A shout out to my friend and lender Christian Carr – NMLS #1466899 for posting this information I felt I should share here.

The Federal Housing Administration (FHA) updates its loan limits and the mechanics of its loan programs each year. For 2025, there are key changes that homebuyers—especially first-time and moderate-income borrowers—should be aware of.

FHA Loan Limits in 2025

• Single-family homes: Loan limits range from $524,225 in low-cost areas (floor limit) to $1,209,750 in high-cost counties (ceiling limit).

• Multi-unit properties:

◦ 2-unit: $671,200 – $1,548,975

◦ 3-unit: $811,275 – $1,872,225

◦ 4-unit: $1,008,300 – $2,326,875

• These limits are tied to median home prices and align with conforming loan ceilings set by the FHFA ($806,500 standard / $1,209,750 high-cost).

Why it matters: Higher limits allow FHA financing for more expensive homes without needing a jumbo mortgage.

FHA Repayment Terms & Refinancing Options

✅ Fixed Terms and Gradual Payment Options

• Standard FHA mortgages come with 15- and 30-year terms

• Graduated Payment Mortgages (GPMs) are also available, allowing payments to increase gradually (e.g., 2.5%–7.5% annually) during the first 5–10 years before leveling out en.wikipedia.org.

🔄FHA Refinance Programs (2025 Highlights)

FHA homeowners may refinance under four main options:

1 Simple Refinance – Switch from one FHA loan to another to lower rate or shorten term, requires appraisal.

2 Streamline Refinance – Less documentation, sometimes no appraisal or credit check, must show “net tangible benefit” and have made 6+ on-time payments.

3 Cash‑Out Refinance – Access up to 85% equity for any purpose; requires appraisal.

4 203(k) Rehab Refinance – Finance purchase or refinance plus home improvements; available for primary residences only.

What Buyers Should Know

• Loan limits expanded in 2025—check your county limits via the HUD lookup tool.

• Graduated Payment Mortgages can help match payments to growing incomes—especially useful for younger buyers.

• Streamline refinances are attractive for existing FHA homeowners: minimal paperwork, faster turnaround—but closing costs apply (~3–6%).

• Cash‑out and 203(k) options remain available, but careful consideration of equity use and repayment ability is essential.

Final Thoughts

If you’re shopping for a new home or refinancing in 2025, FHA’s expanded limits can open more opportunities. Whether you’re looking to lower your rate, tap into equity, or finance renovations, FHA offers versatile programs—but it’s important to choose based on your goals and ability to repay. To verify your specific county’s limit, visit the official HUD lookup tool . For details on repayment plan options, review FHA’s official policy handbook or speak to an FHA-approved lender.

Cell| Sabrina 650.799.4333 |Susan 650.796.0654 | EMAIL | WEB| BLOG

We love what we do and would love to help you navigate your sale or purchase of Residential Real Estate. Please reach out for a personal consultation. Please enjoy our free resources below and get to know our team from our TESTIMONIALS.

Effective. Efficient. Responsive. The Caton Team 🏡

Got Real Estate Questions? The Caton Team is here to help.

We strive to be more than just Realtors – we are also your home resource. If you have any real estate questions, concerns, need a referral, or some guidance – we are here for you. Contact us at your convenience – we are but a call, text, or click away!

The Caton Team believes, in order to be successful in the San Francisco | Peninsula | Bay Area | Silicon Valley Real Estate Market, we have to think and act differently. We do this by positioning our clients in the strongest light, representing them with the utmost integrity, while strategically maneuvering through negotiations and contracts. Together we make dreams come true.

A mother and daughter-in-law team with over 35 years of combined local Real Estate experience and knowledge – wouldn’t you like The Caton Team to represent you? Let us know how we can be of service. Contact us any time.

Cell | Sabrina 650.799.4333 | Susan 650.796.0654 | EMAIL | WEB| BLOG

The Caton Team – Susan & Sabrina A Family of Realtors Effective. Efficient. Responsive. What can we do for you?

Caring for our planet is important for The Caton Team. When we saw this service – we knew we had to share it with our people…

Many residents may not start to think about their options for disposing toxic waste—including paints, batteries and fertilizers—until the very last minute when they are moving. Sometimes they even ask their Realtor to take it in, which is actually illegal unless the realtor signs a special waiver.

To help Realtors avoid this issue, San Mateo County Health has provided an informational postcards that you can share with clients, which explains their toxic waste disposal options. Clients of SAMCAR Realtors who bring the postcard to their HHW drop-off event appointment will receive a Home Depot gift card that may help them with the moving process.

It is important we all do our part for our community and planet. THANK YOU!

Got Questions? The Caton Team is here to help.

Cell| Sabrina 650.799.4333 |Susan 650.796.0654 | EMAIL | WEB| BLOG

We love what we do and would love to help you navigate your sale or purchase of Residential Real Estate. Please reach out for a personal consultation. Please enjoy our free resources below and get to know our team from our TESTIMONIALS.

Effective. Efficient. Responsive. The Caton Team 🏡

Got Real Estate Questions? The Caton Team is here to help.

We strive to be more than just Realtors – we are also your home resource. If you have any real estate questions, concerns, need a referral, or some guidance – we are here for you. Contact us at your convenience – we are but a call, text, or click away!

The Caton Team believes, in order to be successful in the San Francisco | Peninsula | Bay Area | Silicon Valley Real Estate Market, we have to think and act differently. We do this by positioning our clients in the strongest light, representing them with the utmost integrity, while strategically maneuvering through negotiations and contracts. Together we make dreams come true.

A mother and daughter-in-law team with over 35 years of combined local Real Estate experience and knowledge – wouldn’t you like The Caton Team to represent you? Let us know how we can be of service. Contact us any time.

Cell | Sabrina 650.799.4333 | Susan 650.796.0654 | EMAIL | WEB| BLOG

The Caton Team – Susan & Sabrina A Family of Realtors Effective. Efficient. Responsive. What can we do for you?

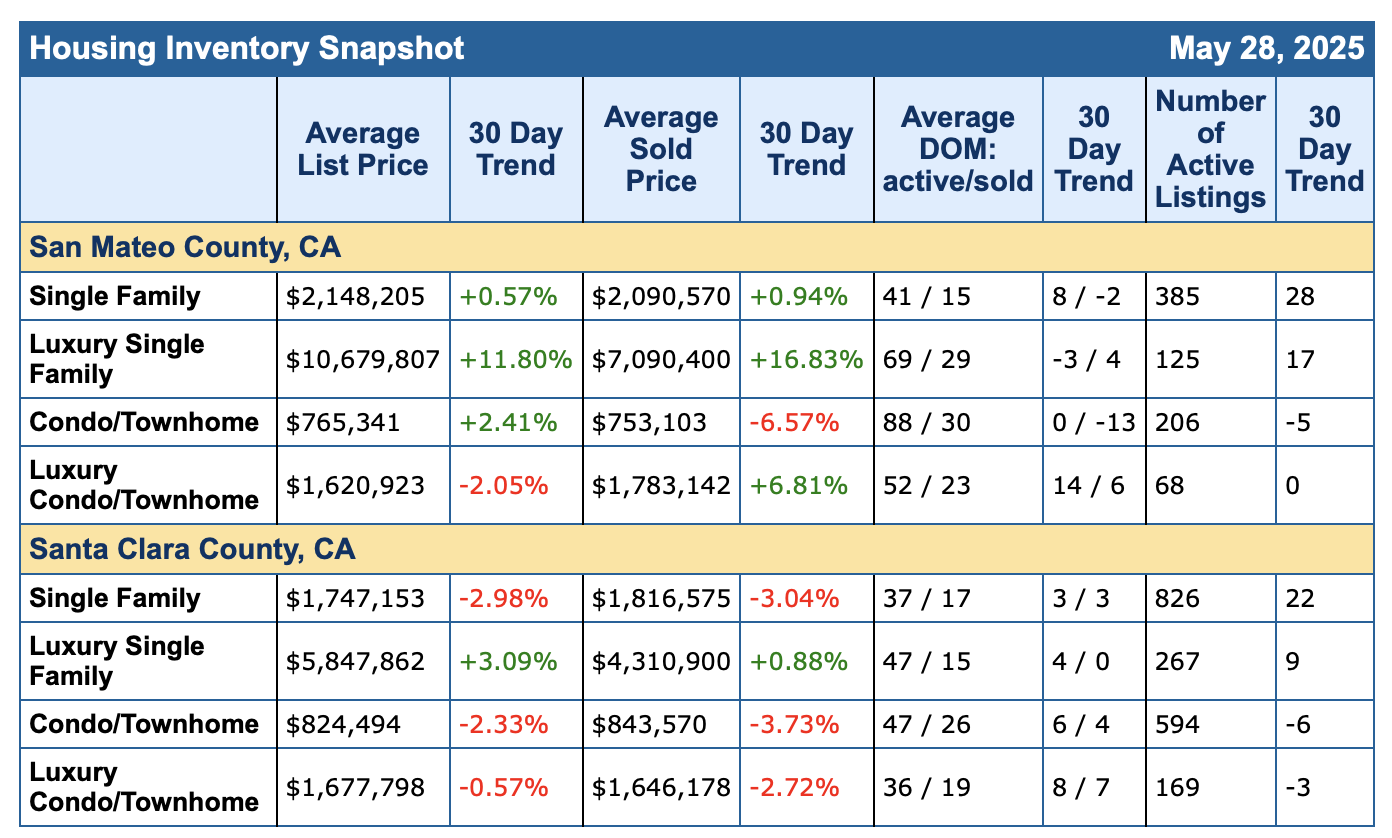

The stats are in for June 2025. What I see is price sensitivity. There is a lot of inventory on the market compared to years past, there is change in the air and it reflects in sales. We see some homes fetch multiple offers and sell over list price, but not crazy over. We also see some homes sitting and taking price reductions to attract offers. This year just feels different from the past 21 summers I’ve been in Real Estate. But that is not necessarily a bad thing. When the market is different that often is a great time to buy. All depends on where, when and the budget. So…. If you’re considering a Real Estate move, contact The Caton Team for a free consultation. With over 40 years of combined Real Estate experience, we have the knowledge and know-how to guide you to your goal. Call us at 650.799.4333 or email us at info@TheCatonTeam.com.

Whether you are selling or buying – today or tomorrow – contact The Caton Team – we’re happy to help you achieve your Real Estate goals.

Effective. Efficient. Responsive. The Caton Team 🏡

Each market is unique and with over 40 years of combined Real Estate experience, The Caton Team is more than happy to be of service if and when you are considering a move. Contact us anytime during your journey, together we’ll help you achieve your Real Estate goals.

Got Questions? The Caton Team is here to help.

Call| Text | Sabrina 650.799.4333 |EMAIL | WEB| BLOG

We love what we do and would love to help you navigate your sale or purchase of Residential Real Estate. Please reach out for a personal consultation. Please enjoy our free resources below and get to know our team TESTIMONIALS.

