A shout out to my friend and lender Christian Carr – NMLS #1466899 for posting this information I felt I should share here.

The Federal Housing Administration (FHA) updates its loan limits and the mechanics of its loan programs each year. For 2025, there are key changes that homebuyers—especially first-time and moderate-income borrowers—should be aware of.

FHA Loan Limits in 2025

• Single-family homes: Loan limits range from $524,225 in low-cost areas (floor limit) to $1,209,750 in high-cost counties (ceiling limit).

• Multi-unit properties:

◦ 2-unit: $671,200 – $1,548,975

◦ 3-unit: $811,275 – $1,872,225

◦ 4-unit: $1,008,300 – $2,326,875

• These limits are tied to median home prices and align with conforming loan ceilings set by the FHFA ($806,500 standard / $1,209,750 high-cost).

Why it matters: Higher limits allow FHA financing for more expensive homes without needing a jumbo mortgage.

FHA Repayment Terms & Refinancing Options

✅ Fixed Terms and Gradual Payment Options

• Standard FHA mortgages come with 15- and 30-year terms

• Graduated Payment Mortgages (GPMs) are also available, allowing payments to increase gradually (e.g., 2.5%–7.5% annually) during the first 5–10 years before leveling out en.wikipedia.org.

🔄FHA Refinance Programs (2025 Highlights)

FHA homeowners may refinance under four main options:

1 Simple Refinance – Switch from one FHA loan to another to lower rate or shorten term, requires appraisal.

2 Streamline Refinance – Less documentation, sometimes no appraisal or credit check, must show “net tangible benefit” and have made 6+ on-time payments.

3 Cash‑Out Refinance – Access up to 85% equity for any purpose; requires appraisal.

4 203(k) Rehab Refinance – Finance purchase or refinance plus home improvements; available for primary residences only.

What Buyers Should Know

• Loan limits expanded in 2025—check your county limits via the HUD lookup tool.

• Graduated Payment Mortgages can help match payments to growing incomes—especially useful for younger buyers.

• Streamline refinances are attractive for existing FHA homeowners: minimal paperwork, faster turnaround—but closing costs apply (~3–6%).

• Cash‑out and 203(k) options remain available, but careful consideration of equity use and repayment ability is essential.

Final Thoughts

If you’re shopping for a new home or refinancing in 2025, FHA’s expanded limits can open more opportunities. Whether you’re looking to lower your rate, tap into equity, or finance renovations, FHA offers versatile programs—but it’s important to choose based on your goals and ability to repay. To verify your specific county’s limit, visit the official HUD lookup tool . For details on repayment plan options, review FHA’s official policy handbook or speak to an FHA-approved lender.

Cell| Sabrina 650.799.4333 |Susan 650.796.0654 | EMAIL | WEB| BLOG

We love what we do and would love to help you navigate your sale or purchase of Residential Real Estate. Please reach out for a personal consultation. Please enjoy our free resources below and get to know our team from our TESTIMONIALS.

Effective. Efficient. Responsive. The Caton Team 🏡

Got Real Estate Questions? The Caton Team is here to help.

We strive to be more than just Realtors – we are also your home resource. If you have any real estate questions, concerns, need a referral, or some guidance – we are here for you. Contact us at your convenience – we are but a call, text, or click away!

The Caton Team believes, in order to be successful in the San Francisco | Peninsula | Bay Area | Silicon Valley Real Estate Market, we have to think and act differently. We do this by positioning our clients in the strongest light, representing them with the utmost integrity, while strategically maneuvering through negotiations and contracts. Together we make dreams come true.

A mother and daughter-in-law team with over 35 years of combined local Real Estate experience and knowledge – wouldn’t you like The Caton Team to represent you? Let us know how we can be of service. Contact us any time.

Cell | Sabrina 650.799.4333 | Susan 650.796.0654 | EMAIL | WEB| BLOG

The Caton Team – Susan & Sabrina A Family of Realtors Effective. Efficient. Responsive. What can we do for you?

Mortgage rates play a crucial role in determining how much you’ll pay for your home over time. As a first-time homebuyer, understanding these rates can help you make informed financial decisions and secure the best possible loan terms. Here’s what you need to know.

1. What Are Mortgage Rates?

Mortgage rates are the interest rates lenders charge on home loans. These rates fluctuate based on economic conditions, lender policies, and your financial profile. Even a small change in interest rates can significantly impact your monthly payments and the total cost of your loan.

2. Factors That Influence Mortgage Rates

Several factors affect mortgage rates, including:

Credit Score: Higher scores typically secure lower rates.

Loan Term: Shorter loan terms often have lower rates.

Down Payment: A larger down payment may qualify you for better rates.

Market Conditions: Economic trends, inflation, and Federal Reserve policies impact interest rates.

3. Fixed vs. Adjustable Rates

Fixed-Rate Mortgages: The interest rate remains the same throughout the loan term, offering stability.

Adjustable-Rate Mortgages (ARMs): The interest rate may change periodically based on market conditions, potentially lowering initial costs but increasing future payments.

4. How to Secure the Best Mortgage Rate

To get the lowest possible mortgage rate:

Improve your credit score before applying.

Shop around and compare offers from multiple lenders.

Consider a larger down payment.

Lock in your rate when conditions are favorable.

Understanding mortgage rates empowers you to make smart financial choices and secure an affordable home loan.

Cell| Sabrina 650.799.4333 |Susan 650.796.0654 | EMAIL | WEB| BLOG

We love what we do and would love to help you navigate your sale or purchase of Residential Real Estate. Please reach out for a personal consultation. Please enjoy our free resources below and get to know our team from our TESTIMONIALS.

Effective. Efficient. Responsive. The Caton Team 🏡

Got Real Estate Questions? The Caton Team is here to help.

We strive to be more than just Realtors – we are also your home resource. If you have any real estate questions, concerns, need a referral, or some guidance – we are here for you. Contact us at your convenience – we are but a call, text or click away!

The Caton Team believes, in order to be successful in the San Fransisco | Peninsula | Bay Area | Silicon Valley Real Estate Market we have to think and act differently. We do this by positioning our clients in the strongest light, representing them with the utmost integrity, while strategically maneuvering through negotiations and contracts. Together we make dreams come true.

A mother and daughter-in-law team with over 35 years of combined, local Real Estate experience and knowledge – wouldn’t you like The Caton Team to represent you? Let us know how we can be of service. Contact us any time.

Cell | Sabrina 650.799.4333 | Susan 650.796.0654 | EMAIL | WEB| BLOG

The Caton Team – Susan & Sabrina A Family of Realtors Effective. Efficient. Responsive. What can we do for you?

Nearly one in three renters admit to delaying a home purchase because of misgivings about the mortgage process. Here’s how you can get them on the right page.

