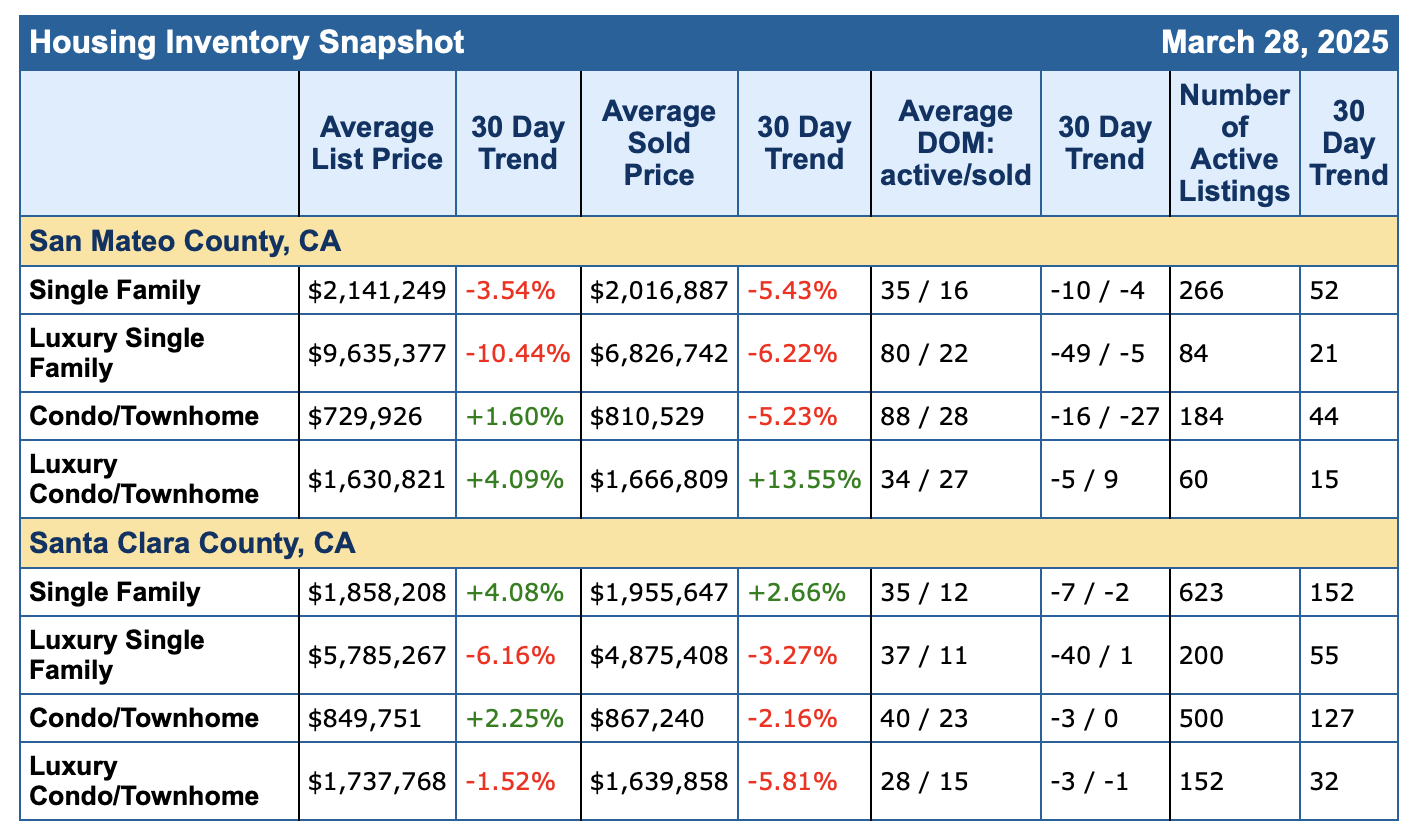

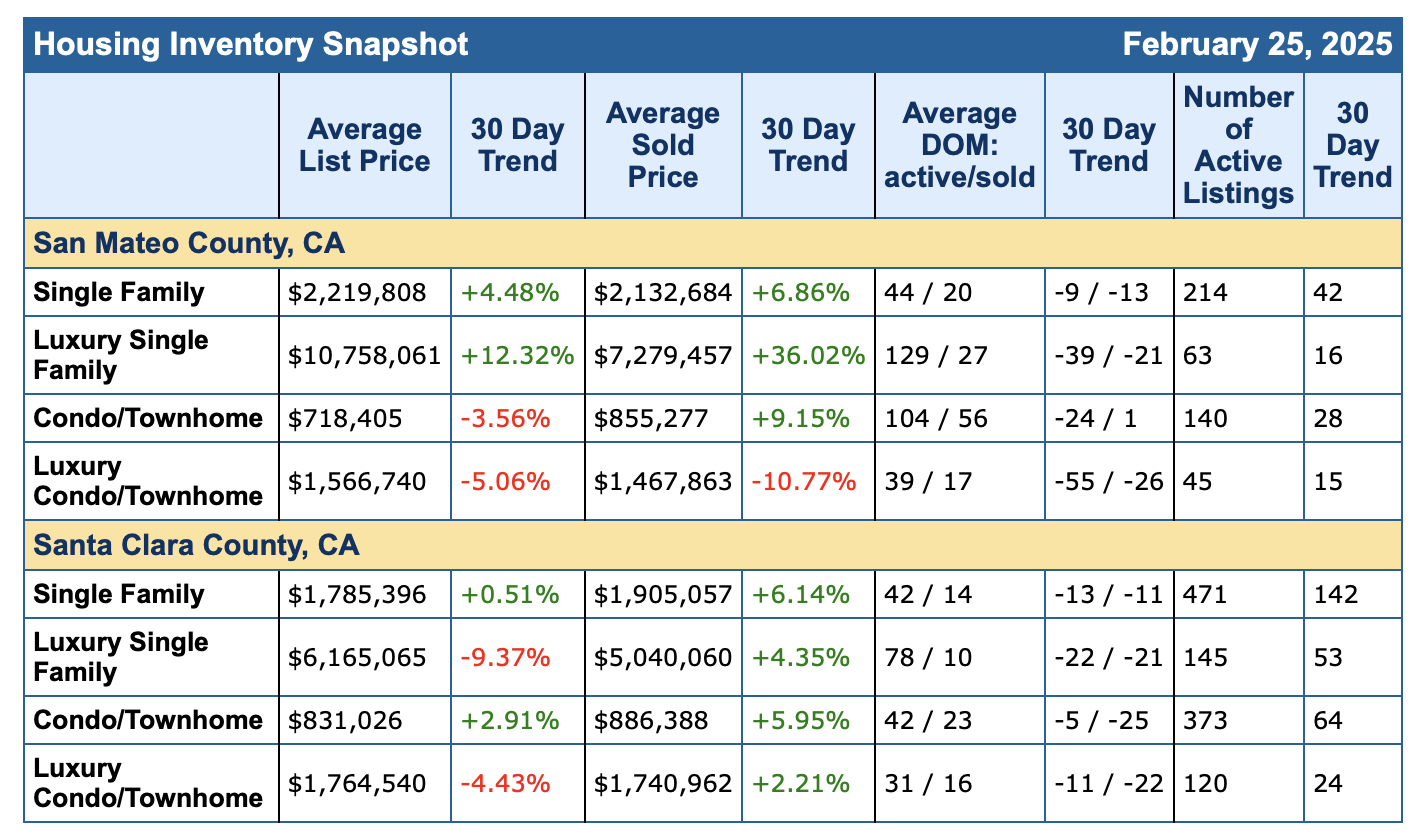