Got Real Estate Questions? The Caton Team is here to help.

We strive to be more than just Realtors – we are also your home resource. If you have any real estate questions, concerns, need a referral, or need some guidance – we are here for you. Contact us at your convenience – we are but a call, text or click away!

The Caton Team believes, in order to be successful in the San Fransisco | Peninsula | Bay Area | Silicon Valley Real Estate Market we have to think and act differently. We do this by positioning our clients in the strongest light, representing them with the utmost integrity, while strategically maneuvering through negotiations and contracts. Together we make dreams come true.

A mother and daughter-in-law team with over 35 years of combined, local Real Estate experience and knowledge – wouldn’t you like The Caton Team to represent you? Let us know how we can be of service. Contact us any time.

Call| Text | Sabrina 650.799.4333 | Susan 650.796.0654 |EMAIL | WEB| BLOG

The Caton Team – Susan & Sabrina A Family of Realtors Effective. Efficient. Responsive. What can we do for you?

When our long time friends needed to sell the family home – it was a honor to get the call. This 100+ year old home was in the family for over 60 years, raising multiple generations. But it was time. Time to move on.

Each home and client is unique and so is the plan for sale. Together we came up what was best for the client on their time line. Then it was time for us to shine.

We held two weekends of open houses and set an offer date – yes – even in this odd market of Spring /Summer 2025. We were grateful to receive 3 very strong and compelling offers.

Thank you Eric Ma with Bay One Realty for a smooth transaction. We are grateful to work with professionals such as yourself.

We love what we do – How can The Caton Team help You?

We truly enjoy helping our clients sell their homes. The Caton Team loves what we do and would love to help you – please enjoy our resources below. Get to know us at through our clients words.

Got Real Estate Questions? The Caton Team is here to help.

We strive to be more than just Realtors – we are also your home resource. If you have any real estate questions, concerns, need a referral or some guidance – we are here for you. Contact us at your convenience – we are but a call, text or click away!

The Caton Team believes, in order to be successful in the San Fransisco | Peninsula | Bay Area | Silicon Valley Real Estate Market we have to think and act differently. We do this by positioning our clients in the strongest light, representing them with the utmost integrity, while strategically maneuvering through negotiations and contracts. Together we make dreams come true.

A mother and daughter-in-law team with over 35 years of combined, local Real Estate experience and knowledge – would’t you like The Caton Team to represent you? Let us know how we can be of service. Contact us any time.

Call | Text | Sabrina 650.799.4333 | Susan 650.796.0654 | EMAIL | WEB| BLOG

The Caton Team – Susan & Sabrina A Family of Realtors Effective. Efficient. Responsive. What can we do for you?

Options range from family loans to outright gifts to help your children buy a home.

If you want to help your children buy a home there are a number of ways to go about it, ranging from family loans to outright gifts. Lofty home prices, rising mortgage rates and a tight inventory of homes for sale have shut many young buyers out of the housing market. In 2023, the median age of home buyers was 49, the highest on record, according to a survey from the National Association of Realtors — which means first-time buyers are delaying their purchases. The typical first-time buyer was 35, one year less than last year’s all-time high.

With that in mind, parents (and grandparents) of would-be home buyers are often interested in helping out. Their options include gifting a down payment, co-signing a mortgage, jointly owning a home, making a loan, and buying a home outright for your children or grandchildren. Each of these avenues of financial support has its own perks and pitfalls.

First, consider how any assistance could affect family relationships. Your children or their spouses may be anxious or uncomfortable about accepting financial help from parents or in-laws. Siblings feelings matter, too. “If you have multiple children, spend some time upfront to understand how giving or loaning to one child might affect family dynamics,” says Mitchell Kraus, a certified financial planner based in Santa Monica, Calif. “We’ve seen years of resentment coming from a small loan to one family member when it was not available to another.”

Intra-family loans

One option that could benefit both parties is an intra-family loan. You may be able to offer your child a lower interest rate than a conventional mortgage lender would while still earning a higher interest rate than you could earn from a savings account. For example, if you provide your child with a mortgage at a 4.5% interest rate, you’ll earn almost four percentage points more than the 0.55% average yield for a bank savings account. Your child, meanwhile, will pay significantly less than the national average for a 30-year fixed-rate mortgage.

An intra-family loan works especially well for well-off individuals who can afford to give their children the money but prefer the financial discipline that comes with a loan, says Tim Burke, chief executive officer of National Family Mortgage, a family lending agency. “For many parents, the motivation to lend money over gifting it is just about personal accountability,” he says. “Parents feel the responsibilities that come with homeownership, and the satisfaction that comes with meeting these responsibilities builds character.”

That was the case for Mary and Terry Shaffer of Pittsburgh, who lent money to both of their children to buy homes in that city. “Our son and our daughter do not like things handed to them, although they deserve to be helped,” says Mary, 68. “They have worked hard, and they both had accumulated savings for their closing costs.”

If parents need assurance that their child can afford the monthly payments, they should ask the child to get preapproved for a conventional mortgage, Burke says. However, that could be difficult for some children, especially if they’re self-employed borrowers. Even if a self-employed individual’s debt-to-income ratio — the amount of debt you owe as a percentage of your monthly income — may support a loan, a single year in which income declines may cause a bank to reject the application.

If your child can’t get preapproval, it comes down to your judgment. “If you think your family member is not going to repay you, then don’t go through the exercise of setting up a loan that isn’t going to work,” Burke says.

Put the terms of the intra-family loan in writing so they’re clear and it’s an arm’s-length transaction, says Brian Lamborne, senior director of advanced planning at Northwestern Mutual. Putting the terms of the loan in writing can also help you deal with instances in which your children are unable to make payments. For example, you can agree ahead of time that should your child suffer financial hardship, payments will be deferred for a certain period of time — perhaps six months or up to a year — and moved to the end of the loan.

The loan agreement should contemplate worst-case scenarios as well. For example, you may want to state the conditions under which the parents could foreclose on the property so they can sell it and pay off the loan.

It’s also important to understand the tax implications for intra-family loans. Borrowers who itemize can only deduct interest on a loan secured by a mortgage if the mortgage has been properly recorded. In order to do that, families need to obtain a deed of trust and file it with the borrower’s local government authority, such as the registrar of deeds or country clerk’s office. A real estate attorney can help you draw up these documents.

If the loan exceeds $10,000, the IRS requires you to charge an interest rate equal to or above the Applicable Federal Rate (AFR), which the IRS publishes monthly. The interest must be reported as income on your tax return.

If you don’t want to act as the loan servicer, you could use National Family Mortgage to set up, document and service the loan. It will email payment reminders and monthly statements, collect and credit payments, and issue year-end IRS 1098 and 1099-INT tax forms. Cost: a one-time fee of $725 to $2,100, depending on the size of the loan, and optional loan servicing starting at $15 per month.

Making a gift

For some families, the easiest solution is to give children enough money to make a down payment or buy a house outright. Gifting spares families the hassle of a loan and damage to their relationships if a loan can’t be repaid. Mortgage lenders generally allow a relative to supply the entire down payment, but they will require a letter that provides the name of the giver, the amount of the gift and a statement that the giver doesn’t expect to be repaid.

As is the case with a loan, it’s important to understand the tax implications of this transaction. In 2024, you can give up to $18,000 per person to as many people as you’d like without having to file a gift tax return. Married couples can give up to $36,000 per person.

Any amount over the annual limit will reduce your exemption from the federal estate and gift tax. This isn’t a problem for most families because the federal estate tax exclusion is $13.61 million for 2024 or $27.22 million for married couples. However, if Congress fails to extend the 2017 Tax Cuts and Jobs Act, the exclusion will drop to about $6 million in 2026.

In any event, parents or grandparents should only give a gift they can afford without jeopardizing their own financial security. “There are no loans when it comes to your own retirement,” says Jennifer Weber, a CFP in Lake Success, N.Y. “So only help in ways that you can afford now and in the future.”

Other options: co-signing and co-borrowing

If your child can’t qualify for a mortgage based on their own income and credit record but can afford monthly payments, co-signing a mortgage is one way to help them buy a home. However, it can be risky.

A co-signer acts as a guarantor for the primary borrower, promising to assume responsibility for repayment if the primary borrower doesn’t pay as required. The lender will review your sources of income and your credit to ensure your income is high enough and your credit strong enough to qualify for a mortgage.

If your child falls behind on monthly payments, your own credit could suffer. Plus, co-signing for a mortgage will increase your own debt-to-income ratio which could make it more difficult for you to borrow for your own purposes. Also, some lenders don’t allow co-signers.

In another arrangement, a co-borrower or joint applicant shares ownership of the loan and assumes responsibility for payments from the start. In general, you and your child combined must put down at least 20%, and your child must cover the first 5% of the down payment from their own funds. Otherwise, the property may qualify as an investment, in which case you’ll be charged a higher interest rate for the loan and be required to have more financial reserves. But If your child fails to pay the mortgage, property taxes or insurance on time, that could ding your credit history or result in a lien against the property.

Cell| Sabrina 650.799.4333 |Susan 650.796.0654 | EMAIL | WEB| BLOG

We love what we do and would love to help you navigate your sale or purchase of Residential Real Estate. Please reach out for a personal consultation. Please enjoy our free resources below and get to know our team from our TESTIMONIALS.

Effective. Efficient. Responsive. The Caton Team 🏡

Got Real Estate Questions? The Caton Team is here to help.

We strive to be more than just Realtors – we are also your home resource. If you have any real estate questions, concerns, need a referral, or some guidance – we are here for you. Contact us at your convenience – we are but a call, text or click away!

The Caton Team believes, in order to be successful in the San Fransisco | Peninsula | Bay Area | Silicon Valley Real Estate Market we have to think and act differently. We do this by positioning our clients in the strongest light, representing them with the utmost integrity, while strategically maneuvering through negotiations and contracts. Together we make dreams come true.

A mother and daughter-in-law team with over 35 years of combined, local Real Estate experience and knowledge – wouldn’t you like The Caton Team to represent you? Let us know how we can be of service. Contact us any time.

Cell | Sabrina 650.799.4333 | Susan 650.796.0654 | EMAIL | WEB| BLOG

The Caton Team – Susan & Sabrina A Family of Realtors Effective. Efficient. Responsive. What can we do for you?

Buying a home is one of the biggest financial decisions you’ll ever make. It’s exciting, but it can also feel overwhelming if you don’t have the right guidance. The key to navigating the homebuying process with confidence is understanding the steps involved and working with the right professionals. Here’s how you can make your journey smoother and more successful.

1. Get Pre-Approved for a Mortgage

One of the first steps to take when buying a home is getting pre-approved for a mortgage. This gives you a clear understanding of your budget and strengthens your position when making an offer. Lenders will review your credit, income, and financial history to determine how much you qualify for. Having a pre-approval letter in hand signals to sellers that you are a serious buyer.