Americans are confused about mortgages and many other financial aspects of homeownership, according to a new survey of about 1,000 prospective buyers and homeowners conducted by JW Surety Bonds. Read the whole survey HERE.

One in three renters say their lack of knowledge about homeownership has caused them to delay a home purchase, while homeowners admit to making some costly mistakes in the homebuying process because of a low homeownership IQ.

Real estate professionals must play the role of an educator, helping to clear up their clients’ misunderstanding about a home purchase. “It’s clear that improved education and resources could help foster Americans’ homeownership success,” researchers note in the JW Surety Bonds survey. “As the housing market continues to change, so must our approach to homeownership literacy.”

The Gaps in Homebuying Knowledge

Aside from confusion about mortgages, home buyers also appear to misunderstand the added costs involved when buying a home, such as closing costs and property maintenance. The JW Surety Bonds survey uncovered the following consumer knowledge gaps about homeownership:

Unaware of key real estate terms. One in eight buyers surveyed could not accurately define what a “mortgage” is, and 43% were unsure of the meaning of “mortgage rate,” the survey found. That knowledge gap may be alarming, considering that 74% of buyers financed their home purchase with a mortgage in 2024. You can provide your clients with NAR’s Consumer Guide on mortgages and financing, as well as a customer handout on loan and lending terms to know.

Not budgeting for hidden homeownership expenses. More than a quarter of homeowners—27%—say they were caught off guard about unexpected fees during the homebuying process, according to JW Surety Bonds’ research. Real estate professionals can help their clients prepare for the added costs, such as property taxes, homeowners insurance, homeowners association fees (if applicable) and routine property maintenance. (Most financial advisers recommend saving 1% to 2% of the home’s purchase price annually.) What’s more, 40% of homeowners say they do not use an escrow account to pay their property taxes, which could expose them to large annual tax bills, the survey’s researchers caution. You can provide your clients with NAR’s Consumer Guides on homeowners insurance—including specific guidance on flood and fire coverage—and escrow and earnest money. Also, you can share a comprehensive overview of transactions involving homeowners associations.

Not paying attention to home affordability. Some home buyers may be at risk of overspending on their home purchase. It could lead to buyer’s remorse: One in nine homeowners say they regret buying their home due to unexpected costs they learned about only after closing. Further, one in nine homeowners say they spend more than 50% of their monthly income on housing costs—a percentage that most financial experts would consider severely “cost-burdened.” Another 36% of homeowners say they did not have an emergency fund to cover unexpected home repairs, leaving them vulnerable to further financial strain, the survey notes. You can share NAR’s Consumer Guide on preparing for homeownership and provide a customer handout with a worksheet to track your clients’ budgets.

Where Home Buyers Can Turn for Guidance

Some prospective home buyers are on the lookout for more answers and guidance on the homebuying process. NAR has many Consumer Guides covering various aspects of the process, from written buyer agreements to home inspections and appraisals, at facts.realtor. Here are other top sources consumers cite for gathering homeownership information, according to the JW Surety Bonds survey:

Friends or family: 64%

Articles or blogs: 49%

Real estate agents: 31%

YouTube: 29%

Financial advisers: 17%

Online courses: 14%

TikTok: 13%

How Real Estate Agents Can Improve Homebuying Education

Real estate professionals may be able to help improve their clients’ homeownership literacy while also expanding their outreach. Try this:

Host education seminars. Team with lenders or financial advisers to offer buyers education seminars that highlight the financial aspects of a home purchase, such as the types of loans available and getting pre-approved for a mortgage. Loans and grants for first-time home buyers may help your clients better afford homeownership.

Talk real estate on social media. Glennda Baker, an associate broker with Glennda Baker + Associates, Inc., in Atlanta, has amassed more than 870,000 followers on TikTok with her short-form real estate education videos. Her videos cover a range of topics, including homebuying mistakes, financing a home purchase and living under a homeowners association.

Customize your consumer handouts. Publish content on your blogs and newsletters and provide handouts about the various aspects of home buying. REALTOR® Magazine offers customizable client education and handouts that detail the steps involved in a home purchase, from financing to closing.

We love what we do and would love to help you navigate your sale or purchase of Residential Real Estate. Please reach out for a personal consultation. Please enjoy our free resources below and get to know our team from our TESTIMONIALS.

Effective. Efficient. Responsive. The Caton Team 🏡 How can The Caton Team help You?

Got Real Estate Questions? The Caton Team is here to help.

We strive to be more than just Realtors – we are also your home resource. If you have any real estate questions, concerns, need a referral, or some guidance – we are here for you. Contact us at your convenience – we are but a call, text or click away!

The Caton Team believes, in order to be successful in the San Fransisco | Peninsula | Bay Area | Silicon Valley Real Estate Market we have to think and act differently. We do this by positioning our clients in the strongest light, representing them with the utmost integrity, while strategically maneuvering through negotiations and contracts. Together we make dreams come true.

A mother and daughter-in-law team with over 35 years of combined, local Real Estate experience and knowledge – wouldn’t you like The Caton Team to represent you? Let us know how we can be of service. Contact us any time.

Call| Text | Sabrina 650.799.4333 | Susan 650.796.0654 | EMAIL | WEB| BLOG

The Caton Team – Susan & Sabrina A Family of Realtors Effective. Efficient. Responsive. What can we do for you?

If you’re getting ready to buy a home, it’s exciting to jump a few steps ahead and think about moving in and making it your own. But before you get too far down the emotional path, there are some key things to keep in mind after you apply for your mortgage and before you close. Here’s a list of things to remember when you apply for your home loan. SOURCE

Don’t Deposit Large Sums of Cash

Lenders need to source your money, and cash isn’t easily traceable. Before you deposit any cash into your accounts, discuss the proper way to document your transactions with your loan officer.

Don’t Make Any Large Purchases

It’s not just home-related purchases that could disqualify you from your loan. Any large purchases can be red flags for lenders. People with new debt have higher debt-to-income ratios (how much debt you have compared to your monthly income). Since higher ratios make for riskier loans, borrowers may no longer qualify for their mortgage. Resist the temptation to make any large purchases, even for furniture or appliances.

Don’t Cosign Loans for Anyone

When you cosign for a loan, you’re making yourself accountable for that loan’s success and repayment. With that obligation comes higher debt-to-income ratios as well. Even if you promise you won’t be the one making the payments, your lender will have to count them against you.

Don’tSwitch Bank Accounts

Lenders need to source and track your assets. That task is much easier when there’s consistency among your accounts. Before you transfer any money, speak with your loan officer.

Don’t Apply for New Credit

It doesn’t matter whether it’s a new credit card or a new car. When your credit report is run by organizations in multiple financial channels (mortgage, credit card, auto, etc.), it will have an impact on your FICO® score. Lower credit scores can determine your interest rate and possibly even your eligibility for approval.

