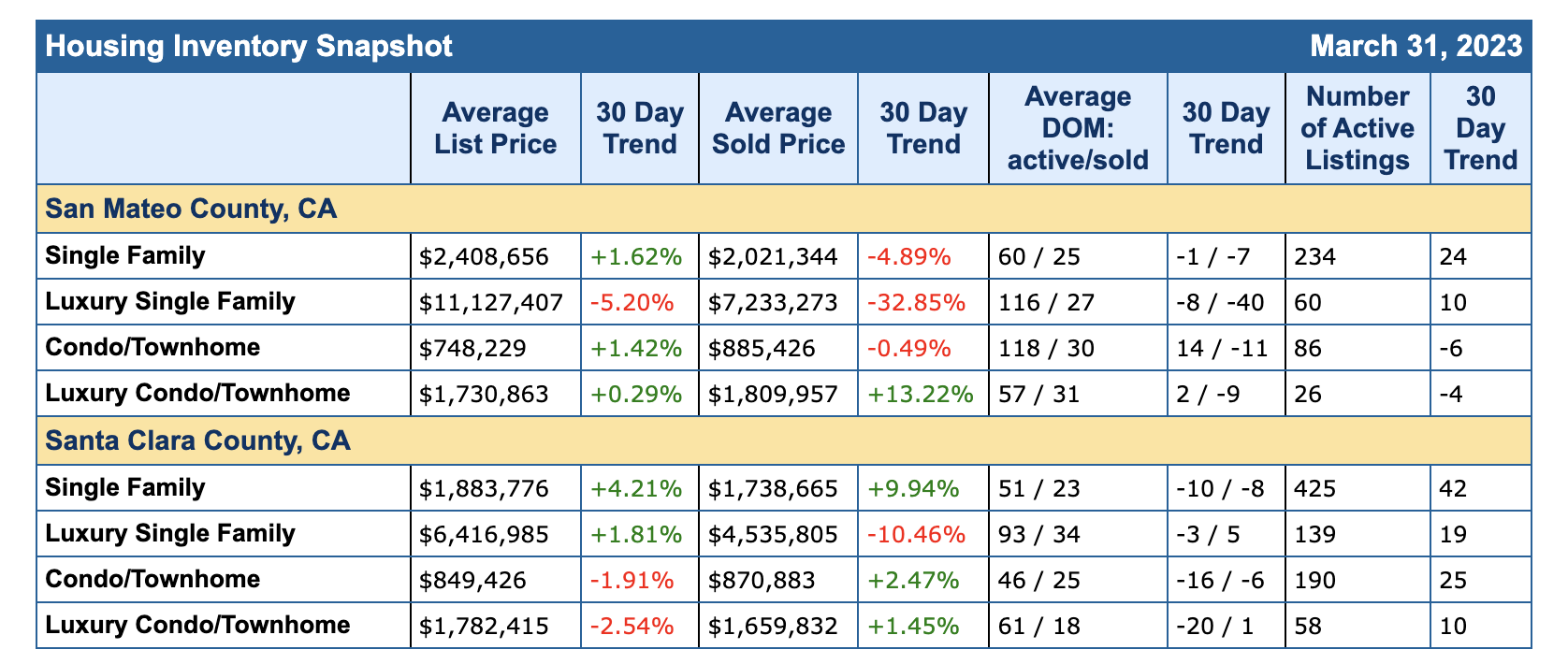

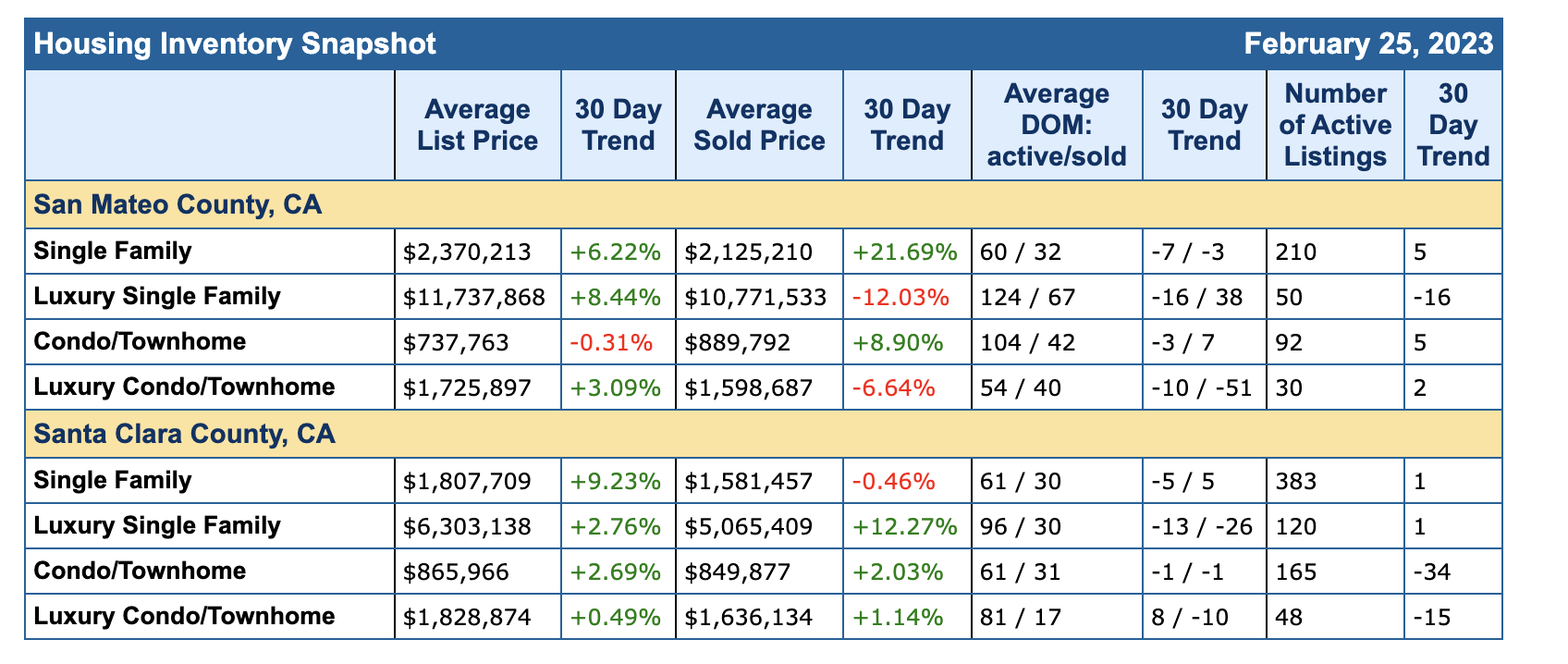

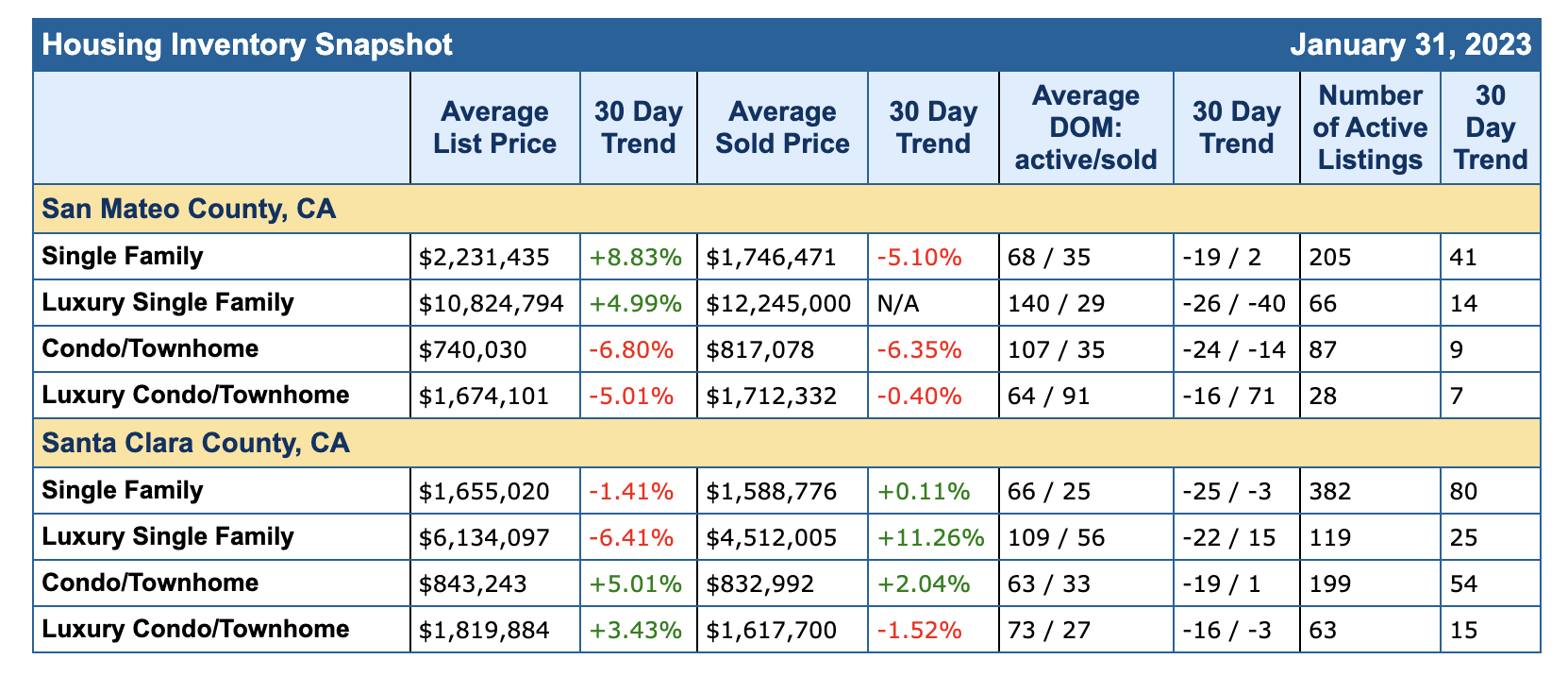

What gain we saw in Feb has tempered in March. We are midway through April and I can feel the cold thawing. Buyers are doing their homework, loan shopping and budget making. While sellers are getting their homes ready for the Spring Market that officially starts on May 1. Are you ready?

There was slight price adjustments in March, which still feels seasonal. Buyer right now are weighing so much, the interest rates haven’t fallen much, hovering around 6%+, the state of the economy and the world has folks on edge. But not off the table. With caution and a solid plan, I am seeing my clients make their Real Estate goals work! How can The Caton Team help you?

What are your thoughts for the year ahead?

For my selling clients, life changes everyday and if you need to sell your home – let’s come up with a strategy to get you sold! Even in an odd market The Caton Team can help you strategically sell your home.

For my buyers, some homes are garnering multiple offers, but some are overlooked. With a little legwork, a buyer can truly find some great opportunities when they align with the market.