2. Work with a Knowledgeable Real Estate Agent (like The Caton Team)

A real estate agent can be your best ally in the homebuying process. They have access to market insights, negotiation expertise, and a deep understanding of the home search and purchase process. Choose an agent with experience in your preferred area who can help you find the right home and guide you through each step of the transaction.

3. Understand the Market and Set Realistic Expectations

Before you start house hunting, take the time to research the local real estate market. Look at property prices, neighborhood trends, and inventory levels. This helps you set realistic expectations about what you can afford and what’s available within your budget. Your real estate agent can provide valuable insights to help you make informed decisions.

4. Make a Competitive Offer

Once you find the right home, it’s time to make an offer. Your agent will help you determine a fair price based on comparable properties and market conditions. In competitive markets, you may need to act quickly and include strong terms, such as a larger earnest money deposit or a flexible closing timeline, to make your offer stand out.

5. Conduct a Thorough Home Inspection

A home inspection is a crucial step that helps uncover potential issues with the property. Hiring a professional inspector ensures you know about any hidden problems before closing. If significant issues arise, you may have the option to negotiate repairs or reconsider your purchase.

6. Secure Financing and Prepare for Closing

Once your offer is accepted, work closely with your lender to finalize your mortgage. This involves submitting required documents, locking in your interest rate, and reviewing loan terms. Additionally, you’ll need to secure homeowners insurance and complete any final paperwork. Your real estate agent and lender will guide you through this process to ensure a smooth closing.

7. Close the Deal and Move In

The final step is closing day, where you’ll sign the necessary documents, make your down payment, and receive the keys to your new home. Before moving in, do a final walkthrough to confirm the property is in the agreed-upon condition. Then, celebrate—you’re officially a homeowner!

Final Thoughts

Buying a home doesn’t have to be stressful. With the right preparation, professional guidance, and a clear understanding of the process, you can confidently navigate your homebuying journey. If you’re looking for expert assistance, reach out to experienced mortgage professionals who can help you every step of the way.

Cell| Sabrina 650.799.4333 |Susan 650.796.0654 | EMAIL | WEB| BLOG

We love what we do and would love to help you navigate your sale or purchase of Residential Real Estate. Please reach out for a personal consultation. Please enjoy our free resources below and get to know our team from our TESTIMONIALS.

Effective. Efficient. Responsive. The Caton Team 🏡

Got Real Estate Questions? The Caton Team is here to help.

We strive to be more than just Realtors – we are also your home resource. If you have any real estate questions, concerns, need a referral, or some guidance – we are here for you. Contact us at your convenience – we are but a call, text or click away!

The Caton Team believes, in order to be successful in the San Fransisco | Peninsula | Bay Area | Silicon Valley Real Estate Market we have to think and act differently. We do this by positioning our clients in the strongest light, representing them with the utmost integrity, while strategically maneuvering through negotiations and contracts. Together we make dreams come true.

A mother and daughter-in-law team with over 35 years of combined, local Real Estate experience and knowledge – wouldn’t you like The Caton Team to represent you? Let us know how we can be of service. Contact us any time.

Cell | Sabrina 650.799.4333 | Susan 650.796.0654 | EMAIL | WEB| BLOG

The Caton Team – Susan & Sabrina A Family of Realtors Effective. Efficient. Responsive. What can we do for you?

Buying a home is a major milestone, but it also comes with challenges. Whether you’re navigating financial hurdles, competitive markets, or unexpected repairs, overcoming these obstacles can make homeownership even more rewarding. Here’s how you can turn challenges into triumphs.

1. Financial Preparation

Budgeting for homeownership goes beyond the down payment. Plan for closing costs, maintenance expenses, and emergency repairs to avoid financial stress down the road.

2. Competing in a Competitive Market

In hot markets, multiple buyers may be vying for the same property. Strengthen your position by getting pre-approved, making a strong offer, and working with a skilled real estate agent.

3. Managing Home Maintenance

Owning a home means taking care of ongoing maintenance. Set aside funds for routine upkeep and unexpected repairs to keep your property in top shape.

4. Long-Term Value

Think beyond the purchase—homeownership is a long-term investment. Keep up with property improvements, understand market trends, and consider refinancing opportunities to maximize your home’s value over time.

5. Embracing the Homeownership Mindset

Homeownership is not just about buying a property—it’s about creating stability, building wealth, and making memories. Approach challenges with a proactive mindset and embrace the journey to turn your home into a valuable and fulfilling asset.

By preparing for these challenges and staying proactive, you can turn homeownership into one of your greatest financial and personal achievements.

Cell| Sabrina 650.799.4333 |Susan 650.796.0654 | EMAIL | WEB| BLOG

We love what we do and would love to help you navigate your sale or purchase of Residential Real Estate. Please reach out for a personal consultation. Please enjoy our free resources below and get to know our team from our TESTIMONIALS.

Effective. Efficient. Responsive. The Caton Team 🏡

Got Real Estate Questions? The Caton Team is here to help.

We strive to be more than just Realtors – we are also your home resource. If you have any real estate questions, concerns, need a referral, or some guidance – we are here for you. Contact us at your convenience – we are but a call, text or click away!

The Caton Team believes, in order to be successful in the San Fransisco | Peninsula | Bay Area | Silicon Valley Real Estate Market we have to think and act differently. We do this by positioning our clients in the strongest light, representing them with the utmost integrity, while strategically maneuvering through negotiations and contracts. Together we make dreams come true.

A mother and daughter-in-law team with over 35 years of combined, local Real Estate experience and knowledge – wouldn’t you like The Caton Team to represent you? Let us know how we can be of service. Contact us any time.

Cell | Sabrina 650.799.4333 | Susan 650.796.0654 | EMAIL | WEB| BLOG

The Caton Team – Susan & Sabrina A Family of Realtors Effective. Efficient. Responsive. What can we do for you?

