For many young or first-time homebuyers, purchasing a home can feel intimidating. A recent survey shows some homebuyers ages 25 to 40 may be unsure about the homebuying process and what they can afford. It found:

“1 in 4 underestimated their buying potential by $150k or more”

“1 in 4 underestimated the increase in value by $100k or more”

“47% don’t know what a good interest rate is”

Because they feel uncertain, many young homebuyers have given up on their search, or worse, they’ve decided homebuying isn’t for them and never started on their journey to begin with.

If you’re interested in buying but aren’t sure where to begin, here are three key concepts about homeownership you should understand before you get started.

1. What You Need To Know About Down Payments

Saving for a down payment is sometimes viewed as one of the biggest obstacles for homebuyers, but that doesn’t have to be the case. As Freddie Macsays:

“The most damaging down payment myth—since it stops the homebuying process before it can start—is the belief that 20% is necessary.”

According to the most recent Home Buyers and Sellers Generational Trends Report from the National Association of Realtors (NAR), the median down payment for homes purchased between July 2019 and June 2020 was only 12%. That number is even lower when we control for age – for buyersin the 22 to 30 age range, the median down payment was only 6%.

2. You May Be Able To Afford More Home Than You Think

Working remotely, exercising, and generally spending more time than ever in our homes has changed what many people are looking for in their living space. However, some young homebuyers don’t feel they can afford a home that suits their growing needs and have decided to continue renting instead. That means they’ll miss out on some of the long-term benefits of owning a home. As an article recently published by NAR points out:

“Many young adults are underestimating how much they need for homeownership, the survey finds. Millennials underestimated how much home they can afford right now, how much interest they would pay over a 30-year mortgage, and how much home values appreciate, on average, over 10 years…”

Knowing how much home you can afford when starting the buying process is critical and could be the game-changer that gets you from renting to buying.

3. Homeownership Will Become Less Affordable the Longer You Wait

Finally, with mortgage rates starting to rise along with home prices appreciating, putting off buying a home now could cost you much more later. Sam Khater, Chief Economist at Freddie Mac,notes:

“As the economy progresses and inflation remains elevated, we expect that rates will continually rise in the second half of the year.”

Most experts forecast interest rates will rise in the months ahead, and even the smallest increase can influence your buying power. If you’ve been on the fence about buying a home, there’s no time like the present.

Bottom Line

If you feel overwhelmed by the prospect of starting your home search, you’re not alone. Let’s connect today so we can talk more about the process, what you’ll need to start your search, and what to expect.

The Caton Team knows what it takes to close a successful escrow for our selling clients – that’s why when we represent buyers – we outshine the rest. Read our TESTIMONIALS to learn more about why our clients love us and our unique approach to buying Real Estate in Silicon Valley.

Got Questions? The Caton Team is here to help.

Call| Text | Sabrina 650.799.4333 |EMAIL | WEB| BLOG

We love what we do and would love to help you navigate your sale or purchase of Residential Real Estate. Please reach out for a personal consultation. Please enjoy our free resources below and get to know our team from our TESTIMONIALS.

Got Real Estate Questions? The Caton Team is here to help.

We strive to be more than just Realtors – we are also your home resource. If you have any real estate questions, concerns, need a referral, or some guidance – we are here for you. Contact us at your convenience – we are but a call, text or click away!

The Caton Team believes, in order to be successful in the San Fransisco | Peninsula | Bay Area | Silicon Valley Real Estate Market we have to think and act differently. We do this by positioning our clients in the strongest light, representing them with the utmost integrity, while strategically maneuvering through negotiations and contracts. Together we make dreams come true.

A mother and daughter-in-law team with over 35 years of combined, local Real Estate experience and knowledge – wouldn’t you like The Caton Team to represent you? Let us know how we can be of service. Contact us any time.

Call| Text | Sabrina 650.799.4333 | Susan 650.796.0654 |EMAIL | WEB| BLOG

The Caton Team – Susan & Sabrina A Family of Realtors Effective. Efficient. Responsive. What can we do for you?

In today’s sellers’ market, standing out as a buyer is critical. Multi-offer scenarios and bidding wars are the norm due to the low supply of houses for sale and high buyer demand. If you’re buying this fall, you’ll want every advantage, especially when you’ve found the home of your dreams.

Below are five things to keep in mind when it’s time to make an offer.

1. Know Your Budget

Knowing your budget and what you can afford is critical to your success as a homebuyer. The best way to understand your numbers is to work with a lender so you can get pre-approved for a loan. As Freddie Macputs it:

“This pre-approval allows you to look for a home with greater confidence and demonstrates to the seller that you are a serious buyer.”

Showing sellers you’re serious can give you a competitive edge. It enables you to act quickly when you’ve found your perfect home.

2. Be Prepared To Move Fast

Speed and the pace of sales are contributing factors to today’s competitive housing market. According to the latest Existing Home Sales Report from the National Association of Realtors (NAR), the average home is on the market for just 17 days. As the report notes:

“Eighty-nine percent of homes sold in July 2021 were on the market for less than a month.”

When homes are selling fast, staying on top of the market and moving quickly are key. After you’ve worked with your agent to find the home that suits your needs, they’ll help you put together and submit your best offer as soon as possible.