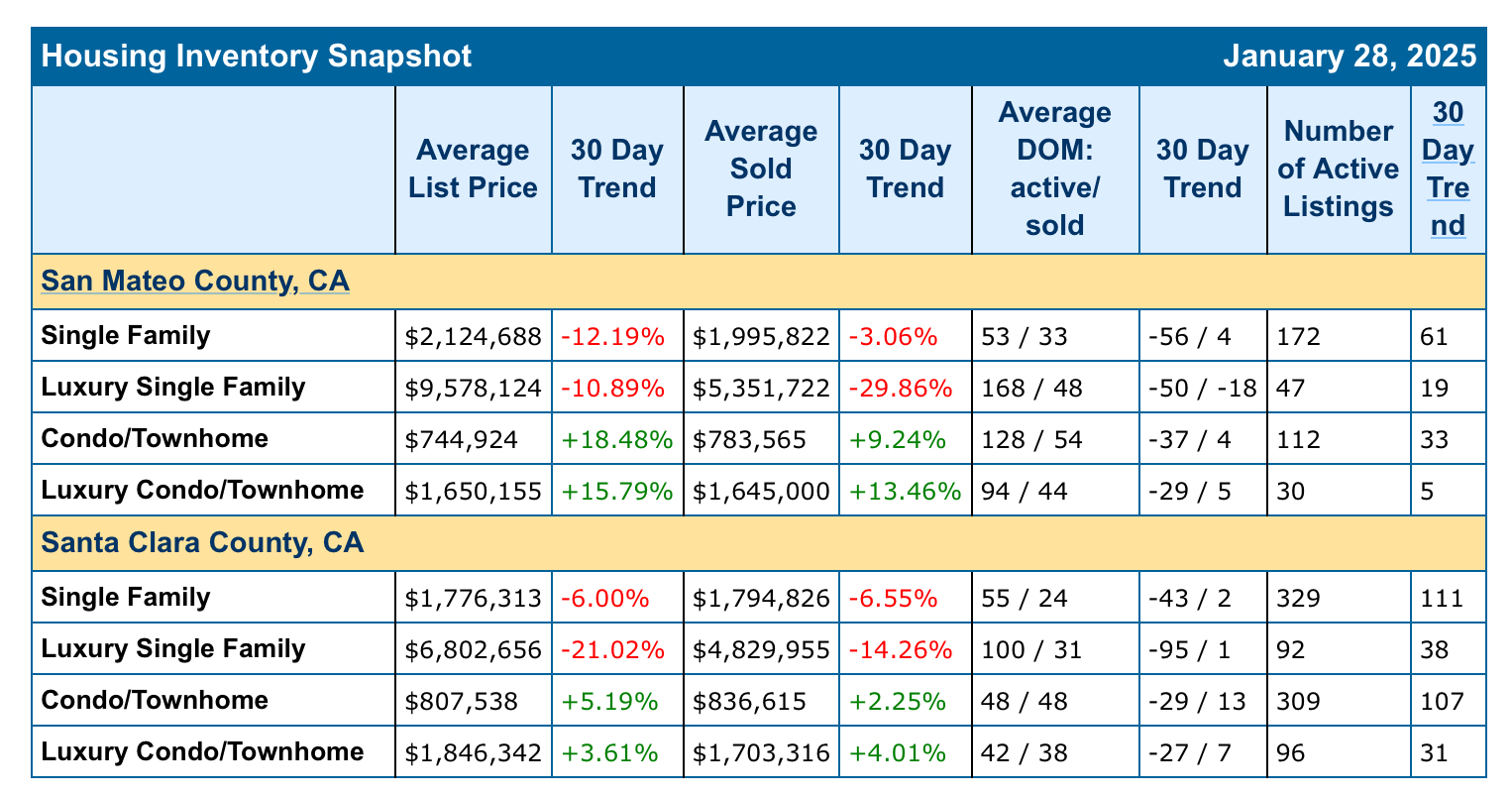

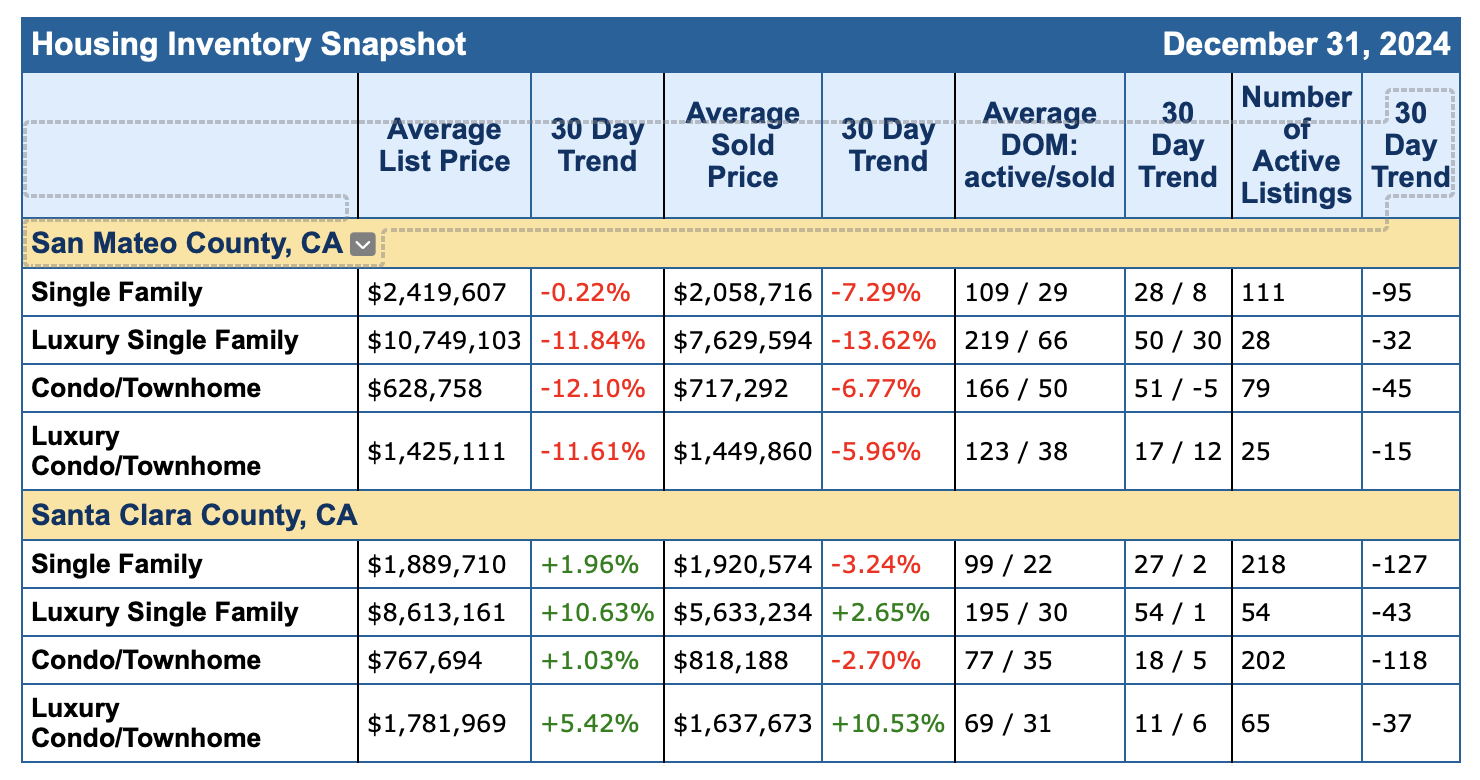

Key Points

Elevated, stylish designs beat traditional or overly personal features.

Buyers prioritize natural light, outdoor space, and charm.

Practical features like mudrooms and soundproofing are also important.