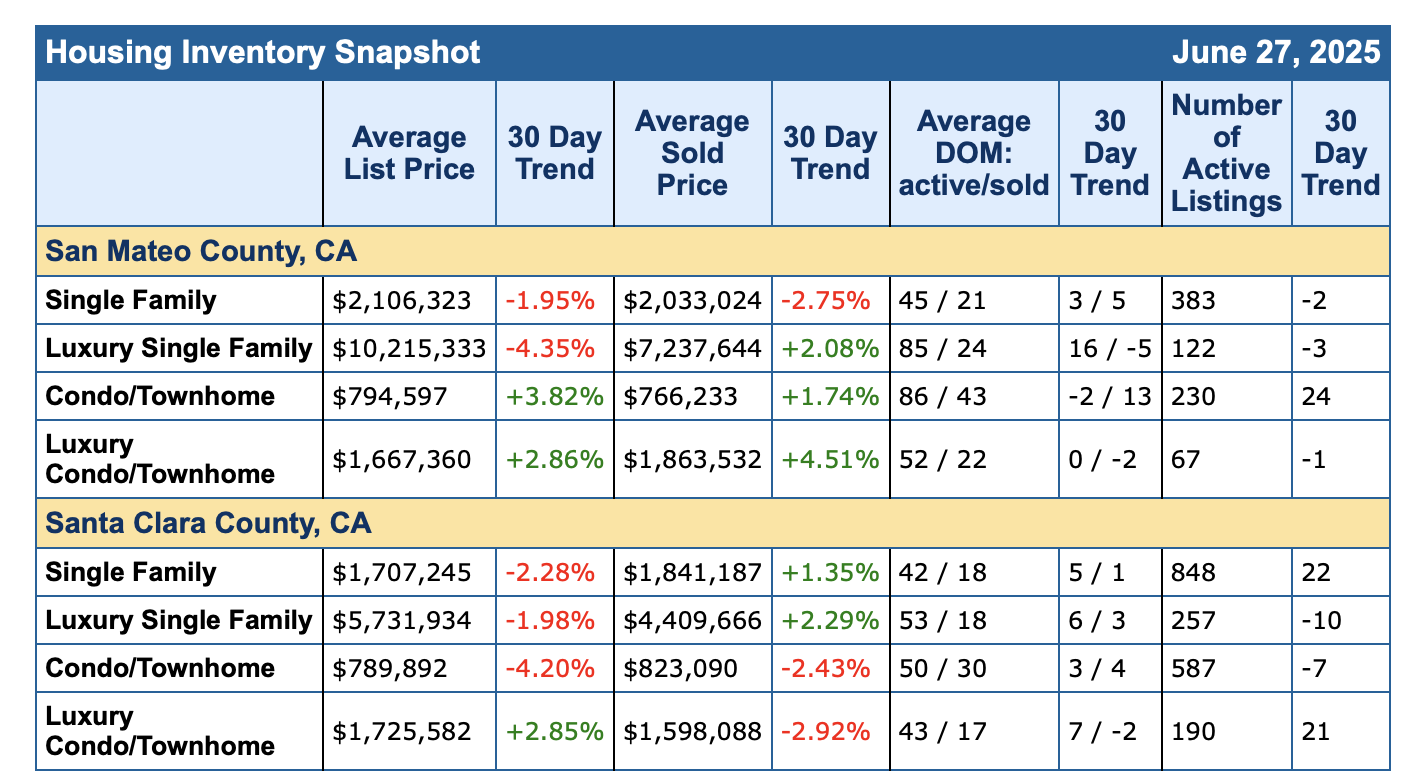

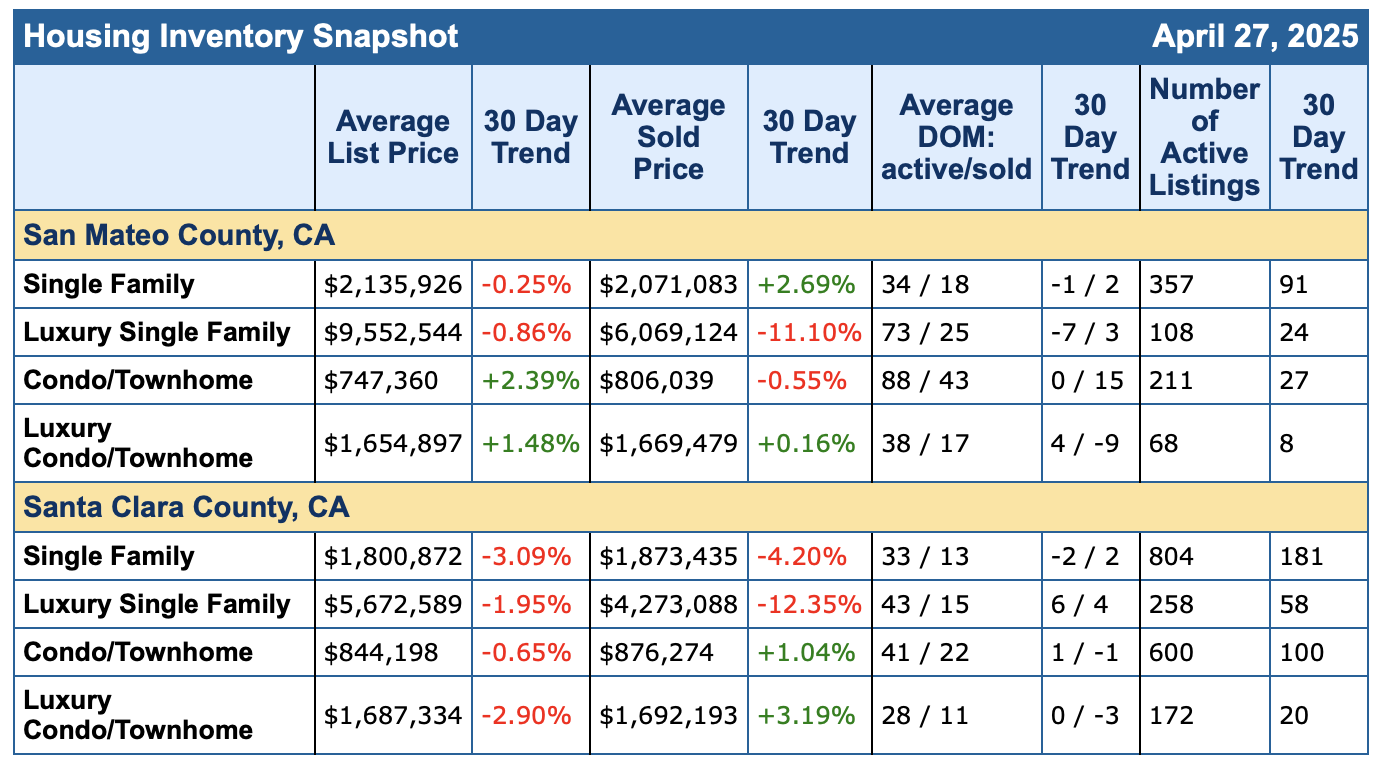

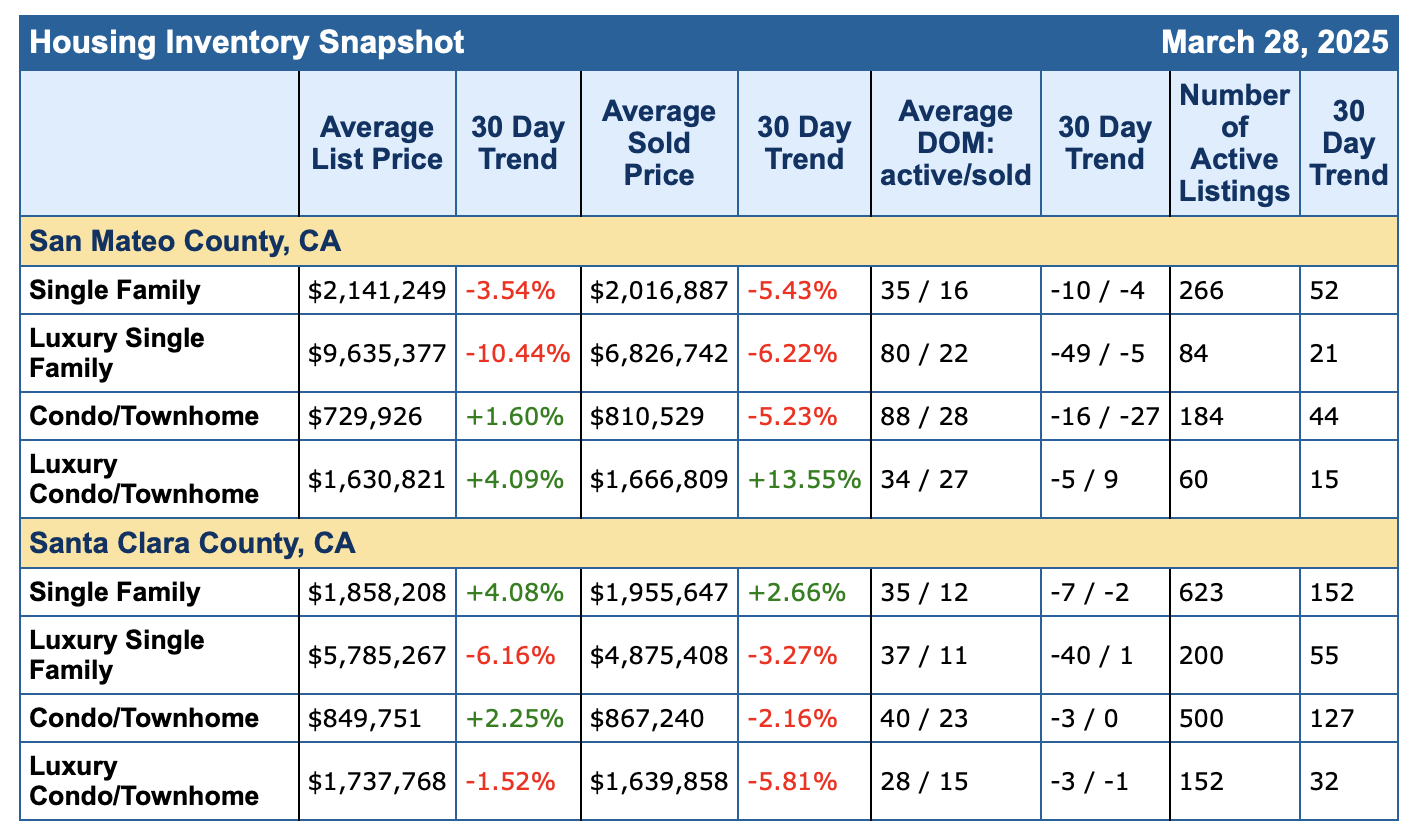