3. A Real Estate Professional Can Lead You to Victory

No matter what the housing market looks like, rely on a trusted real estate advisor. As Freddie Macsays:

“The success of your homebuying journey largely depends on the company you keep. . . . be sure to select experienced, trusted professionals who will help you make informed decisions and avoid any pitfalls.”

Agents are experts in the local real estate market. They have insight into what’s worked for other buyers in your area and what sellers may be looking for in an offer. It may seem simple, but catering to what a seller may need can help your offer stand out.

4. Craft a Strong, Fair Offer

In the past, offering at or near the asking price was enough to make your offer appealing to sellers. In today’s market, that’s often not the case. According to the latest Realtors Confidence Index from NAR, 50% of offers are above the list price.

In such a competitive market, emotions and prices can run high. Having an agent to help craft a strong, fair offer is critical in these situations. Your agent can help you understand:

The market value of the home

Recent sales trends in the area

Current buyer demand

5. Understand the Seller’s Needs, but Resist Waiving Certain Contingencies

When crafting an offer, you’ll want to keep both your best interest and the interest of the seller in mind. Your trusted real estate advisor will help you consider which levers you could pull, including contract contingencies (conditions you set that the seller must meet for the purchase to be finalized). Of course, there are certain contingencies you don’t want to give up, like the home inspection.

“Resist the temptation to waive the inspection contingency, especially in a hot market or if the home is being sold ‘as-is’, which means the seller won’t pay for repairs. Without an inspection contingency, you could be stuck with a contract on a house you can’t afford to fix.”

Bottom Line

Today’s competitive housing market makes it more important than ever to make a strong offer on a home. Let’s connect to make sure your offer rises to the top.

The Caton Team knows what it takes to close a successful escrow for our selling clients – that’s why when we represent buyers – we outshine the rest. Read our TESTIMONIALS to learn more about why our clients love us and our unique approach to buyer Real Estate in Silicon Valley.

Got Questions? The Caton Team is here to help.

Call| Text | Sabrina 650.799.4333 |EMAIL | WEB| BLOG

We love what we do and would love to help you navigate your sale or purchase of Residential Real Estate. Please reach out for a personal consultation. Please enjoy our free resources below and get to know our team from our TESTIMONIALS.

Got Real Estate Questions? The Caton Team is here to help.

We strive to be more than just Realtors – we are also your home resource. If you have any real estate questions, concerns, need a referral, or some guidance – we are here for you. Contact us at your convenience – we are but a call, text or click away!

The Caton Team believes, in order to be successful in the San Fransisco | Peninsula | Bay Area | Silicon Valley Real Estate Market we have to think and act differently. We do this by positioning our clients in the strongest light, representing them with the utmost integrity, while strategically maneuvering through negotiations and contracts. Together we make dreams come true.

A mother and daughter-in-law team with over 35 years of combined, local Real Estate experience and knowledge – wouldn’t you like The Caton Team to represent you? Let us know how we can be of service. Contact us any time.

Call| Text | Sabrina 650.799.4333 | Susan 650.796.0654 |EMAIL | WEB| BLOG

The Caton Team – Susan & Sabrina A Family of Realtors Effective. Efficient. Responsive. What can we do for you?

It’s worth considering the many benefits of homeownership before you make the decision to rent or buy a home.

When you buy, you can stabilize your housing costs, own a tangible asset, and grow your net worth as you gain equity. When you rent, you face rising housing costs, won’t see a return on your investment, and limit your ability to save.

If you want to learn more about the benefits of homeownership, let’s connect today.

Each client is unique – please reach out for a personal consultation or read our blog HERE

Got Questions? The Caton Team is here to help.

Call| Text | Sabrina 650.799.4333 |EMAIL | WEB| BLOG

We love what we do and would love to help you navigate your sale or purchase of Residential Real Estate. Please reach out for a personal consultation. Please enjoy our free resources below and get to know our team from our TESTIMONIALS.

Got Real Estate Questions? The Caton Team is here to help.

We strive to be more than just Realtors – we are also your home resource. If you have any real estate questions, concerns, need a referral, or some guidance – we are here for you. Contact us at your convenience – we are but a call, text or click away!

The Caton Team believes, in order to be successful in the San Fransisco | Peninsula | Bay Area | Silicon Valley Real Estate Market we have to think and act differently. We do this by positioning our clients in the strongest light, representing them with the utmost integrity, while strategically maneuvering through negotiations and contracts. Together we make dreams come true.

A mother and daughter-in-law team with over 35 years of combined, local Real Estate experience and knowledge – wouldn’t you like The Caton Team to represent you? Let us know how we can be of service. Contact us any time.

Call| Text | Sabrina 650.799.4333 | Susan 650.796.0654 |EMAIL | WEB| BLOG

The Caton Team – Susan & Sabrina A Family of Realtors Effective. Efficient. Responsive. What can we do for you?

How does The Caton Team set our buying clients apart from the crowd?

That’s a great question and the answer is easy – with strategy, professionalism, kindness, and the ability to maneuver through contracts and negotiations with ease and grace.

Our market can move very fast. Pending sales information is imperative to understand the temperature of the market. Though Appraisers will only use Closed Sales (aka Sold), that information is already 30 days old, while pending sales help a buyer act accordingly in the current market.