If you’re considering a Real Estate move, contact The Caton Team for a free consultation. With over 45+ years of combined Real Estate experience, we have the knowledge and know-how to guide you to your goal. Call us at 650.799.4333 or email us at info@TheCatonTeam.com.

Whether you are selling or buying – today or tomorrow – contact The Caton Team – we’re happy to help you achieve your Real Estate goals.

Effective. Efficient. Responsive. The Caton Team 🏡

Each market is unique and with over 40 years of combined Real Estate experience, The Caton Team is more than happy to be of service if and when you are considering a move. Contact us anytime during your journey, together we’ll help you achieve your Real Estate goals.

Got Questions? The Caton Team is here to help.

Call| Text | Sabrina 650.799.4333 |EMAIL | WEB| BLOG

We love what we do and would love to help you navigate your sale or purchase of Residential Real Estate. Please reach out for a personal consultation. Please enjoy our free resources below and get to know our team TESTIMONIALS.

Got Real Estate Questions? The Caton Team is here to help.

We strive to be more than just Realtors – we are also your home resource. If you have any real estate questions, concerns, need a referral, or need some guidance – we are here for you. Contact us at your convenience – we are but a call, text or click away!

The Caton Team believes, in order to be successful in the San Fransisco | Peninsula | Bay Area | Silicon Valley Real Estate Market we have to think and act differently. We do this by positioning our clients in the strongest light, representing them with the utmost integrity, while strategically maneuvering through negotiations and contracts. Together we make dreams come true.

A mother and daughter-in-law team with over 35 years of combined, local Real Estate experience and knowledge – wouldn’t you like The Caton Team to represent you? Let us know how we can be of service. Contact us any time.

Call| Text | Sabrina 650.799.4333 | Susan 650.796.0654 |EMAIL | WEB| BLOG

The Caton Team – Susan & Sabrina A Family of Realtors Effective. Efficient. Responsive. What can we do for you?

You must be logged in to post a comment.