Don’t Close Any Accounts

Many buyers believe having less available credit makes them less risky and more likely to be approved. This isn’t true. A major component of your score is your length and depth of credit history (as opposed to just your payment history) and your total usage of credit as a percentage of available credit. Closing accounts has a negative impact on both of those parts of your score.

Do Discuss Changes with Your Lender

Be upfront about any changes that occur or you’re expecting to occur when talking with your lender. Blips in income, assets, or credit should be reviewed and executed in a way that ensures your home loan can still be approved. If your job or employment status has changed recently, share that with your lender as well. Ultimately, it’s best to fully disclose and discuss your intentions with your loan officer before you do anything financial in nature.

Bottom Line

You want your home purchase to go as smoothly as possible. Remember, before you make any large purchases, move your money around, or make major life changes, be sure to consult your lender – someone who’s qualified to explain how your financial decisions may impact your home loan.

Got Questions? The Caton Team is here to help.

Call| Text | Sabrina 650.799.4333 |Susan 650.796.0654 | EMAIL | WEB| BLOG

We love what we do and would love to help you navigate your sale or purchase of Residential Real Estate. Please reach out for a personal consultation. Please enjoy our free resources below and get to know our team from our TESTIMONIALS.

Effective. Efficient. Responsive. The Caton Team 🏡 How can The Caton Team help You?

Got Real Estate Questions? The Caton Team is here to help.

We strive to be more than just Realtors – we are also your home resource. If you have any real estate questions, concerns, need a referral, or some guidance – we are here for you. Contact us at your convenience – we are but a call, text or click away!

The Caton Team believes, in order to be successful in the San Fransisco | Peninsula | Bay Area | Silicon Valley Real Estate Market we have to think and act differently. We do this by positioning our clients in the strongest light, representing them with the utmost integrity, while strategically maneuvering through negotiations and contracts. Together we make dreams come true.

A mother and daughter-in-law team with over 35 years of combined, local Real Estate experience and knowledge – wouldn’t you like The Caton Team to represent you? Let us know how we can be of service. Contact us any time.

Call| Text | Sabrina 650.799.4333 | Susan 650.796.0654 | EMAIL | WEB| BLOG

The Caton Team – Susan & Sabrina A Family of Realtors Effective. Efficient. Responsive. What can we do for you?

There’s a lot of discussion about affordability as home prices continue to appreciate rapidly. Even though the most recent index on affordability from the National Association of Realtors (NAR) shows homes are more affordable today than the historical average, some still have concerns about whether or not it’s truly affordable to buy a home right now.

When addressing this topic, there are various measures of affordability to consider. However, very few of the indexes compare the affordability of owning a home to renting one. In a paper just published by the Urban Institute, Homeownership Is Affordable Housing, author Mike Loftin examines whether it’s more affordable to buy or rent. Here are some of the highlights included.

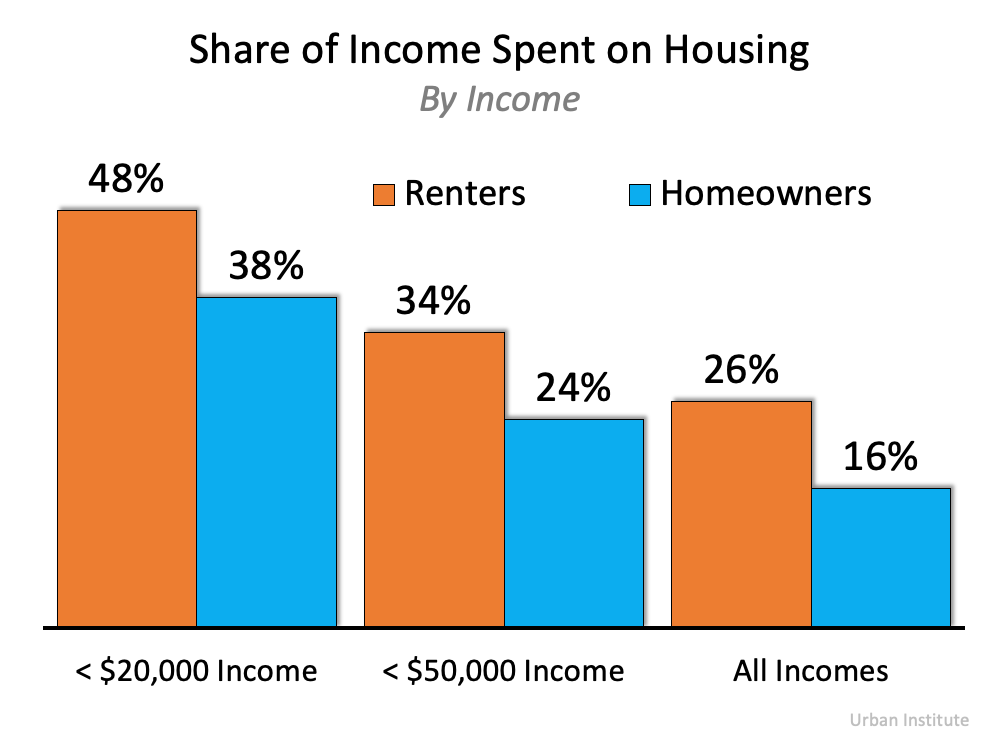

1. Renters pay a higher percentage of their income toward their rental payment than homeowners pay toward their mortgage.

The report explains:

“When we look at the median housing expense ratio of all households, the typical homeowner household spends 16 percent of its income on housing while the typical renter household spends 26 percent. This is true, you might say, because people who own their own home must make more money than people who rent. But if we control for income, it is still more affordable to own a home than to rent housing, on average.”

Here’s the data from the report shown in a graph:

2. Renters don’t have extra money to invest in other assets.

The report goes on to say:

“Buying a home is not a decision between investing in real estate versus investing in stocks, as financial advisers often claim. Instead, the home buying investment simply converts some portion of an existing expense (renting) into an investment in real estate.”

It explains that you still have a housing expense (rent payments) even if you don’t buy a home. You can’t live in your 401K, but you can transfer housing expenses to your real estate investment. A mortgage payment is forced savings; it goes toward building equity you will likely get back when you sell your home. There’s no return on your rent payments.