We provide data on the area at the start of our journey once our clients provide a pre-approval letter with their confirmed price range. With that price range and the towns and types of homes desired, we see where our budget lands, contact pending sales to take the temperature of the market, and then act accordingly. It may mean adjusting areas, size, yard, and amenities. Or it may mean writing an offer. Negotiating the offer and standing out from the crowd is what The Caton Team does best. We’ll review with our buying clients privately how best to achieve a winning offer as each home, client and situation is unique.

It is a journey. We are data-driven, and this enables our buyers to hunt in areas where they have a chance to compete it. If we see sales are 5% over list price and that figure lands within a client’s budget, we know it is time to act. If the figure lands outside, we know it is time to expand and adjust the search. It is an ongoing process with many turning gears and we love it. With over 40 years of combined, local Real Estate experience, we’re here to work with you towards your goal.

When our clients make time for the biggest purchase of their life, we help them succeed quickly. Seeing homes and reviewing disclosures during the week sets our buyers apart from the mainstream. Granting them time to do all it takes to confidently write a winning offer. We’re proud to say several sellers have left money on the table to take our clients’ offers over the highest offer. Our work ethic shows. The Caton Team believes, in order to be successful in the Silicon Valley Real Estate Market we need to act and think differently. So we do and our success rate reflects that.

How can The Caton Team Help You? Let us know how. Call or text 650.799.4333. Thank you! Susan & Sabrina – The Caton Team

Got Questions? The Caton Team is here to help.

Call| Text | Sabrina 650.799.4333 |EMAIL | WEB| BLOG

We love what we do and would love to help you navigate your sale or purchase of Residential Real Estate. Please reach out for a personal consultation. Please enjoy our free resources below and get to know our team TESTIMONIALS.

Got Real Estate Questions? The Caton Team is here to help.

We strive to be more than just Realtors – we are also your home resource. If you have any real estate questions, concerns, need a referral, or some guidance – we are here for you. Contact us at your convenience – we are but a call, text or click away!

The Caton Team believes, in order to be successful in the San Fransisco | Peninsula | Bay Area | Silicon Valley Real Estate Market we have to think and act differently. We do this by positioning our clients in the strongest light, representing them with the utmost integrity, while strategically maneuvering through negotiations and contracts. Together we make dreams come true.

A mother and daughter-in-law team with over 40 years of combined, local Real Estate experience and knowledge – wouldn’t you like The Caton Team to represent you? Let us know how we can be of service. Contact us any time.

Call| Text | Sabrina 650.799.4333 | Susan 650.796.0654 | EMAIL | WEB| BLOG

The Caton Team – Susan & Sabrina A Family of Realtors Effective. Efficient. Responsive. What can we do for you?

The historically low inventory over the past few years led to challenges for many buyers trying to find a home that met their needs and their budget. If you’re in the same boat, you should know the recent shift in the housing market may have opened up doors for you to restart your search.

The inventory of homes for sale has increased this year, and that’s giving buyers much needed options. As Danielle Hale, Chief Economist at realtor.com, says:

“. . . today’s shoppers have more than 5 homes to consider for every 4 they had at this time a year ago.”

But perspective is important. Overall, housing supply is still low. If you need even more choices, expanding your search by adding additional housing types, like condominiums, could help.

Exploring Condos Could Add Options That Fit Your Budget

One thing to consider is condos generally differ from single-family homes in average space and floorplans. But that size difference is one reason why condos can be a more affordable option. According to a recent report from realtor.com, condo buyers paid roughly 7% less for their home than buyers of other housing types last year. With rising mortgage rates and home prices, the relative affordability of a condo could be worth considering.

Remember, your first home doesn’t have to be your forever home. The important thing is to get your foot in the door as a homeowner. Buying a condo now can springboard you into a bigger home later on. An article from the Urban Institute explains:

“Because condos and co-ops are generally more affordable, they tend to help first-time homebuyers step onto the first rung of the homeownership ladder. These buyers often use the equity on their condo to then purchase a larger single-family home.”

In other words, owning a condo will help you start building wealth in the form of home equity. In time, the equity you build can fuel a future purchase should you decide you want to buy a home with more space or different amenities.

Condo Living Provides Several Great Perks

Boosting the number of options in your budget during your home search is just one reason to consider condos, but there are several other benefits to condo living.

First, they tend to require minimal upkeep and lower maintenance – and that can give you more time to spend doing the things you enjoy. A recent article from Bankrate highlights this, saying:

“Condos can be a good option for anyone who wants to keep home maintenance to a minimum . . . if the roof is leaking or the carpet in the lobby needs to be replaced, that’s not your responsibility — the condo association handles those duties.”

Plus, since many condos are located in or near city centers, they offer the added benefit of being in close proximity to work and leisure. Again, realtor.comexplains:

“Buying a condo, which is generally less expensive than a single-family home, enables a household to afford to own in the middle of it all, and often means a newer-built home with less maintenance responsibility.”

Ultimately, owning and living in a condo can be a lifestyle choice. And if that appeals to you, they could give you the added options you need to buy your first home.

Bottom Line

Adding condominiums to your housing search could be a great move. If you’re ready to search condos in your area, connect with a local real estate professional today.

Each client is unique – please reach out for a personal consultation or read our blog HERE

Got Questions? The Caton Team is here to help.

Call| Text | Sabrina 650.799.4333 |EMAIL | WEB| BLOG

We love what we do and would love to help you navigate your sale or purchase of Residential Real Estate. Please reach out for a personal consultation. Please enjoy our free resources below and get to know our team from our TESTIMONIALS.