I read this article HERE. By Sarah Lyon

Not all home features are created equal: There are some that will majorly stand out to prospective buyers and others that may seem promising yet will ultimately fall by the wayside. Today’s buyers, real estate agents tell us, are especially focused on properties that offer plenty of natural light, outdoor gathering spaces, and lots of character and charm, among other features.

Read on to learn more about the six features—some of which are a bit unexpected—that three agents notice buyers focusing in on time and time again.

Meet the Expert

- Lauren Auresto is a real estate agent with Better Homes and Gardens Real Estate Gaetano Marra Homes.

- Cy Karrat is a real estate agent with Dallien Realty.

- Allison Freeman is a real estate agent with The Premier Property Group.

Natural Light

:max_bytes(150000):strip_icc():format(webp)/Screenshot2025-10-22at4.30.33PM-4e7a7f7cf2f545feb3c3a66e47a6317c.png)

Natural light is priceless, quite literally, and it majorly stands out to home buyers, agents say. “It’s amazing how often buyers walk into a home and instinctively exhale when sunlight pours through large windows,” says Lauren Auresto, a real estate agent with Better Homes and Gardens Real Estate Gaetano Marra Homes. Cy Karrat, a real estate agent with Dallien Realty, agrees, and says that when his buyers are transitioning out of dark apartments, the presence of abundant natural light in particular becomes a top priority in their home search.

Want more design inspiration? Sign up for our free daily newsletter for the latest decor ideas, designer tips, and more!

Don’t Miss

Real Estate Agents Agree: This One Home Feature Always Sells a Home Faster

:max_bytes(150000):strip_icc():format(webp)/GettyImages-88878477-b26cbd4b23004302942447bd2f4ba170.jpg)

Designers Agree: These Are the Features That Instantly Make a Home Feel Warm and Welcoming

Outdoor Living Spaces

Sometimes, it’s not only about what’s inside a home—a property’s outdoor features play a significant role in wooing buyers, too. The pandemic really revived backyard living, Auresto says, and ample outdoor space is key for many. “Buyers light up at the sight of a thoughtfully designed outdoor space,” she says. To really make an outdoor area great, she adds, ensure it’s equipped with privacy, good lighting, and WiFi.

Shallow Pools

While pools are more popular in certain areas of the country over others, they can still definitely be a selling point. But these days not just any type of pool will do, says Allison Freeman, a real estate agent with The Premier Property Group. Prospective buyers are partial to shallow pools made for sports and lounging as opposed to more traditional deeper pools.

Character and Charm

:max_bytes(150000):strip_icc():format(webp)/Screenshot2025-10-22at4.31.17PM-0511e0a1392c4be3957e9ec78b1648ca.png)

You may think that buyers want every inch of a home to be perfect, but in reality, what people often really crave is a bit of character, Auresto says. “They’re tired of cookie-cutter new builds and love details that add soul,” she says, highlighting features like built-in bookshelves, window seats, and statement lighting as instant winners among prospective buyers.

Freeman feels similarly, adding that charm is also a major part of the equation. “We live on social media,” she says, so “whether it’s decor, natural light, or a charming exterior, ‘cute’ sells.”

Keep in mind that there’s a big difference between character and personalization, though. Auresto says that sellers need to remember to steer clear of too much of the latter to ensure that any buyer will be able to envision creating their own life in your home.

Noise Level

Peace and quiet is at the top of many people’s lists. When a buyer is touring a condo building or townhouse in particular, noise levels may be one of their top concerns, Karrat says. “Many want to know how well the building is insulated, and whether they’ll hear footsteps upstairs or noise from neighboring units,” he says.

Functional Mudrooms

:max_bytes(150000):strip_icc():format(webp)/Screenshot2025-10-22at4.32.43PM-a8b17595ca19449385dee6b488e8b541.png)

Today’s buyers are all about the practical, and when they see a well-designed mudroom, they’re likely to fall head over heels for it, says Auresto. “Once an afterthought, these functional spaces have become a quiet luxury,” she says. Bonus points for mudrooms equipped with hooks, drawers, charging stations, and even laundry bins, she says. “It’s not glamorous, but it’s the kind of feature that makes a house functional.”