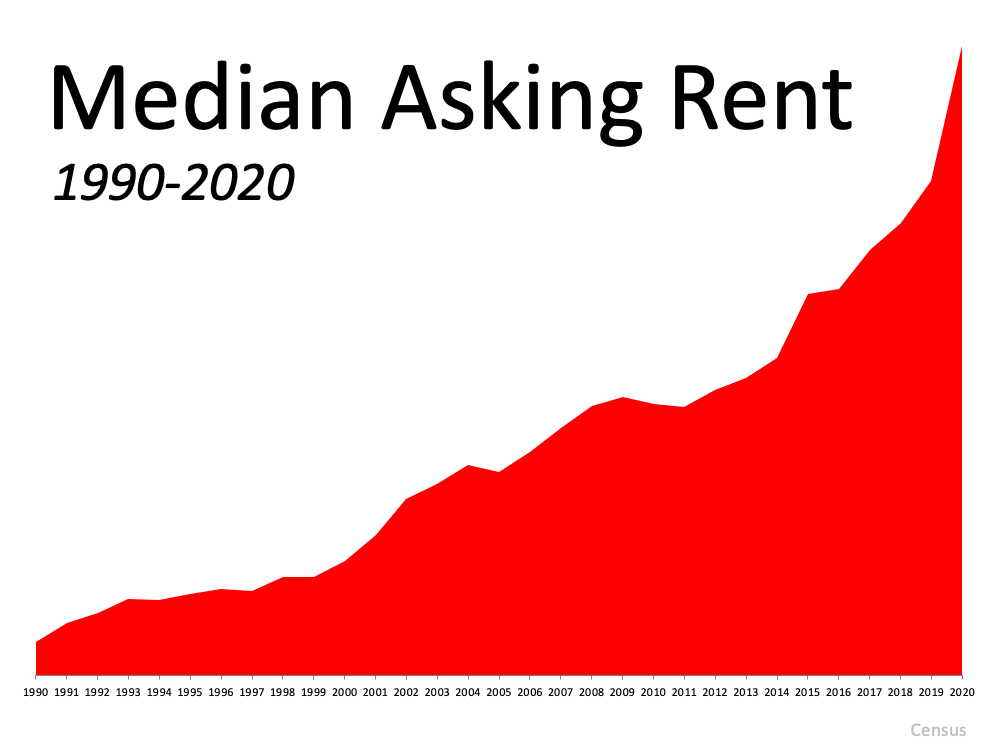

3. Your mortgage payment remains relatively the same over time. Your rent keeps going up.

The report also notes:

“Whereas renters are continuously vulnerable to cost increases, rising home prices do not affect homeowners. Nobody rebuys the same home every year. For the homeowner with a fixed-rate mortgage, monthly payments increase only if property taxes and property insurance costs increase. The principal and interest portion of the payment, the largest portion, is fixed. Meanwhile, the renter’s entire payment is subject to inflation.

Consequently, over time, the homeowner’s and renter’s differing trajectories produce starkly different economic outcomes. Homeownership’s major affordability benefit is that it stabilizes what is likely the homeowner’s biggest monthly expense, assuming a buyer has a fixed-rate mortgage, which most American homeowners do. The only portion of the homeowner’s housing expenses that can increase is taxes and insurance. The principal and interest portion stays the same for 30 years.”

A mortgage payment remains about the same over the 30 years of the mortgage. Here’s what rents have done over the last 30 years:

4. If you want to own a home and can afford it, waiting could cost you.

As the report also indicates:

“We need to stop seeing housing as a reward for financial success and instead see it as a critical tool that can facilitate financial success. Affordable homeownership is not the capstone of economic well-being; it is the cornerstone.”

Homeownership is the first rung on the ladder of financial success for most households, as their home is most often their largest asset.

Bottom Line

If the current headlines reporting a supposed drop-off in home affordability are making you nervous, let’s connect to go over the real insights into our area.

Whether you’re just starting your journey in Real Estate or you’ve bought and sold before you can trust – The Caton Team to be your guides. We’ve built our business on trust, honesty, communication, respect, loyalty, wisdom, and knowledge. Each client is unique – please reach out for a personal consultation or read our blog HERE.

Got Questions? The Caton Team is here to help.

Call| Text | Sabrina 650.799.4333 |EMAIL | WEB| BLOG

We love what we do and would love to help you navigate your sale or purchase of Residential Real Estate. Please reach out for a personal consultation. Please enjoy our free resources below and get to know our team from our TESTIMONIALS.

Got Real Estate Questions? The Caton Team is here to help.

We strive to be more than just Realtors – we are also your home resource. If you have any real estate questions, concerns, need a referral, or some guidance – we are here for you. Contact us at your convenience – we are but a call, text or click away!

The Caton Team believes, in order to be successful in the San Fransisco | Peninsula | Bay Area | Silicon Valley Real Estate Market we have to think and act differently. We do this by positioning our clients in the strongest light, representing them with the utmost integrity, while strategically maneuvering through negotiations and contracts. Together we make dreams come true.

A mother and daughter-in-law team with over 35 years of combined, local Real Estate experience and knowledge – wouldn’t you like The Caton Team to represent you? Let us know how we can be of service. Contact us any time.

Call| Text | Sabrina 650.799.4333 | Susan 650.796.0654 |EMAIL | WEB| BLOG

The Caton Team – Susan & Sabrina A Family of Realtors Effective. Efficient. Responsive. What can we do for you?

You may have been told that it’s important to get pre-approved at the beginning of the homebuying process, but what does that really mean, and why is it so important? Especially in today’s market, with rising buyer competition, it’s crucial to have a clear understanding of your budget so you stand out to sellers as a serious homebuyer.

Being intentional and competitive are musts when buying a home right now. Pre-approval from a lender is the only way to know your true price range and how much money you can borrow for your loan. Just as important, being able to present a pre-approval letter shows sellers you’re a qualified buyer, something that can really help you land your dream home in an ultra-competitive market.

With limited housing inventory, there are many more buyers active in the market than there are sellers, and that’s creating some serious competition. According to the National Association of Realtors (NAR), homes are receiving an average of 5.1 offers for sellers to consider. As a result, bidding wars are more and more common. Pre-approval gives you an advantage if you get into a multiple-offer scenario, and these days, it’s likely you will. When a seller knows you’re qualified to buy the home, you’re in a better position to potentially win the bidding war.

“By having a pre-approval letter from your lender, you’re telling the seller that you’re a serious buyer, and you’ve been pre-approved for a mortgage by your lender for a specific dollar amount. In a true bidding war, your offer will likely get dropped if you don’t already have one.”

Every step you can take to gain an advantage as a buyer is crucial when today’s market is constantly changing. Interest rates are low, prices are going up, and lending institutions are regularly updating their standards. You’re going to need guidance to navigate these waters, so it’s important to have a team of professionals such as a loan officer and a trusted real estate agent making sure you take the right steps and can show your qualifications as a buyer when you find a home to purchase.

Bottom Line

In a competitive market with low inventory, a pre-approval letter is a game-changing piece of the homebuying process. Not only does being pre-approved bring clarity to your homebuying budget, but it shows sellers how serious you are about purchasing a home.