Got Real Estate Questions? The Caton Team is here to help.

We strive to be more than just Realtors – we are also your home resource. If you have any real estate questions, concerns, need a referral, or some guidance – we are here for you. Contact us at your convenience – we are but a call, text or click away!

The Caton Team believes, in order to be successful in the San Fransisco | Peninsula | Bay Area | Silicon Valley Real Estate Market we have to think and act differently. We do this by positioning our clients in the strongest light, representing them with the utmost integrity, while strategically maneuvering through negotiations and contracts. Together we make dreams come true.

A mother and daughter-in-law team with over 35 years of combined, local Real Estate experience and knowledge – wouldn’t you like The Caton Team to represent you? Let us know how we can be of service. Contact us any time.

Call| Text | Sabrina 650.799.4333 | Susan 650.796.0654 |EMAIL | WEB| BLOG

The Caton Team – Susan & Sabrina A Family of Realtors Effective. Efficient. Responsive. What can we do for you?

SOLD by The Caton Team! We are so grateful to earn our client’s trust. The journey our clients takes is unique to them. With over forty years of combined Real Estate experience, The Caton Team can help our clients in any market area. With data, know-how, experience, solid ethics, and business practices – we set our clients apart and help them achieve their Real Estate goals.

We love helping our clients achieve their Real Estate goals – how can The Caton Team help you? Let us know @ info@TheCatonTeam.com | 650.799.4333

How can The Caton Team help You?

We truly enjoy helping our clients sell their home. The Caton Team loves what we do and would love to help you – please enjoy our resources below. Get to know us at through our clients words.

The Caton Team does not receive any compensation for our Real Eats posts, we use YELP for ease of use. All restaurant reviews are unsolicited and unpaid. Photos of dishes and edits are my own. Information deemed reliable but not guaranteed. Third-party information not verified.

How can The Caton Team help You?

Call| Text | Sabrina 650.799.4333 | Susan 650.796.0654 |EMAIL | WEB| BLOG

Get exclusive inside access when you follow uson Facebook & Instagram

Got Real Estate Questions? The Caton Team is here to help.

We strive to be more than just Realtors – we are also your home resource. If you have any real estate questions, concerns, need a referral, or some guidance – we are here for you. Contact us at your convenience – we are but a call, text or click away!

The Caton Team believes, in order to be successful in the San Fransisco | Peninsula | Bay Area | Silicon Valley Real Estate Market we have to think and act differently. We do this by positioning our clients in the strongest light, representing them with the utmost integrity, while strategically maneuvering through negotiations and contracts. Together we make dreams come true. How can The Caton Team help you?

A mother and daughter-in-law team with over 35 years of combined, local Real Estate experience and knowledge – wouldn’t you like The Caton Team to represent you? Let us know how we can be of service. Contact us any time.

Call | Text | Sabrina 650.799.4333 | Susan 650.796.0654 |EMAIL | WEB| BLOG

The Caton Team – Susan & Sabrina A Family of Realtors Effective. Efficient. Responsive. What can we do for you?

Here is an excerpt from the excellent website, Mortgage New Daily:

Before you stop paying your bills in the hope of cashing in, let’s separate fact from fiction. First and most importantly, you will absolutely NOT get a better deal on a mortgage rate if your credit score is lower, even if your nephew just texted you a screenshot of a news headline saying “620 FICO SCORE GETS A 1.75% FEE DISCOUNT” and “740 FICO SCORE PAYS 1% FEE.” MATTHEW GRAHAM – MORTGAGE NEWS DAILY

I strongly encourage you to read the rest of his article here: https://www.mortgagenewsdaily.com/markets/mortgage-rates-04212023 It is well-written and informative and takes the political bias and opinion out of the explanation. Just the facts. And yes, it has gotten more expensive to get a home loan–for everyone.

But to really understand what’s changed, you need to first understand that mortgage rates have a price. In other words, each rate on a rate sheet is associated with a price or fee and that price/fee goes up and and down with the rate you choose, based on how much money you want to borrower, what your credit score is and how much down payment you’re bringing to the purchase. There are a few other factors that determine rate and that is why it is so difficult to answer your question: “What are rates like today?”

With that out of the way, sometimes an interest rate comes at cost to you (that’s what we all know as “Points”) and sometimes that price/fee is a rebate to you (that’s how some lenders will quote you a “no cost loan”). What’s in the middle is something called “PAR”. This is the fancy Wall Street word for “Neutral”, meaning you don’t pay points and you don’t get a rebate. The price for mortgage rates has been increased at the direction of the Federal Housing Finance Administration because they don’t believe they are making enough money and raising these fees (because inflation). The FHFA believes this will help them maintain the financial health of Fannie Mae and Freddie Mac–the two Government Sponsored Entities that purchase many of the home loans that are originated in the United States.

Here’s a picture proving that home loans for the purpose of purchasing just got more expensive for us all:

Now, Fannie and Freddie have what is called a “Duty to Serve” and that requires them to be focused on helping first time home buyers get into homes. That is why the chart above shows that a smaller down payment and a lower credit scores appears to be getting a better deal than say someone with higher credit and a larger down payment.