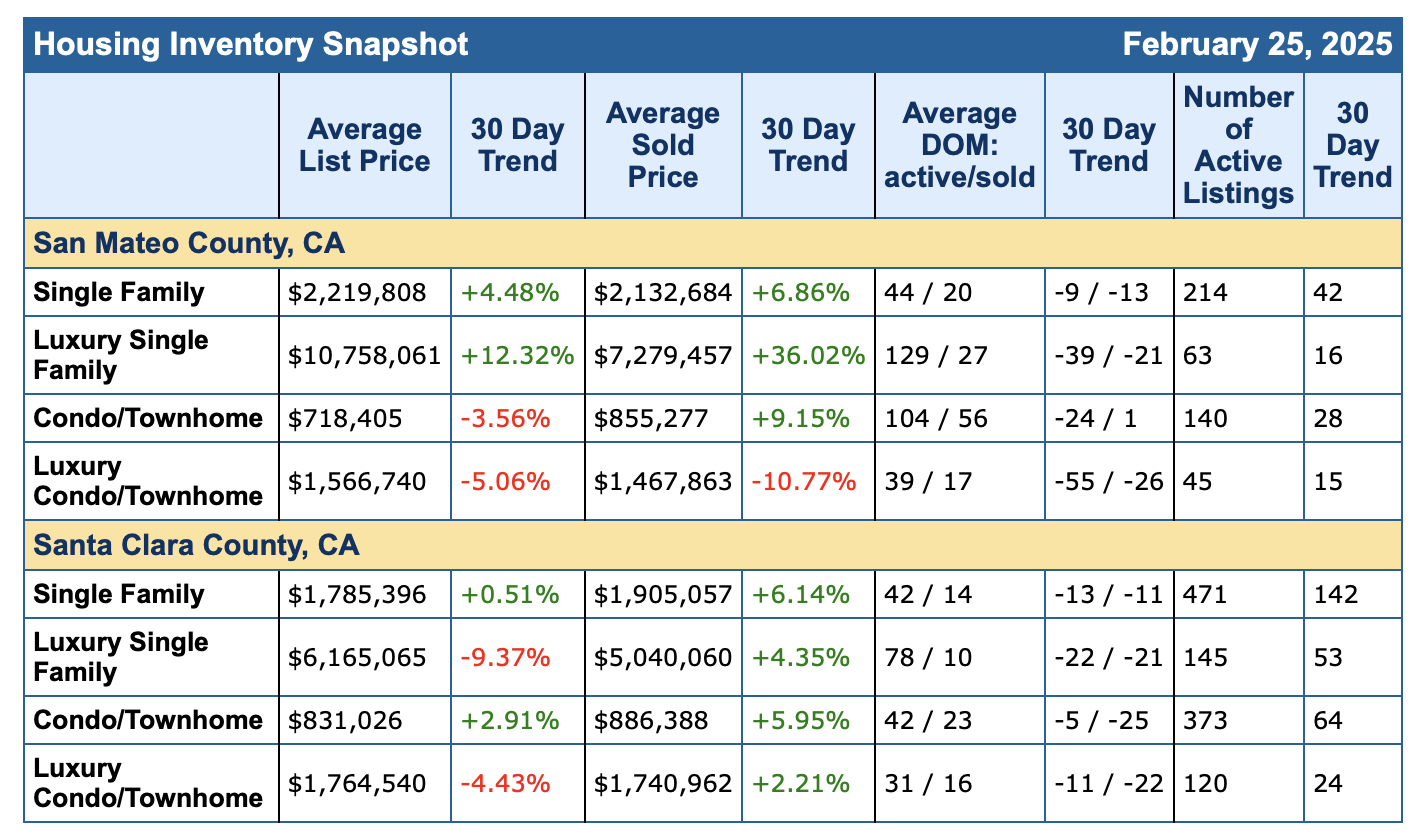

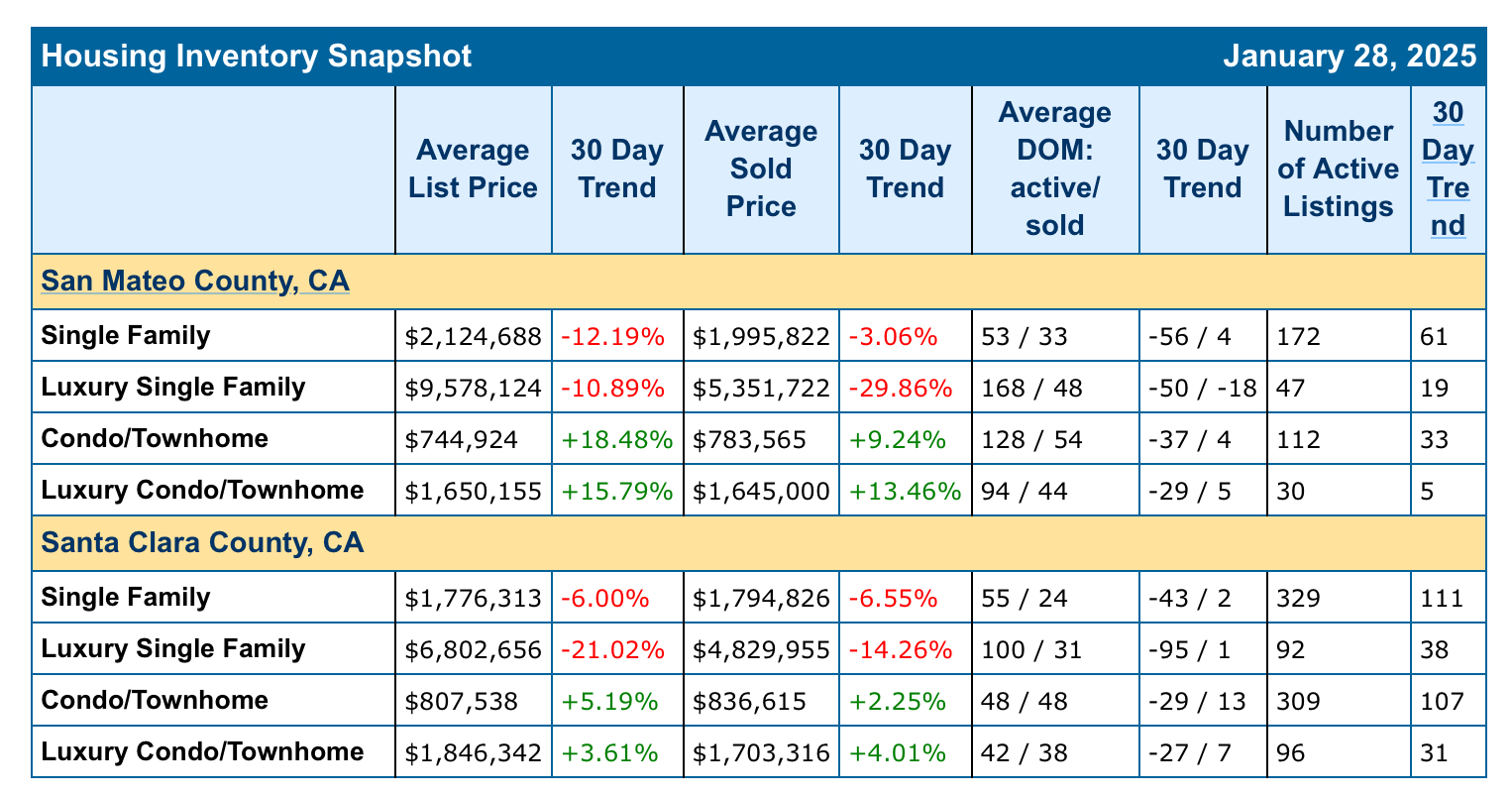

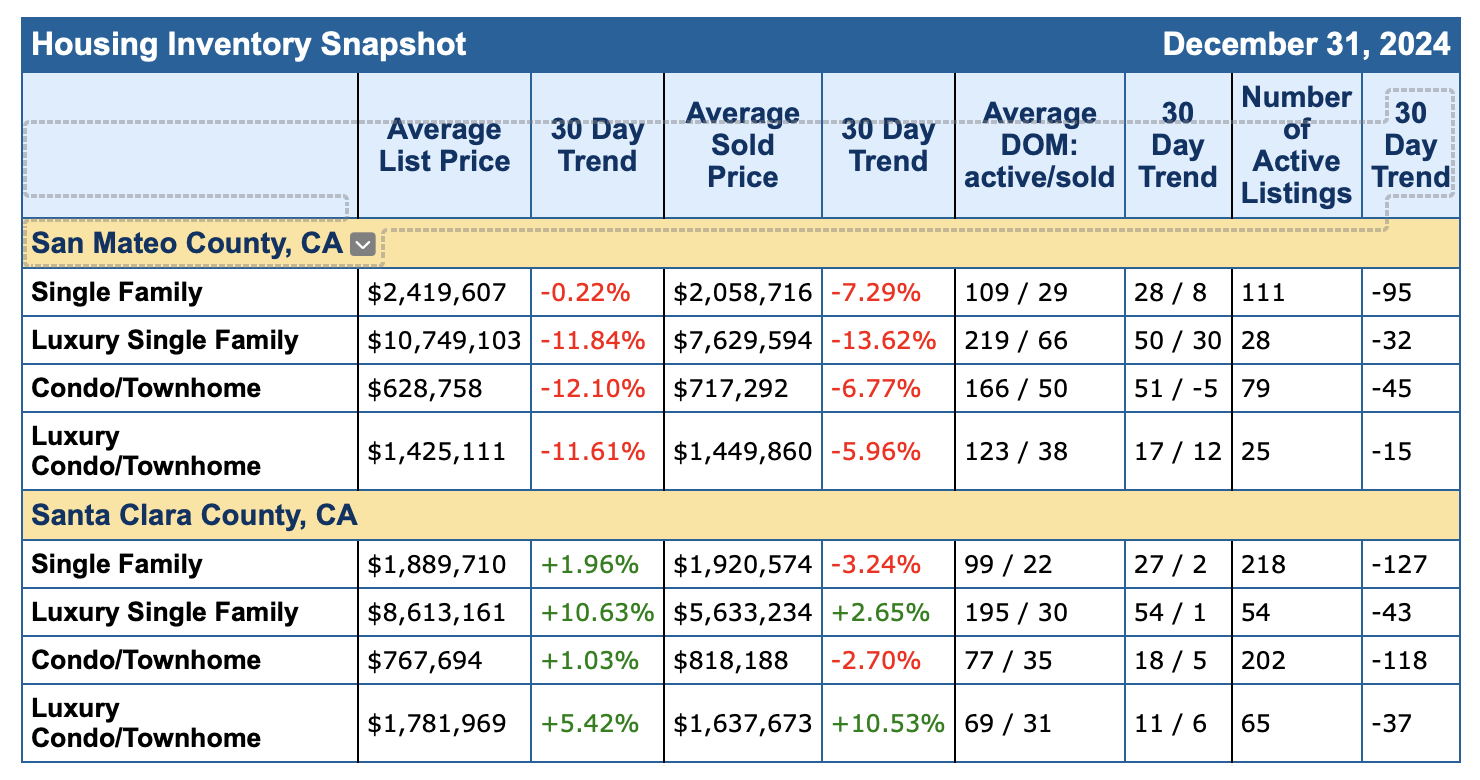

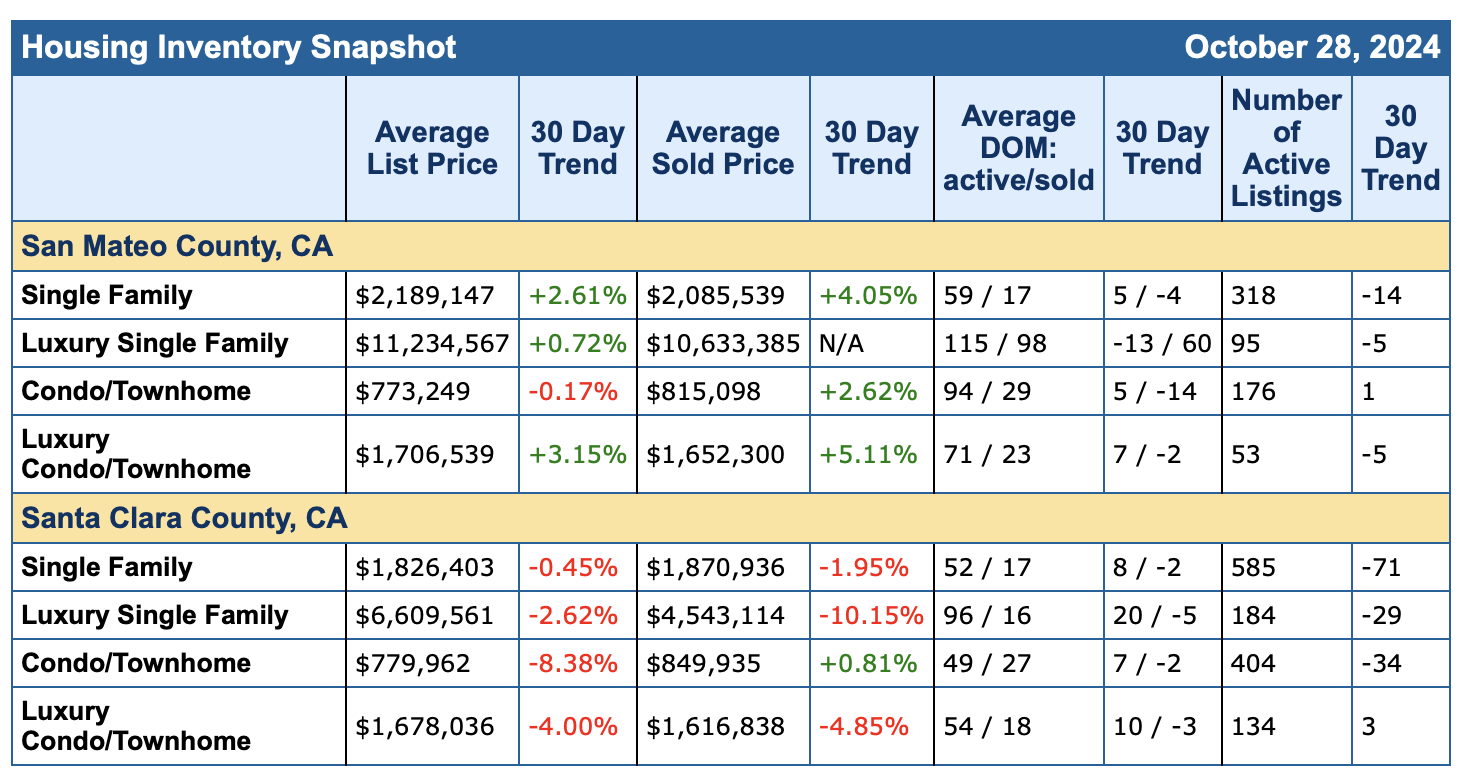