Whether you’re just starting your journey in Real Estate or you’ve bought and sold before you can trust – The Caton Team to be your guides. We’ve built our business on trust, honesty, communication, respect, loyalty, wisdom, and knowledge. Each client is unique – please reach out for a personal consultation or read our blog HERE.

Got Questions? The Caton Team is here to help.

Call| Text | Sabrina 650.799.4333 |EMAIL | WEB| BLOG

We love what we do and would love to help you navigate your sale or purchase of Residential Real Estate. Please reach out for a personal consultation. Please enjoy our free resources below and get to know our team from our TESTIMONIALS.

Got Real Estate Questions? The Caton Team is here to help.

We strive to be more than just Realtors – we are also your home resource. If you have any real estate questions, concerns, need a referral, or some guidance – we are here for you. Contact us at your convenience – we are but a call, text or click away!

The Caton Team believes, in order to be successful in the San Fransisco | Peninsula | Bay Area | Silicon Valley Real Estate Market we have to think and act differently. We do this by positioning our clients in the strongest light, representing them with the utmost integrity, while strategically maneuvering through negotiations and contracts. Together we make dreams come true.

A mother and daughter-in-law team with over 35 years of combined, local Real Estate experience and knowledge – wouldn’t you like The Caton Team to represent you? Let us know how we can be of service. Contact us any time.

Call| Text | Sabrina 650.799.4333 | Susan 650.796.0654 |EMAIL | WEB| BLOG

The Caton Team – Susan & Sabrina A Family of Realtors Effective. Efficient. Responsive. What can we do for you?

Here is an excerpt from the excellent website, Mortgage New Daily:

Before you stop paying your bills in the hope of cashing in, let’s separate fact from fiction. First and most importantly, you will absolutely NOT get a better deal on a mortgage rate if your credit score is lower, even if your nephew just texted you a screenshot of a news headline saying “620 FICO SCORE GETS A 1.75% FEE DISCOUNT” and “740 FICO SCORE PAYS 1% FEE.” MATTHEW GRAHAM – MORTGAGE NEWS DAILY

I strongly encourage you to read the rest of his article here: https://www.mortgagenewsdaily.com/markets/mortgage-rates-04212023 It is well-written and informative and takes the political bias and opinion out of the explanation. Just the facts. And yes, it has gotten more expensive to get a home loan–for everyone.

But to really understand what’s changed, you need to first understand that mortgage rates have a price. In other words, each rate on a rate sheet is associated with a price or fee and that price/fee goes up and and down with the rate you choose, based on how much money you want to borrower, what your credit score is and how much down payment you’re bringing to the purchase. There are a few other factors that determine rate and that is why it is so difficult to answer your question: “What are rates like today?”

With that out of the way, sometimes an interest rate comes at cost to you (that’s what we all know as “Points”) and sometimes that price/fee is a rebate to you (that’s how some lenders will quote you a “no cost loan”). What’s in the middle is something called “PAR”. This is the fancy Wall Street word for “Neutral”, meaning you don’t pay points and you don’t get a rebate. The price for mortgage rates has been increased at the direction of the Federal Housing Finance Administration because they don’t believe they are making enough money and raising these fees (because inflation). The FHFA believes this will help them maintain the financial health of Fannie Mae and Freddie Mac–the two Government Sponsored Entities that purchase many of the home loans that are originated in the United States.

Here’s a picture proving that home loans for the purpose of purchasing just got more expensive for us all:

Now, Fannie and Freddie have what is called a “Duty to Serve” and that requires them to be focused on helping first time home buyers get into homes. That is why the chart above shows that a smaller down payment and a lower credit scores appears to be getting a better deal than say someone with higher credit and a larger down payment.

But let’s take the following example, if you have two borrowers, one with a 700 FICO and 20% down, and another with 640 and 5% down, the LLPAs (1.500%) are in fact the same, creating an “equal” playing field. However, if you have both come in with 5% the higher FICO score gets an improvement to LLPA of 0.625%, whereas if the lower FICO borrower comes in with 20%, their LLPA is 1.375% higher. With the latter, a mortgage of $600,000 results in $8,250 of additional costs to the lower credit score borrower. The point here is that the FHFA is working to create more affordable housing for those that have lower credit scores and by assumption a smaller down payment.

After Weeks of Decline, Mortgage Rates Increase

For the first time in over a month, mortgage rates moved up due to shifting market expectations. Home prices have stabilized somewhat, but with supply tight and rates stuck above six percent, affordable housing continues to be a serious issue for potential homebuyers. Unless rates drop into the mid five percent range, demand will only modestly recover.

The latest data showed signs of strength in the housing market while the labor sector is getting weaker. Plus, an important recession signal continues to reflect a slowing economy. Don’t miss these stories:

What the Media Gets Wrong About Home Prices

Home Builders Need to be “Starting” Something

NAHB Reports Cautious Optimism Among Home Builders

Job Market Getting Weaker

Recession Signal Flashing

What the Media Gets Wrong About Home Prices

Existing Home Sales fell 2.4% from February to March to a 4.44 million unit annualized pace, per the National Association of Realtors (NAR), which was in line with estimates. Sales were 22% lower than they were in March of last year. This report measures closings on existing homes, which represent around 90% of the market, making it a critical gauge for taking the pulse of the housing sector.

What’s the bottom line? While it’s true that buyer activity slowed in March, February was an especially strong month for closings, so a slight pullback last month was understandable.

In addition, multiple data points suggest that demand remains strong. Homes stayed on the market on average for 29 days, down sharply from 34 days in February. Plus, 65% of homes sold in March were on the market for less than a month, which is up from 57% and shows homes are selling quickly when they’re priced correctly. Meanwhile, investors accounted for 17% of transactions last month, making up roughly one out of every six deals. Clearly investors are seeing the opportunity in housing right now.

Also of note, there was a 0.9% decline in the median home price to $375,700 from a year earlier. However, this is not the same as a decline in home prices as some media reports implied.

The median home price simply means half the homes sold were above that price and half were below it, and this figure can be skewed by the mix of sales among lower-priced and higher-priced homes. In fact, we could see home prices increase across all price categories, but the median price could still fall if the concentration of sales was on the lower end. Actual appreciation numbers are higher, not lower, on a year-over-year basis according to key reports from Case-Shiller, CoreLogic and the Federal Housing Finance Agency.

Home Builders Need to be “Starting” Something

Construction of new homes slowed in March, with Housing Starts falling nearly 1% from February. Building Permits, which are indicative of future supply, also fell 8.8% for the month. While Starts and Permits for single-family homes both ticked higher from February to March, they were significantly lower than in March of last year.

What’s the bottom line? The housing sector is undersupplied, and not enough inventory is heading to the market. Starts for single-family homes have been on a downward trend over the last year, with the pace of 1.191 million units in March 2022 falling all the way to 861,000 units this March. Single-family permits have followed the same pattern, declining from a pace of 1.163 million units to 818,000 over the same period.