But let’s take the following example, if you have two borrowers, one with a 700 FICO and 20% down, and another with 640 and 5% down, the LLPAs (1.500%) are in fact the same, creating an “equal” playing field. However, if you have both come in with 5% the higher FICO score gets an improvement to LLPA of 0.625%, whereas if the lower FICO borrower comes in with 20%, their LLPA is 1.375% higher. With the latter, a mortgage of $600,000 results in $8,250 of additional costs to the lower credit score borrower. The point here is that the FHFA is working to create more affordable housing for those that have lower credit scores and by assumption a smaller down payment.

After Weeks of Decline, Mortgage Rates Increase

For the first time in over a month, mortgage rates moved up due to shifting market expectations. Home prices have stabilized somewhat, but with supply tight and rates stuck above six percent, affordable housing continues to be a serious issue for potential homebuyers. Unless rates drop into the mid five percent range, demand will only modestly recover.

The latest data showed signs of strength in the housing market while the labor sector is getting weaker. Plus, an important recession signal continues to reflect a slowing economy. Don’t miss these stories:

What the Media Gets Wrong About Home Prices

Home Builders Need to be “Starting” Something

NAHB Reports Cautious Optimism Among Home Builders

Job Market Getting Weaker

Recession Signal Flashing

What the Media Gets Wrong About Home Prices

Existing Home Sales fell 2.4% from February to March to a 4.44 million unit annualized pace, per the National Association of Realtors (NAR), which was in line with estimates. Sales were 22% lower than they were in March of last year. This report measures closings on existing homes, which represent around 90% of the market, making it a critical gauge for taking the pulse of the housing sector.

What’s the bottom line? While it’s true that buyer activity slowed in March, February was an especially strong month for closings, so a slight pullback last month was understandable.

In addition, multiple data points suggest that demand remains strong. Homes stayed on the market on average for 29 days, down sharply from 34 days in February. Plus, 65% of homes sold in March were on the market for less than a month, which is up from 57% and shows homes are selling quickly when they’re priced correctly. Meanwhile, investors accounted for 17% of transactions last month, making up roughly one out of every six deals. Clearly investors are seeing the opportunity in housing right now.

Also of note, there was a 0.9% decline in the median home price to $375,700 from a year earlier. However, this is not the same as a decline in home prices as some media reports implied.

The median home price simply means half the homes sold were above that price and half were below it, and this figure can be skewed by the mix of sales among lower-priced and higher-priced homes. In fact, we could see home prices increase across all price categories, but the median price could still fall if the concentration of sales was on the lower end. Actual appreciation numbers are higher, not lower, on a year-over-year basis according to key reports from Case-Shiller, CoreLogic and the Federal Housing Finance Agency.

Home Builders Need to be “Starting” Something

Construction of new homes slowed in March, with Housing Starts falling nearly 1% from February. Building Permits, which are indicative of future supply, also fell 8.8% for the month. While Starts and Permits for single-family homes both ticked higher from February to March, they were significantly lower than in March of last year.

What’s the bottom line? The housing sector is undersupplied, and not enough inventory is heading to the market. Starts for single-family homes have been on a downward trend over the last year, with the pace of 1.191 million units in March 2022 falling all the way to 861,000 units this March. Single-family permits have followed the same pattern, declining from a pace of 1.163 million units to 818,000 over the same period.

With single-family homes remaining in high demand among buyers, the imbalance between supply and demand should continue to be supportive of prices.

NAHB Reports Cautious Optimism Among Home Builders

The National Association of Home Builders (NAHB) Housing Market Index, which is a near real-time read on builder confidence, rose one point to 45 in April, marking the fourth straight month this measure has increased. Among the components of the index, current sales conditions rose two points to 51 while sales expectations for the next six months increased three points to 50. Buyer traffic remained unchanged at 31.

What’s the bottom line? Home builder confidence has now risen 14 points since the low of 31 in December. Present sales conditions returned to expansion territory (over 50) for the first time since last September, while the future sales outlook is right at the breakeven between expansion and contraction at its highest level since June. Even though the overall confidence reading remains below 50 in contraction territory, sentiment continues to rebound in the right direction.

Job Market Getting Weaker

Initial Jobless Claims continued to move higher this month, with the number of people filing for unemployment benefits for the first time rising by 5,000 in the latest week to 245,000. This tied the third highest reading so far this year. Continuing Jobless Claims also surged to 1.865 million, up 61,000.

What’s the bottom line? Continuing Claims measure people who continue to receive benefits after their initial claim is filed and this data clearly shows that hiring has slowed. While the number can be volatile from week to week, the overall trend has been higher with an increase of around 576,000 since the low reached last September.

Plus, there’s greater evidence of workforce reductions as the four-week average of Initial Jobless Claims, which smooths out some of the weekly fluctuation among first-time filers, has hovered around 240,000 at a yearly high in recent weeks.

Recession Signal Flashing

The Conference Board released their Leading Economic Index (LEI) for March, which was down 1.2%, falling to “its lowest level since November of 2020, consistent with worsening economic conditions ahead,” said Justyna Zabinska-La Monica, Senior Manager, Business Cycle Indicators. This report is a composite of economic indexes and can signal peaks and troughs in the business cycle.

What’s the bottom line? The Conference Board explained that a warning signal occurs when the LEI 6-month growth rate on an annualized basis breaks beneath 0%. But a break beneath -4.2%, like we saw last month, is a recession signal that has been highly accurate historically. The Conference Board also stated that they believe the U.S. will enter a recession “starting in mid-2023.”