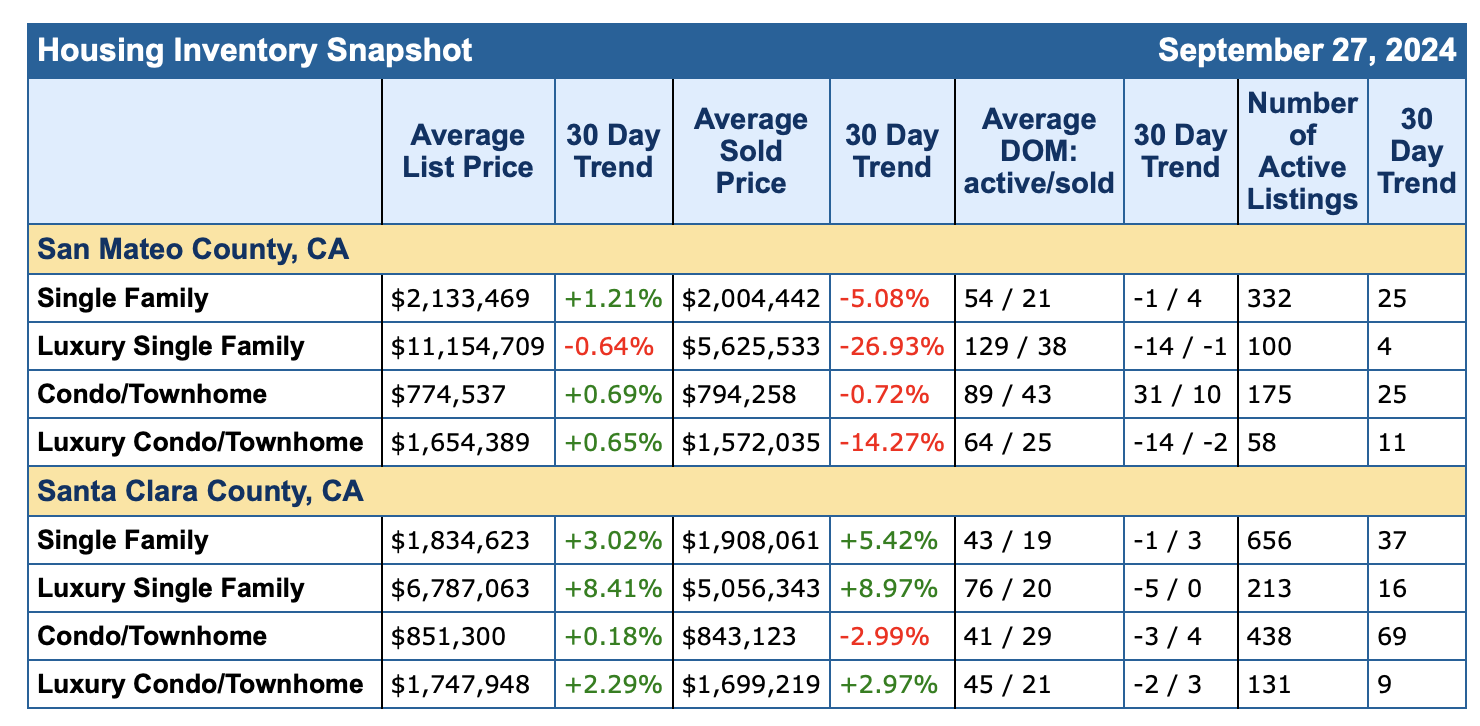

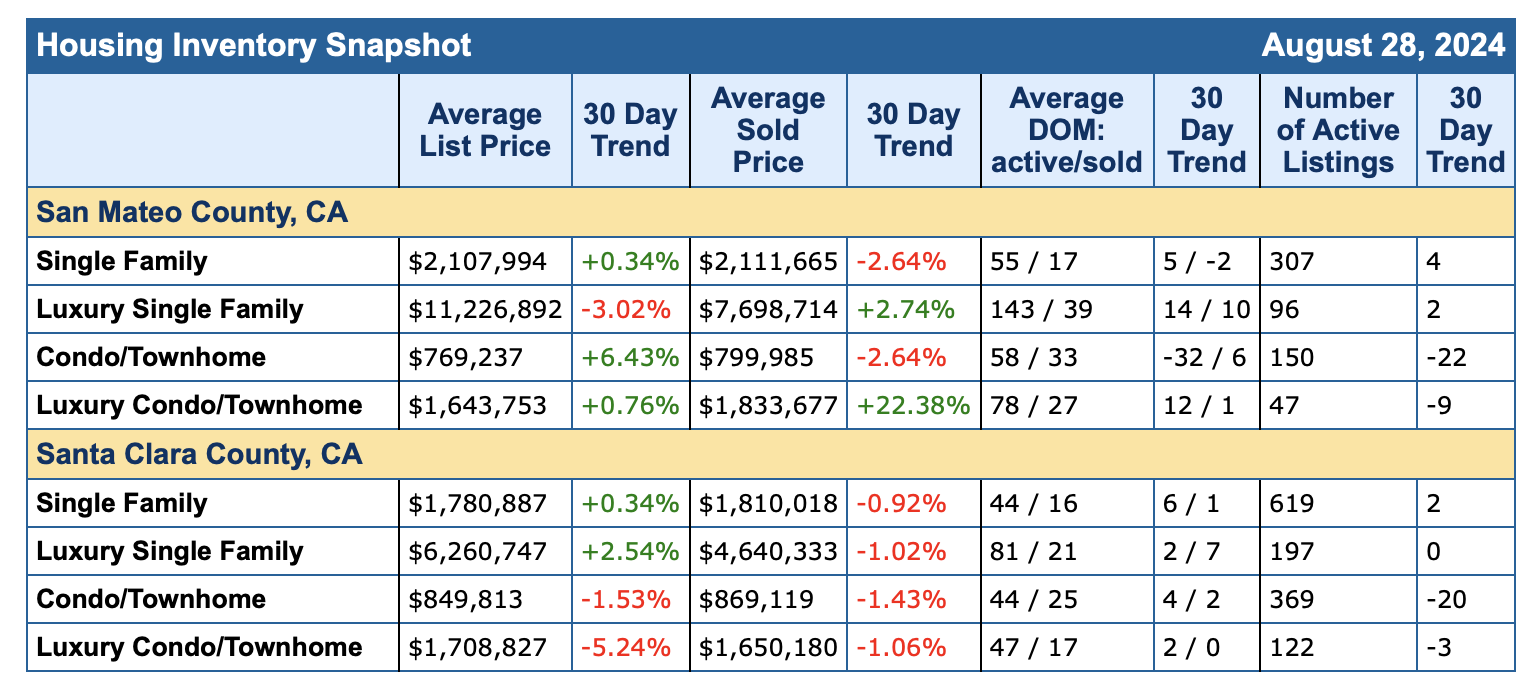

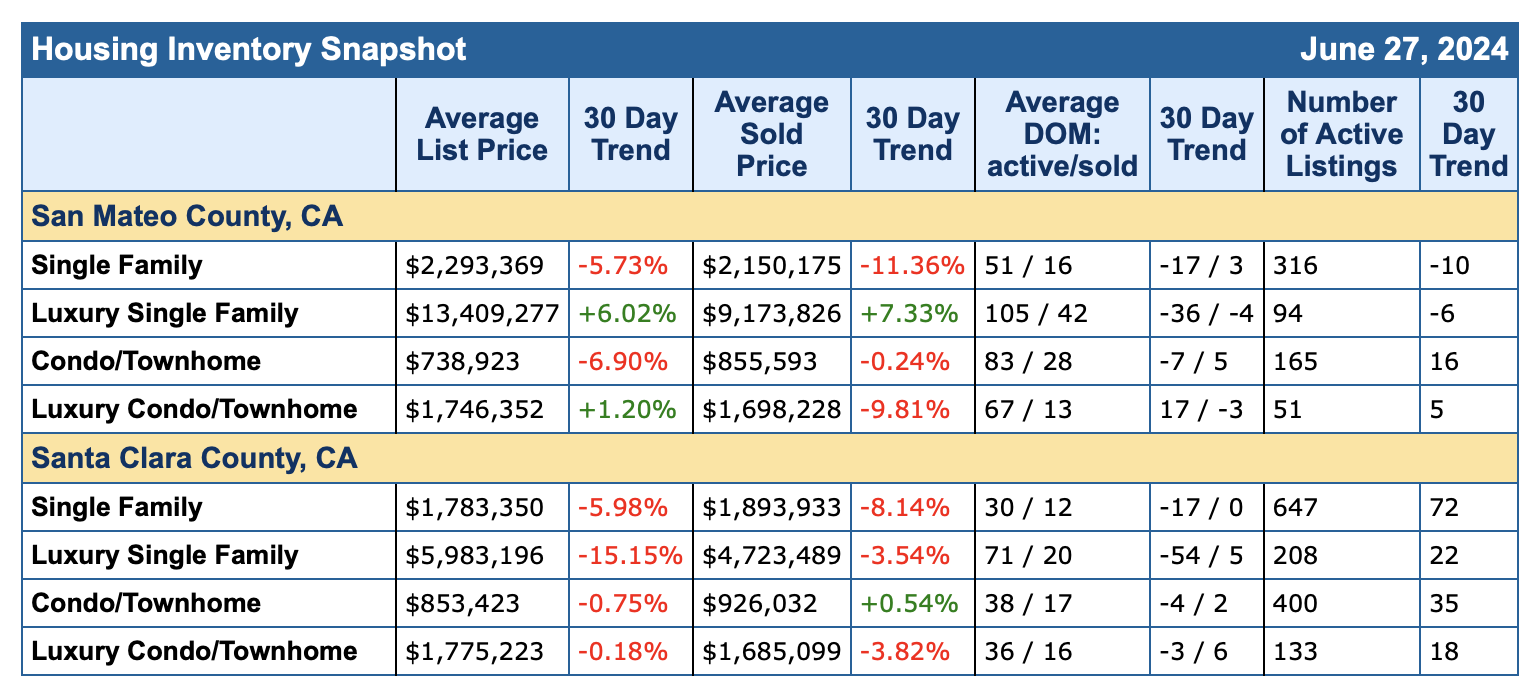