With single-family homes remaining in high demand among buyers, the imbalance between supply and demand should continue to be supportive of prices.

NAHB Reports Cautious Optimism Among Home Builders

The National Association of Home Builders (NAHB) Housing Market Index, which is a near real-time read on builder confidence, rose one point to 45 in April, marking the fourth straight month this measure has increased. Among the components of the index, current sales conditions rose two points to 51 while sales expectations for the next six months increased three points to 50. Buyer traffic remained unchanged at 31.

What’s the bottom line? Home builder confidence has now risen 14 points since the low of 31 in December. Present sales conditions returned to expansion territory (over 50) for the first time since last September, while the future sales outlook is right at the breakeven between expansion and contraction at its highest level since June. Even though the overall confidence reading remains below 50 in contraction territory, sentiment continues to rebound in the right direction.

Job Market Getting Weaker

Initial Jobless Claims continued to move higher this month, with the number of people filing for unemployment benefits for the first time rising by 5,000 in the latest week to 245,000. This tied the third highest reading so far this year. Continuing Jobless Claims also surged to 1.865 million, up 61,000.

What’s the bottom line? Continuing Claims measure people who continue to receive benefits after their initial claim is filed and this data clearly shows that hiring has slowed. While the number can be volatile from week to week, the overall trend has been higher with an increase of around 576,000 since the low reached last September.

Plus, there’s greater evidence of workforce reductions as the four-week average of Initial Jobless Claims, which smooths out some of the weekly fluctuation among first-time filers, has hovered around 240,000 at a yearly high in recent weeks.

Recession Signal Flashing

The Conference Board released their Leading Economic Index (LEI) for March, which was down 1.2%, falling to “its lowest level since November of 2020, consistent with worsening economic conditions ahead,” said Justyna Zabinska-La Monica, Senior Manager, Business Cycle Indicators. This report is a composite of economic indexes and can signal peaks and troughs in the business cycle.

What’s the bottom line? The Conference Board explained that a warning signal occurs when the LEI 6-month growth rate on an annualized basis breaks beneath 0%. But a break beneath -4.2%, like we saw last month, is a recession signal that has been highly accurate historically. The Conference Board also stated that they believe the U.S. will enter a recession “starting in mid-2023.”

What to Look for This Week

More housing news is ahead, starting with Tuesday’s release of home price appreciation data for February from the Case-Shiller Home Price Index and the Federal Housing Finance Agency (FHFA) House Price Index. March’s New Home Sales will also be reported on Tuesday, while Pending Home Sales follows on Thursday.

Also on Thursday, the latest Jobless Claims data will be released along with the first reading for first quarter 2023 GDP. Friday brings perhaps the biggest news of the week with March’s reading for the Fed’s favored inflation measure, Personal Consumption Expenditures.

Technical Picture

Mortgage Bonds were able to stay above their 50-day Moving Average after testing it earlier in the day last Friday. The 10-year tested support at its 200-day Moving Average but remained above it at the end of last week.

Shared From Lender Chris Carr NMLS# 1466899 – SOURCE

If you are considering a sale or purchase of Real Estate – The Caton Team would love to interview for the job as your Realtor. We love what we do, let us take care of you.

We believe to be successful in the Silicon Valley Real Estate Market we have to think and act differently. We do this by positioning our clients in the strongest light, representing them with integrity, while strategically maneuvering through negotiations and contracts.

A mother and daughter-in-law team with 40 years of combined, local real estate experience, knowledge, and know-how – wouldn’t you like The Caton Team to represent you? Let us know how we can be of service. Contact us any time. Call | Text | 650.799.4333 | Email | Info@TheCatonTeam.com

Effective. Efficient. Responsive. Got Questions? The Caton Team is here to help.

Call| Text | Sabrina 650.799.4333 |EMAIL | WEB| BLOG

We love what we do and would love to help you navigate your sale or purchase of Residential Real Estate. Please reach out for a personal consultation. Please enjoy our free resources below and get to know our team from our TESTIMONIALS.

Got Real Estate Questions? The Caton Team is here to help.

We strive to be more than just Realtors – we are also your home resource. If you have any real estate questions, concerns, need a referral, or some guidance – we are here for you. Contact us at your convenience – we are but a call, text or click away!

The Caton Team believes, in order to be successful in the San Fransisco | Peninsula | Bay Area | Silicon Valley Real Estate Market we have to think and act differently. We do this by positioning our clients in the strongest light, representing them with the utmost integrity, while strategically maneuvering through negotiations and contracts. Together we make dreams come true.

A mother and daughter-in-law team with over 35 years of combined, local Real Estate experience and knowledge – wouldn’t you like The Caton Team to represent you? Let us know how we can be of service. Contact us any time.

Call| Text | Sabrina 650.799.4333 | Susan 650.796.0654 |EMAIL | WEB| BLOG

The Caton Team – Susan & Sabrina A Family of Realtors Effective. Efficient. Responsive. What can we do for you?

The news is full of bad news – that’s why The Caton Team is here to change the narrative. Yes – rates did jump 2nd Quarter of 2022 and it rippled through the Real Estate Market. Today – late January 2023, rates have settled down a bit from their nightmarish high of around 7% – today we’re seeing 4.5-6% popping up again.

BUT… it’s still not the 3% we loved in 2021! So, if Buying Bay Area Real Estate is still a goal – when the news says the market is down – now is the time to act – so let’s talk about solutions.

Welcome Home Funding, a division of Berkshire Hathaway HomeServices, is offering two products to help wishful home buyers get into a home while the market is soft – i.e. – that short window when it’s a buyer’s market here in the Bay Area.

Welcome Home Funding is offering a RATE BUY DOWN. Take a look at the example below. Year 1 – the interest rate is nice and low, getting a buyer into a property and each year it goes up a point*.

Next up is the Welcome Home Funding – RATE REBOUND. No one knows when the market will peak or where interest rates will land but with RATE REBOUND a buyer can rest assured that if rates drop further they can take advantage of the lower rate with NO lender fees on the refinance within 5 years of their purchase AND get a $1000 credit to go towards third parties fees associated with refinancing – like the appraisal report and new credit pull. Please note this product has a promotional lifespan. Homes must be IN Contract by 6.30.2023 and Close Escrow by 9.30.23 to qualify. Please note lender fees do apply to the original purchase loan with Welcome Home Funding.

For more information – contact The Caton Team|Cell 650.799.4333|EMAIL|

Or Mike Kamienski with Welcome Home Funding |Cell (650) 484-6488 | EMAIL|

Got Questions? The Caton Team is here to help.

Call| Text | Sabrina 650.799.4333 |EMAIL | WEB| BLOG

We love what we do and would love to help you navigate your sale or purchase of Residential Real Estate. Please reach out at your convenience for a personal consultation. Please enjoy our free resources below and get to know our team through our clients’ words.Testimonials.