What to Look for This Week

More housing news is ahead, starting with Tuesday’s release of home price appreciation data for February from the Case-Shiller Home Price Index and the Federal Housing Finance Agency (FHFA) House Price Index. March’s New Home Sales will also be reported on Tuesday, while Pending Home Sales follows on Thursday.

Also on Thursday, the latest Jobless Claims data will be released along with the first reading for first quarter 2023 GDP. Friday brings perhaps the biggest news of the week with March’s reading for the Fed’s favored inflation measure, Personal Consumption Expenditures.

Technical Picture

Mortgage Bonds were able to stay above their 50-day Moving Average after testing it earlier in the day last Friday. The 10-year tested support at its 200-day Moving Average but remained above it at the end of last week.

Shared From Lender Chris Carr NMLS# 1466899 – SOURCE

If you are considering a sale or purchase of Real Estate – The Caton Team would love to interview for the job as your Realtor. We love what we do, let us take care of you.

We believe to be successful in the Silicon Valley Real Estate Market we have to think and act differently. We do this by positioning our clients in the strongest light, representing them with integrity, while strategically maneuvering through negotiations and contracts.

A mother and daughter-in-law team with 40 years of combined, local real estate experience, knowledge, and know-how – wouldn’t you like The Caton Team to represent you? Let us know how we can be of service. Contact us any time. Call | Text | 650.799.4333 | Email | Info@TheCatonTeam.com

Effective. Efficient. Responsive. Got Questions? The Caton Team is here to help.

Call| Text | Sabrina 650.799.4333 |EMAIL | WEB| BLOG

We love what we do and would love to help you navigate your sale or purchase of Residential Real Estate. Please reach out for a personal consultation. Please enjoy our free resources below and get to know our team from our TESTIMONIALS.

Got Real Estate Questions? The Caton Team is here to help.

We strive to be more than just Realtors – we are also your home resource. If you have any real estate questions, concerns, need a referral, or some guidance – we are here for you. Contact us at your convenience – we are but a call, text or click away!

The Caton Team believes, in order to be successful in the San Fransisco | Peninsula | Bay Area | Silicon Valley Real Estate Market we have to think and act differently. We do this by positioning our clients in the strongest light, representing them with the utmost integrity, while strategically maneuvering through negotiations and contracts. Together we make dreams come true.

A mother and daughter-in-law team with over 35 years of combined, local Real Estate experience and knowledge – wouldn’t you like The Caton Team to represent you? Let us know how we can be of service. Contact us any time.

Call| Text | Sabrina 650.799.4333 | Susan 650.796.0654 |EMAIL | WEB| BLOG

The Caton Team – Susan & Sabrina A Family of Realtors Effective. Efficient. Responsive. What can we do for you?

One of the first steps in your home buying journey is getting pre-approved. To understand why it’s such an important step, you need to understand what pre-approval is and what it does for you. Business Insider explains:

“In a preapproval [sic], the lender tells you which types of loans you may be eligible to take out, how much you may be approved to borrow, and what your rate could be.”

Basically, pre-approval gives you critical information about the home buying process that’ll help you understand your options and what you may be able to borrow.

How does it work? As part of the pre-approval process, a lender will look at your finances to determine what they’d be willing to loan you. From there, your lender will give you a pre-approval letter to help you understand how much money you can borrow. That can make it easier when you set out to search for homes because you’ll know your overall numbers. And with higher mortgage rates impacting affordability for many buyers today, a solid understanding of your numbers is even more important.

Pre-Approval Helps Show You’re a Serious Buyer

Another added benefit is pre-approval can help a seller feel more confident in your offer because it shows you’re serious about buying their house. A recent article from Forbesnotes:

“From the seller’s perspective, a preapproval [sic] letter from a reputable local lender often can make the difference between accepting and rejecting an offer.”

This goes to show, even though you may not face the intense bidding wars you saw if you tried to buy during the pandemic, pre-approval is still an important part of making a strong offer. In fact, Christy Bieber, Personal Finance Writer at The Motley Foolexplains it may be the most important part of making an offer:

“Pre-approval maximizes the chances you’ll be able to actually close the deal – and sellers want to see that.

The fact that a pre-approval gives you a better chance of getting your offer accepted is undoubtedly the most important reason to complete this step . . .”

Bottom Line

Getting pre-approved is an important first step towards buying a home. It lets you know what you can borrow and shows sellers you’re serious about purchasing their home. Connect with a local real estate professional and a trusted lender so you have the tools you need to purchase a home in today’s market.

The Caton Team knows what it takes to turn our buyers into homeowners. Let us guide you home.

Call| Text | Sabrina 650.799.4333 |EMAIL | WEB| BLOG

We love what we do and would love to help you navigate your sale or purchase of Residential Real Estate. Please reach out for a personal consultation. Please enjoy our free resources below and get to know our team from our TESTIMONIALS.

Got Real Estate Questions? The Caton Team is here to help.

We strive to be more than just Realtors – we are also your home resource. If you have any real estate questions, concerns, need a referral, or some guidance – we are here for you. Contact us at your convenience – we are but a call, text or click away!

The Caton Team believes, in order to be successful in the San Fransisco | Peninsula | Bay Area | Silicon Valley Real Estate Market we have to think and act differently. We do this by positioning our clients in the strongest light, representing them with the utmost integrity, while strategically maneuvering through negotiations and contracts. Together we make dreams come true.