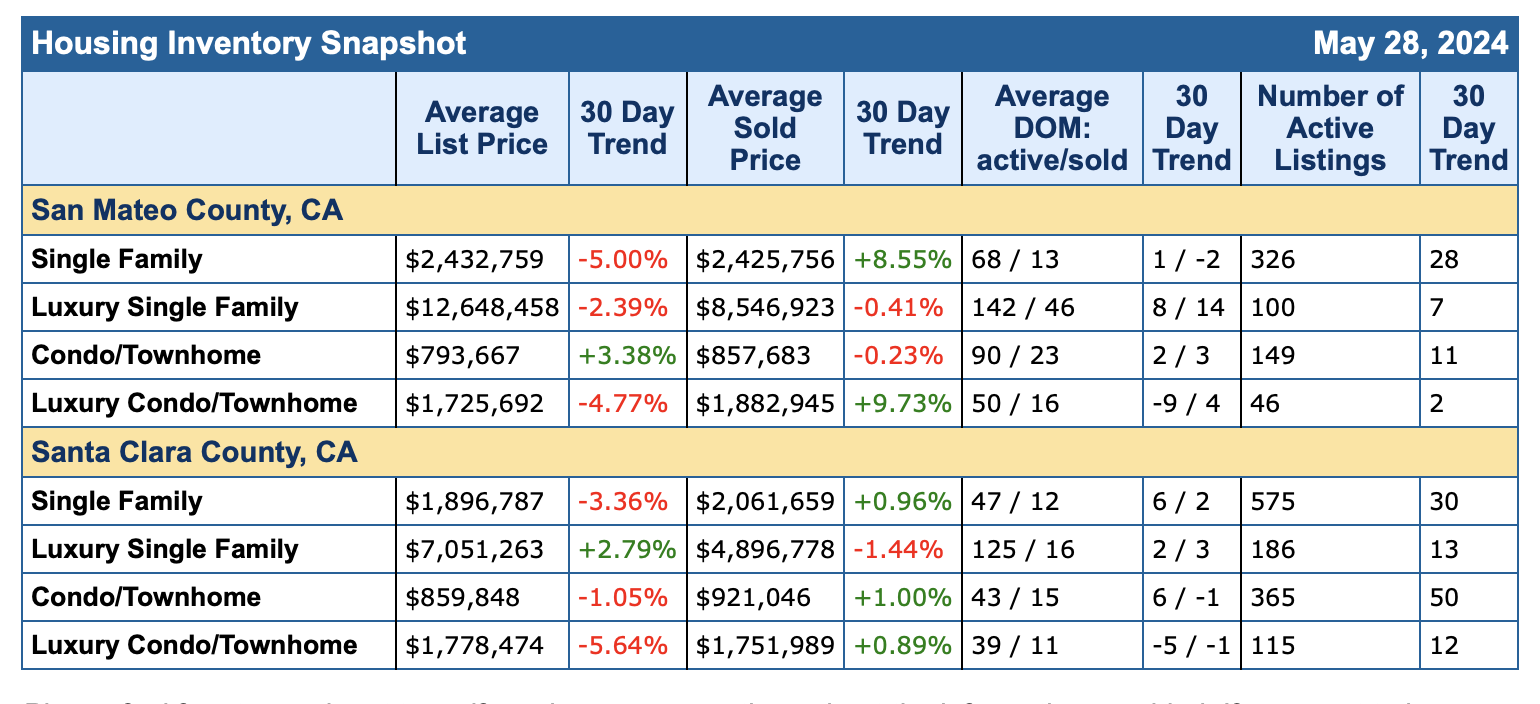

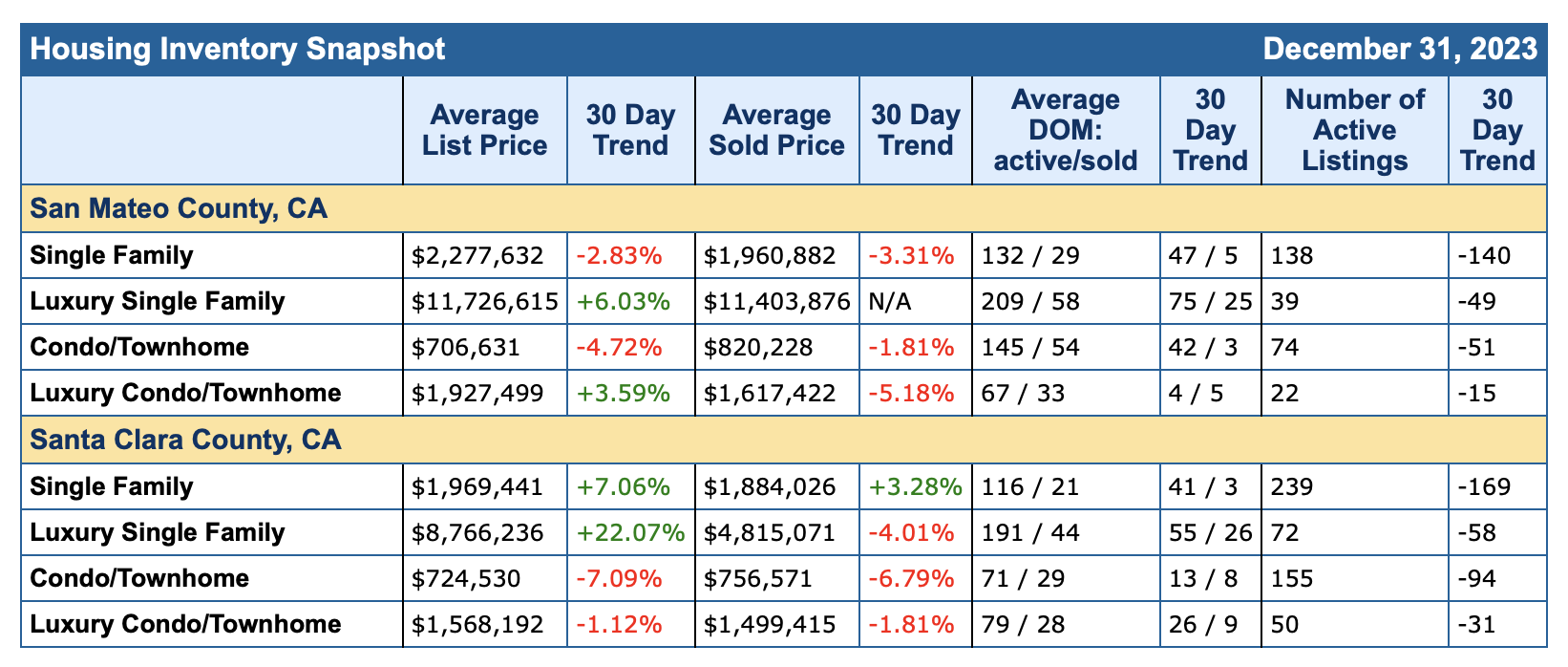

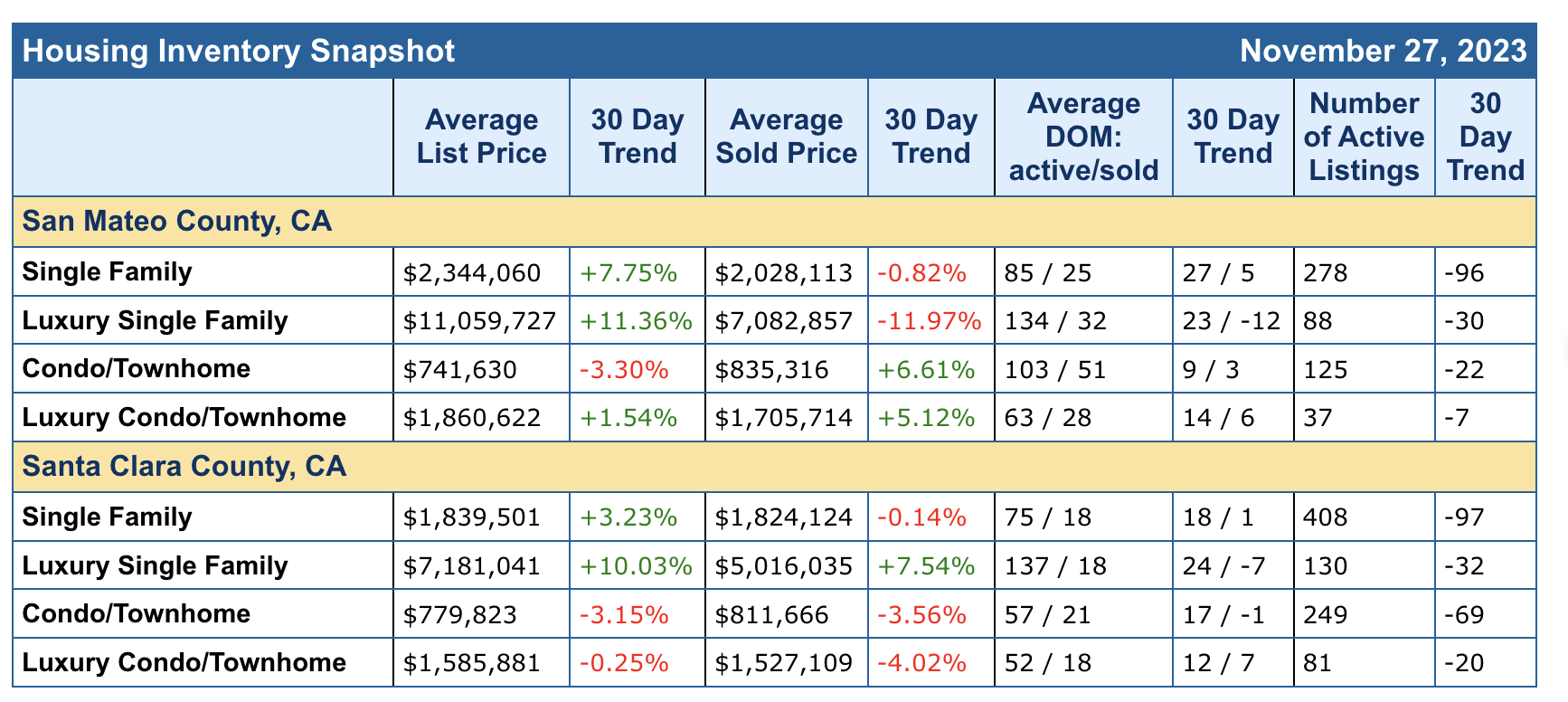

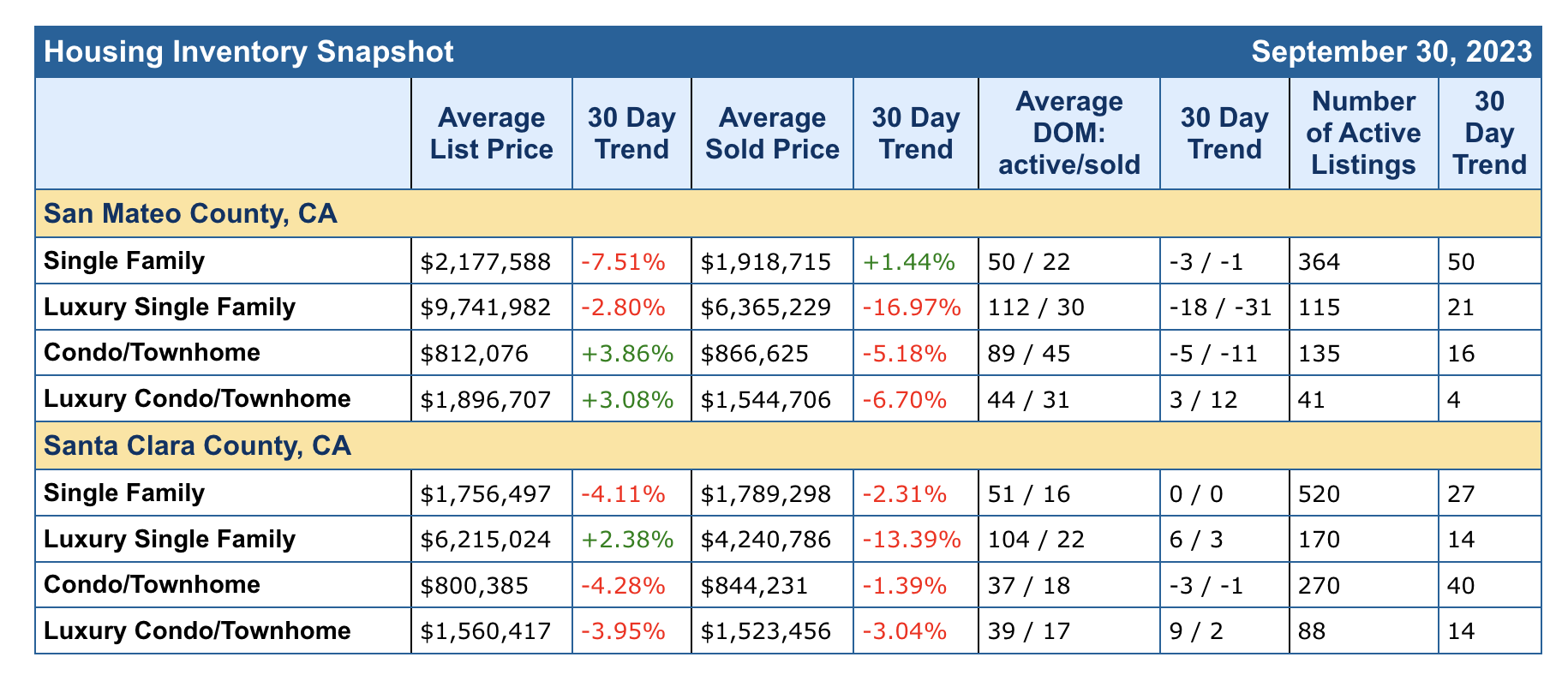