Got Questions? The Caton Team is here to help.

Cell| Sabrina 650.799.4333 | Susan 650.796.0654 | EMAIL | WEB | BLOG

We love what we do and would love to help you navigate your sale or purchase of Residential Real Estate. Please reach out for a personal consultation. Please enjoy our free resources below and get to know our team from our TESTIMONIALS.

Effective. Efficient. Responsive. The Caton Team 🏡

How Can The Caton Team Help You?

TESTIMONIALS | HOW TO SELL | VIRTUAL STAGING | A GUIDE TO BUYING | BUYING INFO | MOVING | TRUST AGREEMENTS | HEALTH CARE DIRECTIVES | TESTIMONIALS

Get exclusive inside access when you follow us on Facebook & Instagram

TESTIMONIALS | HOW TO SELL | VIRTUAL STAGING | A GUIDE TO BUYING | BUYING INFO | MOVING | TRUST AGREEMENTS | HEALTH CARE DIRECTIVES | TESTIMONIALS

Got Real Estate Questions? The Caton Team is here to help.

We strive to be more than just Realtors – we are also your home resource. If you have any real estate questions, concerns, need a referral, or some guidance – we are here for you. Contact us at your convenience – we are but a call, text, or click away!

The Caton Team believes, in order to be successful in the San Francisco | Peninsula | Bay Area | Silicon Valley Real Estate Market, we have to think and act differently. We do this by positioning our clients in the strongest light, representing them with the utmost integrity, while strategically maneuvering through negotiations and contracts. Together we make dreams come true.

A mother and daughter-in-law team with over 35 years of combined local Real Estate experience and knowledge – wouldn’t you like The Caton Team to represent you? Let us know how we can be of service. Contact us any time.

Cell | Sabrina 650.799.4333 | Susan 650.796.0654 | EMAIL | WEB| BLOG

The Caton Team – Susan & Sabrina

A Family of Realtors

Effective. Efficient. Responsive.

What can we do for you?

Website | The Caton Team Testimonials | Our Blog – The Real Estate Beat | Search for Homes | Facebook | Instagram | HomeSnap | Pinterest | LinkedIn Sabrina | Photography | Photography Blog

Berkshire Hathaway HomeServices – Drysdale Properties, Redwood City Ca.

DRE # | Sabrina 01413526 | Susan 01238225 | Team 70000218 | Office 01499008

The Caton Team does not receive compensation for any posts. Information is deemed reliable but not guaranteed. Third-party information not verified.

:max_bytes(150000):strip_icc():format(webp)/DesireeBurns_TopangaCanyon_003_web-aeebaeef9e6140adaa5e7cdce7e51619.jpg)

:max_bytes(150000):strip_icc():format(webp)/GettyImages-1271113589-ebc13481c7eb4ee3aece132992428145.jpg)

:max_bytes(150000):strip_icc():format(webp)/9ca65e_496c9454e27f46c595fa7746d5a00e4bmv2-ef80ca3a009349c3978cce1de1bd3bb5.jpg)

:max_bytes(150000):strip_icc():format(webp)/FremontSt-30-ae68c38ad90841bd9f7882ca3d8aa5fd.jpg)

:max_bytes(150000):strip_icc():format(webp)/House_Nine_Design_Zanna_our_surrey_nest3509_9ba9511d-442f-4f3a-b340-33545de7429c_1000x-ccba7e4bc03f4bbc9ea2f85ba8428540.jpg)

:max_bytes(150000):strip_icc():format(webp)/CarinaSkrobeckiPhoto_JessicaNelsonDesign_3339CascadeAve098-be1a004c3c3d449888776b590151fcbf.jpg)

:max_bytes(150000):strip_icc():format(webp)/CASSPhoto_JND_Zevely11-c2120fc016664816927fd6f32a23a433.jpeg)

You must be logged in to post a comment.