Got Real Estate Questions? The Caton Team is here to help.

We strive to be more than just Realtors – we are also your home resource. If you have any real estate questions, or concerns, or need a referral or some guidance – we are here for you. Contact us at your convenience – we are but a call, text, or click away!

The Caton Team believes, in order to be successful in the San Fransisco | Peninsula | Bay Area | Silicon Valley Real Estate Market we have to think and act differently. We do this by positioning our clients in the strongest light, representing them with the utmost integrity, while strategically maneuvering through negotiations and contracts. Together we make dreams come true.

A mother and daughter-in-law team with over 35 years of combined, local Real Estate experience and knowledge – wouldn’t you like The Caton Team to represent you? Let us know how we can be of service. Contact us any time.

Call| Text | Sabrina 650.799.4333 | Susan 650.796.0654 |EMAIL | WEB| BLOG

The Caton Team – Susan & Sabrina A Family of Realtors Effective. Efficient. Responsive. What can we do for you?

Once you’ve applied for a mortgage to buy a home, there are some key things to keep in mind. While it’s exciting to start thinking about moving in and decorating, be careful when it comes to making any big purchases. Here are a few things you may not realize you need to avoid after applying for your home loan.

Don’t Deposit Large Sums of Cash

Lenders need to source your money, and cash isn’t easily traceable. Before you deposit any amount of cash into your accounts, discuss the proper way to document your transactions with your loan officer.

Don’t Make Any Large Purchases

It’s not just home-related purchases that could disqualify you from your loan. Any large purchases can be red flags for lenders. People with new debt have higher debt-to-income ratios (how much debt you have compared to your monthly income). Since higher ratios make for riskier loans, borrowers may no longer qualify for their mortgages. Resist the temptation to make any large purchases, even for furniture or appliances.

Don’t Co-Sign Loans for Anyone

When you co-sign for a loan, you’re making yourself accountable for that loan’s success and repayment. With that obligation comes higher debt-to-income ratios as well. Even if you promise you won’t be the one making the payments, your lender will have to count the payments against you.

Don’t Switch Bank Accounts

Lenders need to source and track your assets. That task is much easier when there’s consistency among your accounts. Before you transfer any money, speak with your loan officer.

Don’t Apply for New Credit

It doesn’t matter whether it’s a new credit card or a new car. When you have your credit report run by organizations in multiple financial channels (mortgage, credit card, auto, etc.), it will have an impact on your FICO® score. Lower credit scores can determine your mortgage interest rate and possibly even your eligibility for approval.

Don’t Close Any Accounts

Many buyers believe having less available credit makes them less risky and more likely to be approved. This isn’t true. A major component of your score is your length and depth of credit history (as opposed to just your payment history) and your total usage of credit as a percentage of available credit. Closing accounts has a negative impact on both of those aspects of your score.

In Short, Consult an Expert

To sum it up, be upfront about any changes when talking with your lender. Blips in income, assets, or credit should be reviewed and executed in a way that ensures your home loan can still be approved. If your job or employment status has changed recently, share that with your lender as well. Ultimately, it’s best to fully disclose and discuss your intentions with your loan officer before you do anything financial in nature.

Bottom Line

You want your home purchase to go as smoothly as possible. Remember, before you make any large purchases, move your money around, or make any major life changes, be sure to consult your lender – someone who’s qualified to explain how your financial decisions may impact your home loan.

My Two Cents: Your home loan is the most important part of your homeowner journey. The Loan Approval is literally a snapshot of your current financial picture and you DO NOT want to change that picture. If you need to move money around, gather gift funds, pay off debt, etc – do so BEFORE YOU APPLY and keep a paper trail! However, The Caton Team highly recommends that you speak with a lender before you do anything. This ensures you’re doing the right things that do not impact your credit score negatively.

Got Questions? The Caton Team is here to help.

Call| Text | Sabrina 650.799.4333 |EMAIL | WEB| BLOG

We love what we do and would love to help you navigate your sale or purchase of Residential Real Estate. Please reach out at your convenience for a personal consultation. Please enjoy our free resources below and get to know our team through our clients’ words.Testimonials.

Got Real Estate Questions? The Caton Team is here to help.

We strive to be more than just Realtors – we are also your home resource. If you have any real estate questions, concerns, need a referral or some guidance – we are here for you. Contact us at your convenience – we are but a call, text or click away!

The Caton Team believes, in order to be successful in the San Fransisco | Peninsula | Bay Area | Silicon Valley Real Estate Market we have to think and act differently. We do this by positioning our clients in the strongest light, representing them with the utmost integrity, while strategically maneuvering through negotiations and contracts. Together we make dreams come true.

A mother and daughter-in-law team with over 35 years of combined, local Real Estate experience and knowledge – would’t you like The Caton Team to represent you? Let us know how we can be of service. Contact us any time.

Call| Text | Sabrina 650.799.4333 | Susan 650.796.0654 |EMAIL | WEB| BLOG

The Caton Team – Susan & Sabrina A Family of Realtors Effective. Efficient. Responsive. What can we do for you?

When Nicholas Dahl, 36, called Chase Bank to find out about his options for mortgage forbearance at the end of March, an automated voice informed him the wait time would be 43 hours and 45 minutes. Dahl, who runs his family’s art transportation business, hasn’t been able to draw a paycheck since all nonessential businesses in Illinois were shuttered on March 21 due to the coronavirus pandemic. And he doesn’t know how much longer he and his wife will be able to keep making payments on the three-bedroom house in the Chicago suburbs where they’re raising their 8-year-old daughter.

After three hours and 45 minutes on hold, and several times where he heard a woman saying “hello” before going back to the call music, he finally hung up. He emailed the bank for information instead.

Chase responded that he could receive mortgage forbearance for 90 days. During those three months, Dahl wouldn’t have to make his payments and wouldn’t incur late fees, get reported to credit agencies, or risk foreclosure. But once that period was over? All of the missed payments would come due at once.

(After this piece was published, a Chase Home Lending spokesperson contacted us with this statement. “Over these 90 days we will be in communication with our customers to make sure they have the help they need. … We’re just holding tight for [government agency] guidance on how to handle each of these loans.”)

“I don’t really think it’s worth it,” says Dahl, who’s losing about $5,000 in income each month his business is closed. “I don’t really want to pay four mortgage payments in one.”

Dahl is one of many thousands of Americans who are having trouble making their monthly mortgage payments due to the coronavirus pandemic—or will soon, if the crisis drags on. In the past month, nearly 17 million Americans have filed for unemployment as shelter-in-place orders, social distancing measures, and nonessential business closures went into effect. Last week, economists estimated the unemployment rate was about 13%—worse than during the Great Recession. And those numbers don’t even include many out-of-work, self-employed, and gig workers along with those who’ve had trouble filing their claims because unemployment offices are overwhelmed.