A mother and daughter-in-law team with over 35 years of combined, local Real Estate experience and knowledge – wouldn’t you like The Caton Team to represent you? Let us know how we can be of service. Contact us any time.

Call| Text | Sabrina 650.799.4333 | Susan 650.796.0654 |EMAIL | WEB| BLOG

The Caton Team – Susan & Sabrina A Family of Realtors Effective. Efficient. Responsive. What can we do for you?

The news is full of bad news – that’s why The Caton Team is here to change the narrative. Yes – rates did jump 2nd Quarter of 2022 and it rippled through the Real Estate Market. Today – late January 2023, rates have settled down a bit from their nightmarish high of around 7% – today we’re seeing 4.5-6% popping up again.

BUT… it’s still not the 3% we loved in 2021! So, if Buying Bay Area Real Estate is still a goal – when the news says the market is down – now is the time to act – so let’s talk about solutions.

Welcome Home Funding, a division of Berkshire Hathaway HomeServices, is offering two products to help wishful home buyers get into a home while the market is soft – i.e. – that short window when it’s a buyer’s market here in the Bay Area.

Welcome Home Funding is offering a RATE BUY DOWN. Take a look at the example below. Year 1 – the interest rate is nice and low, getting a buyer into a property and each year it goes up a point*.

Next up is the Welcome Home Funding – RATE REBOUND. No one knows when the market will peak or where interest rates will land but with RATE REBOUND a buyer can rest assured that if rates drop further they can take advantage of the lower rate with NO lender fees on the refinance within 5 years of their purchase AND get a $1000 credit to go towards third parties fees associated with refinancing – like the appraisal report and new credit pull. Please note this product has a promotional lifespan. Homes must be IN Contract by 6.30.2023 and Close Escrow by 9.30.23 to qualify. Please note lender fees do apply to the original purchase loan with Welcome Home Funding.

For more information – contact The Caton Team|Cell 650.799.4333|EMAIL|

Or Mike Kamienski with Welcome Home Funding |Cell (650) 484-6488 | EMAIL|

Got Questions? The Caton Team is here to help.

Call| Text | Sabrina 650.799.4333 |EMAIL | WEB| BLOG

We love what we do and would love to help you navigate your sale or purchase of Residential Real Estate. Please reach out at your convenience for a personal consultation. Please enjoy our free resources below and get to know our team through our clients’ words.Testimonials.

Got Real Estate Questions? The Caton Team is here to help.

We strive to be more than just Realtors – we are also your home resource. If you have any real estate questions, or concerns, or need a referral or some guidance – we are here for you. Contact us at your convenience – we are but a call, text, or click away!

The Caton Team believes, in order to be successful in the San Fransisco | Peninsula | Bay Area | Silicon Valley Real Estate Market we have to think and act differently. We do this by positioning our clients in the strongest light, representing them with the utmost integrity, while strategically maneuvering through negotiations and contracts. Together we make dreams come true.

A mother and daughter-in-law team with over 35 years of combined, local Real Estate experience and knowledge – wouldn’t you like The Caton Team to represent you? Let us know how we can be of service. Contact us any time.

Call| Text | Sabrina 650.799.4333 | Susan 650.796.0654 |EMAIL | WEB| BLOG

The Caton Team – Susan & Sabrina A Family of Realtors Effective. Efficient. Responsive. What can we do for you?