The widespread misery spread by COVID-19 has left many homeowners scrambling to figure out how to pay their mortgages. Homeowners with government-backed loans—and even many without—are being offered up to 12 months of forbearance, doled out in 90-day chunks. But this temporary fix could result in another wave of foreclosures if additional assistance isn’t provided.

Many homeowners could be asked to pay back all of those missed mortgage bills in one lump sum at the end of the forbearance period, a near impossible feat for many who can’t afford their payments today and don’t know when the economy will recover.

Fannie Mae, Freddie Mac, and the Federal Housing Administration say their borrowers, who make up slightly more than half of all buyers, are never required to make lump-sum payments. They also offer various assistance plans, some more generous than others.

But even those homeowners will also eventually have to make good on what they owe, a hardship for those out of work. Those who can’t could eventually lose their homes.

“We are concerned about what’s going on right now, with many people going into these forbearance plans without a clear sense of what will happen at the end,” says Joseph Sant, deputy general counsel for the Center for New York City Neighborhoods. The nonprofit organization promotes and protects affordable homeownership.

“If we don’t see further action from Congress to fill this hole … we could see another foreclosure crisis when these forbearances end,” warns Sant.

Dahl’s uncertainty over what would happen at the end of his forbearance period prompted him to tap his savings and his wife’s ongoing salary as a dental assistant to make his $1,700 mortgage payment for their Rolling Meadows, IL, home. But the family can’t afford to do this indefinitely if he can’t get back to work. He’s already lost out on thousands of dollars of annual revenue, as many of the bigger art shows have been cancelled.

“I don’t like to leave things to chance, and I don’t want to lose my house because of something that is out of my control,” says Dahl. “Mortgage companies should be a lot more flexible. If they show flexibility, we will not have a repeat of ’08.”

The foreclosure crisis was in the rearview—until the coronavirus

Before the pandemic, the foreclosure crisis that followed the housing bust and lingered after the Great Recession had seemed firmly in the rearview.

In January, just 0.4% of mortgages were in some stage of foreclosure, according to the most recent data released by real estate data company CoreLogic. Meanwhile, only 3.5% of mortgages were delinquent, which means they were at least 30 days late.

But there are troubling signs those numbers could rise. About 3.74% of all mortgages were in forbearance in the week ending April 5, according to the Mortgage Bankers Association, a national trade group. That’s compared with just 0.25% of loans in forbearance in the week ending March 2.

The association expects the number of homeowners requesting forbearance to steadily increase.

About 15 million homeowners could rely on forbearance to get them through this crisis, or nearly a third of all single-family mortgages, predicts Mark Zandi, chief economist at Moody’s Analytics.

That could result in roughly 2 million foreclosures, says Zandi. To put that into perspective, there were around 7 million foreclosures as a result of the last housing bust.

“I don’t think a lump sum works, at least for most homeowners,” says Zandi. If there isn’t additional assistance offered, “there will be a lot of credit problems down the road, delinquencies, defaults, and foreclosures.”

Housing advocates are urging different kinds of assistance

Sant, with the Center for New York City Neighborhoods, is worried about the lack of uniformity among mortgage assistance programs, particularly between government-backed loans and non-government-backed loans. So available help can vary even though many mortgage companies and servicers follow the steps that Fannie and Freddie take.

Instead of forbearance, Sant would like to see the creation of a program to keep mortgage payments affordable, similar to the one the federal government created after the housing bust of more than a decade ago. It helped to save more than a million homes from the clutches of foreclosures and short sales. The program granted things like loan modifications, which could lower monthly payments, and deferments, which tacked missed payments onto the ends of loans, thereby extending their duration. These actions helped homeowners remain in their properties.

Many of the government-backed loans offer similar options.

(However, the federal government’s Home Affordable Modification Program was widely criticized for not helping nearly enough homeowners. And about a third of the borrowers who participated in the program wound up falling behind on their mortgage payments again.)

“There tends to be this initial, naive hope [from government officials] that, let’s put the situation off, let’s pause for a few months and hopefully at the end of it, people will recover and they won’t need deeper relief,” says Sant. “But we need to be planning now to provide meaningful relief.”

Many homeowners seeking mortgage assistance are wary of forbearance

Since the crisis began, Seattle-area business owner and author Debrena Jackson Gandy‘s income has dropped by about 30%. Her husband, an Uber driver, has seen his take-home pay fall by about 40%. And the couple were worried about paying both the first and second mortgages on their four-bedroom home in the Seattle suburb of Des Moines, WA.

So in late March, Jackson Gandy, 53, called her mortgage companies. The first one, where she has her primary mortgage, agreed to defer her April payment and add an extra payment onto the end of her loan. But her experience with Bank of America, where she has her smaller, second mortgage, didn’t go as smoothly.

The representative she spoke with offered her three months of forbearance instead. She could apply for a loan modification at the end of that period. There was no guarantee it would be granted.

“It was really shocking,” says Jackson Gandy. She runs Masterminds, a personal and organizational development company that hosts events, some of which have been moved online while others have been cancelled.

“If one month is a challenge, then how can I pay four months at once?” she asks.

She was a week late in making her April mortgage payment to Bank of America, because she had to wait for her husband’s earnings to come in.

(Bank of America offers deferments on its own loans, but it provides only forbearance, not deferments, on the government-backed loans it services. Chase is also a mortgage servicer for government-backed loans. Jackson Gandy isn’t sure if she has a federal-backed mortgage.)

“If you can make the payment, make the payment now,” says Rocke Andrews, a mortgage broker at Lending Arizona in Tucson. He’s also the president of the National Association of Mortgage Brokers, a trade group.

“Don’t take [forbearance] if you don’t absolutely need it. It all becomes due, and who knows what happens between now and then,” he advises.

Got Real Estate Questions? The Caton Team is here to help.

We strive to be more than just Realtors – we are also your home resource. If you have any real estate questions, concerns, need a referral or some guidance – we are here for you. Contact us at your convenience – we are but a call, text or click away!

The Caton Team believes, in order to be successful in the San Fransisco | Peninsula | Bay Area | Silicon Valley Real Estate Market we have to think and act differently. We do this by positioning our clients in the strongest light, representing them with the utmost integrity, while strategically maneuvering through negotiations and contracts. Together we make dreams come true. How can The Caton Team help you?

A mother and daughter-in-law team with over 35 years of combined, local Real Estate experience and knowledge – would’t you like The Caton Team to represent you? Let us know how we can be of service. Contact us any time.

Call | Text | Sabrina 650.799.4333 | Susan 650.796.0654

{kind=link}

{kind=link}

You must be logged in to post a comment.