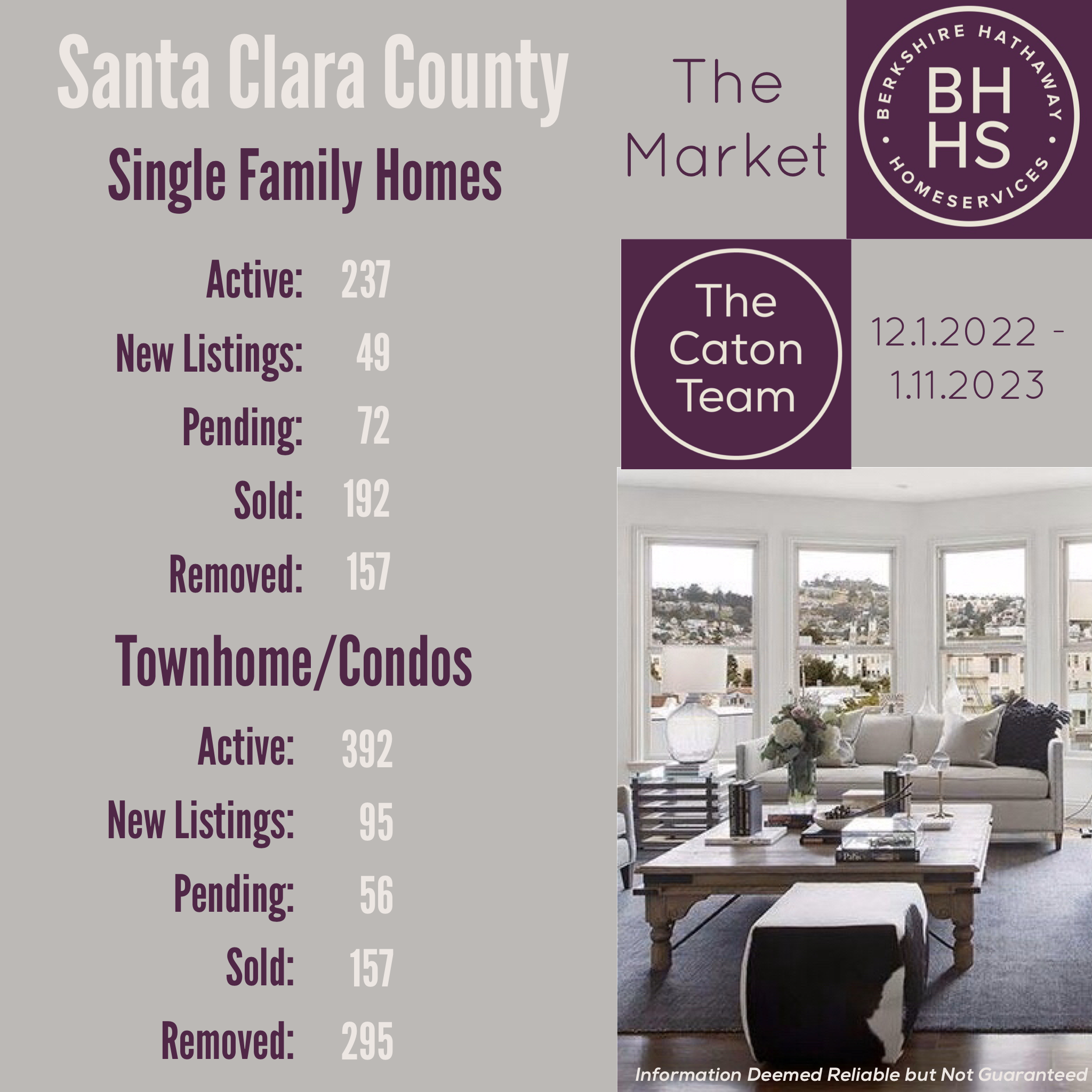

Hello Caton Team Readers. Thank you for tuning in.

Today I’m sharing a market snapshot – how many Single Family Homes and Condos are currently FOR SALE, how many are NEW on the market as of Jan 1, 2023, and how many are PENDING and SOLD as of Dec 1, 2022, in San Mateo, San Francisco and, Santa Clara Counties.

The bottom line – properties are selling. Frankly, buying during the “slow” time of the market – I.E. over the holidays and during the first part of 1st quarter – often offers a buyer LESS competition and perhaps some negotiation opportunities. Why? Homes for sale over the holidays and winter – HAVE TO SELL – and historically the winter season most buyers are in hibernation mode. Fewer buyers equal less demand and MORE opportunities for the buyers that are out there.

So, do yourself a favor; if buying Real Estate is a goal for you – let’s take a look at your budget with today’s rate. Because buying today – at today’s home prices – with temporary low demand – gives you an edge. Remember, when rates go down – a buyer can REFINANCE their loan, and grab that lower rate while earning equity as prices rise – because here in the San Francisco Bay Area – home prices have been rising since 1849 – and that’s accounting for the dips along the way.

If a buyer waits for rates to lower, demand will rise and we’re back to overbidding when inventory is low.

Key takeaways: Demand is low right now – in part due to the rise of Interest Rates from 2022 AND our seasonal market. The Caton Team has great success working with budget-conscious buyers during a slow market. Don’t wait for demand to rise when rates drop, don’t be another offer on the desk. Right now, today, many homes are NOT getting multiple offers – giving a buyer a chance to pay a fair price, without overbidding.

Each client is unique and each market is unique. The Caton Team is here to help you every step of the way – let’s chat about your options and devise a game plan to turn your dreams into reality.

Got Questions? The Caton Team is here to help.

Call| Text | Sabrina 650.799.4333 |EMAIL | WEB| BLOG

Got Questions? The Caton Team is here to help.

Call| Text | Sabrina 650.799.4333 |EMAIL | WEB| BLOG

We love what we do and would love to help you navigate your sale or purchase of Residential Real Estate. Please reach out at your convenience for a personal consultation. Please enjoy our free resources below and get to know our team through our clients’ words.Testimonials.

Got Real Estate Questions? The Caton Team is here to help.

We strive to be more than just Realtors – we are also your home resource. If you have any real estate questions, concerns, need a referral or some guidance – we are here for you. Contact us at your convenience – we are but a call, text or click away!

The Caton Team believes, in order to be successful in the San Fransisco | Peninsula | Bay Area | Silicon Valley Real Estate Market we have to think and act differently. We do this by positioning our clients in the strongest light, representing them with the utmost integrity, while strategically maneuvering through negotiations and contracts. Together we make dreams come true.

A mother and daughter-in-law team with over 35 years of combined, local Real Estate experience and knowledge – would’t you like The Caton Team to represent you? Let us know how we can be of service. Contact us any time.

Call| Text | Sabrina 650.799.4333 | Susan 650.796.0654 |EMAIL | WEB| BLOG

The Caton Team – Susan & Sabrina A Family of Realtors Effective. Efficient. Responsive. What can we do for you?

![Should I Rent or Should I Buy? [INFOGRAPHIC] | Simplifying The Market](https://files.keepingcurrentmatters.com/wp-content/uploads/2022/07/20220715-MEM.png)

{kind=link}

{kind=link}

{kind=link}

You must be logged in to post a comment.