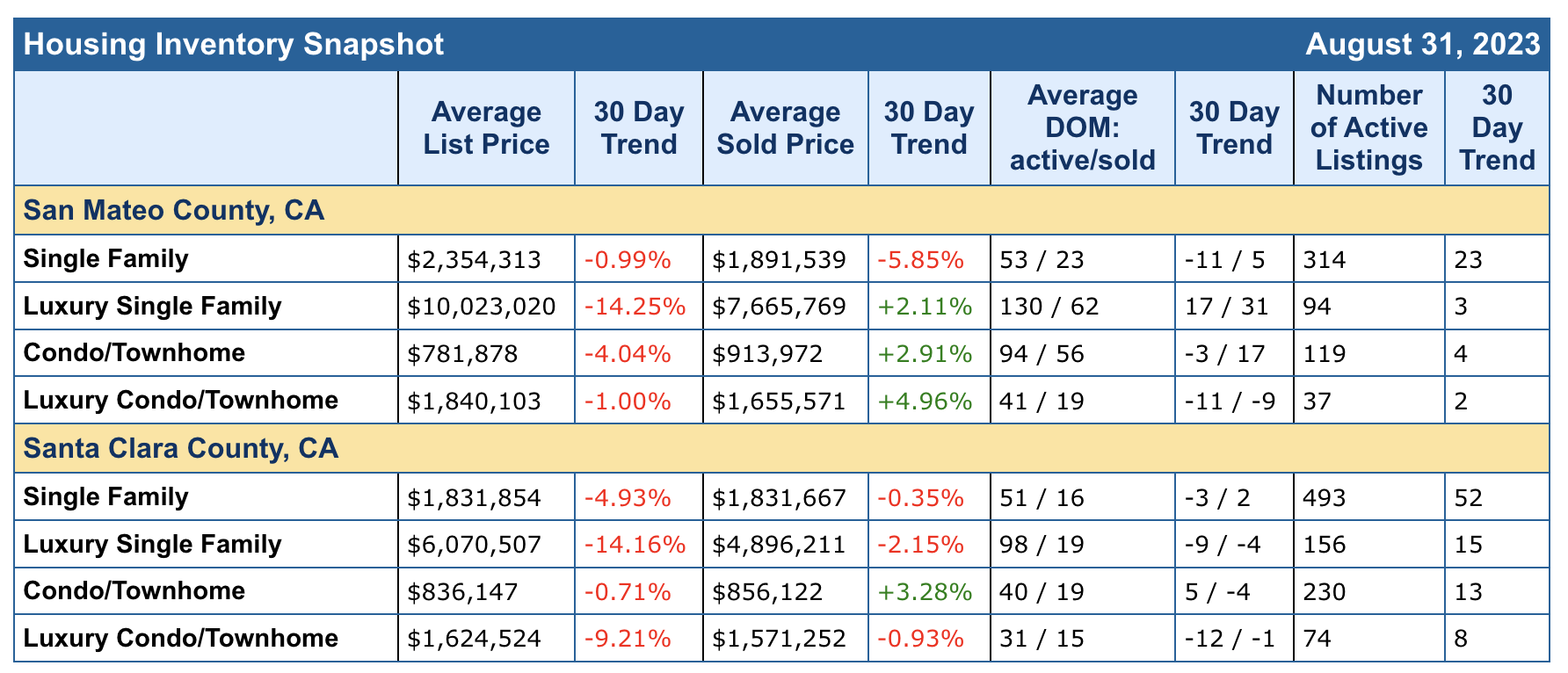

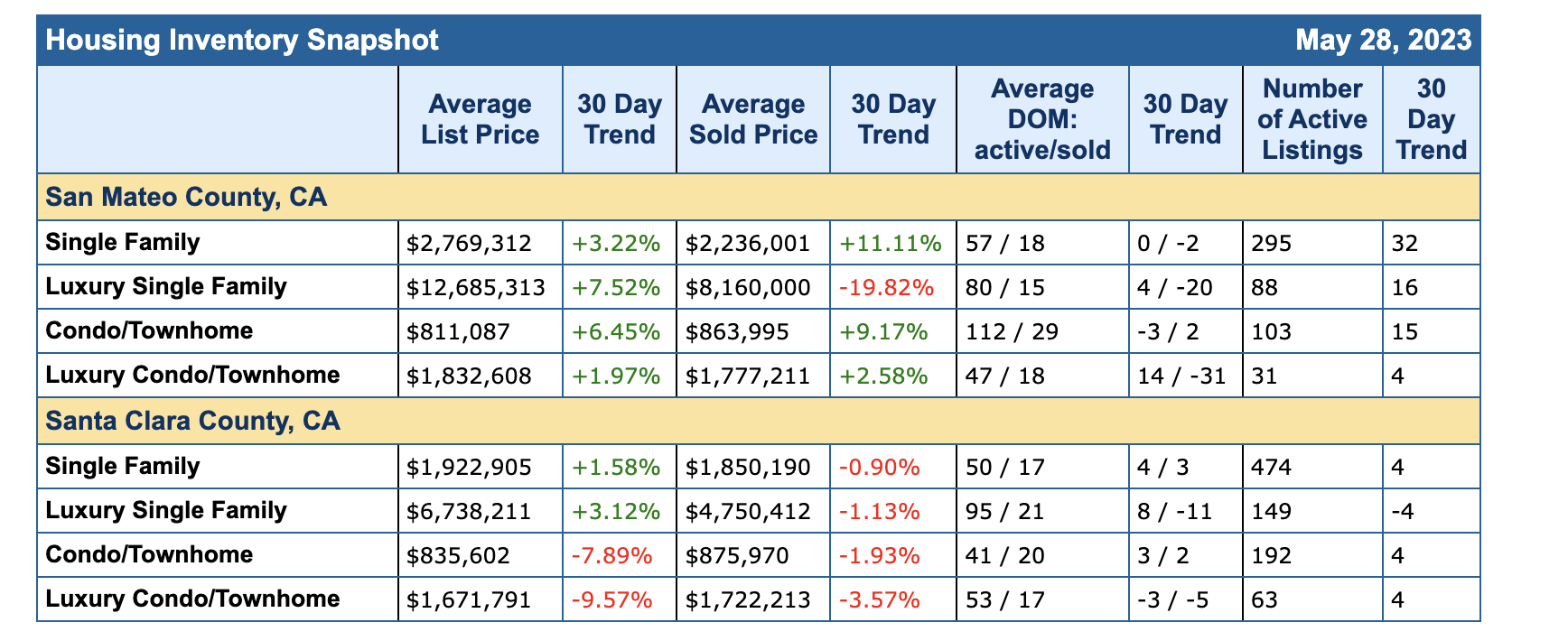

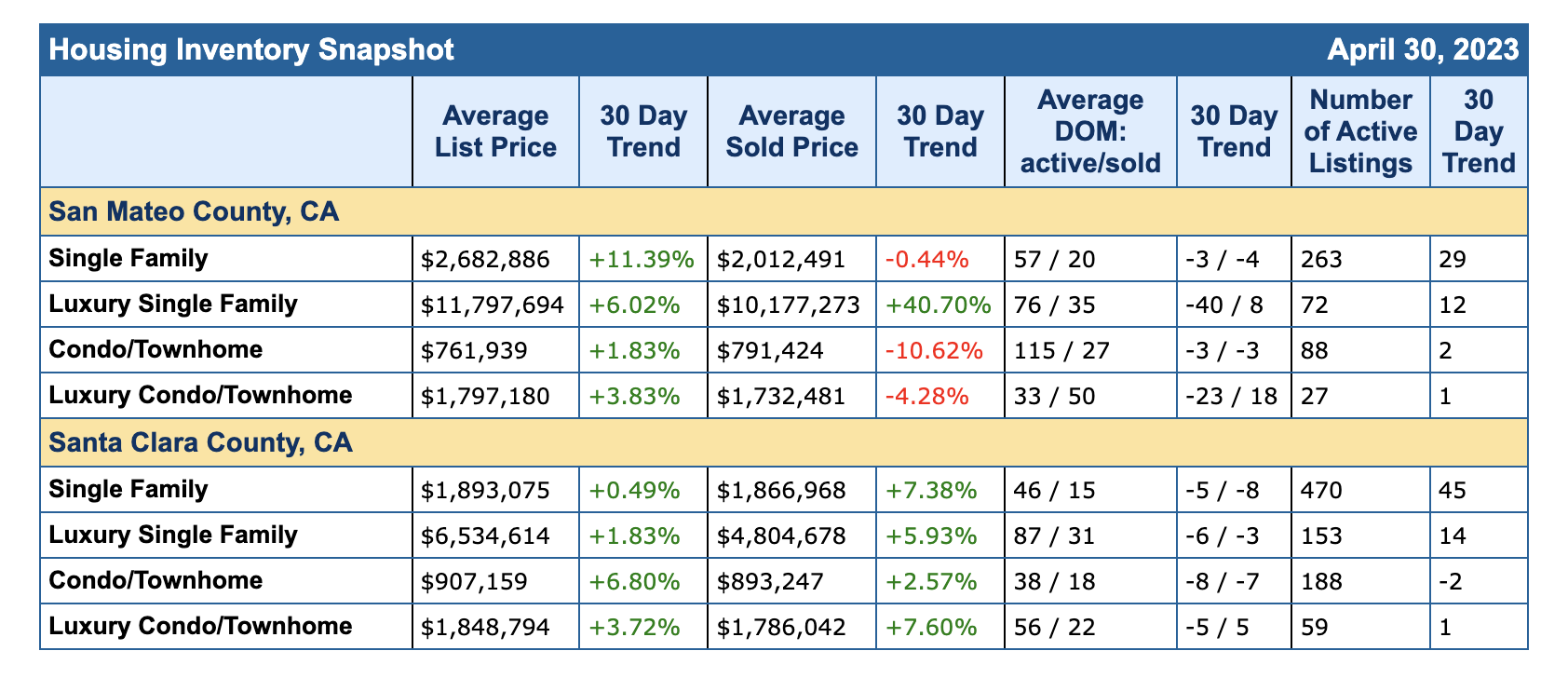

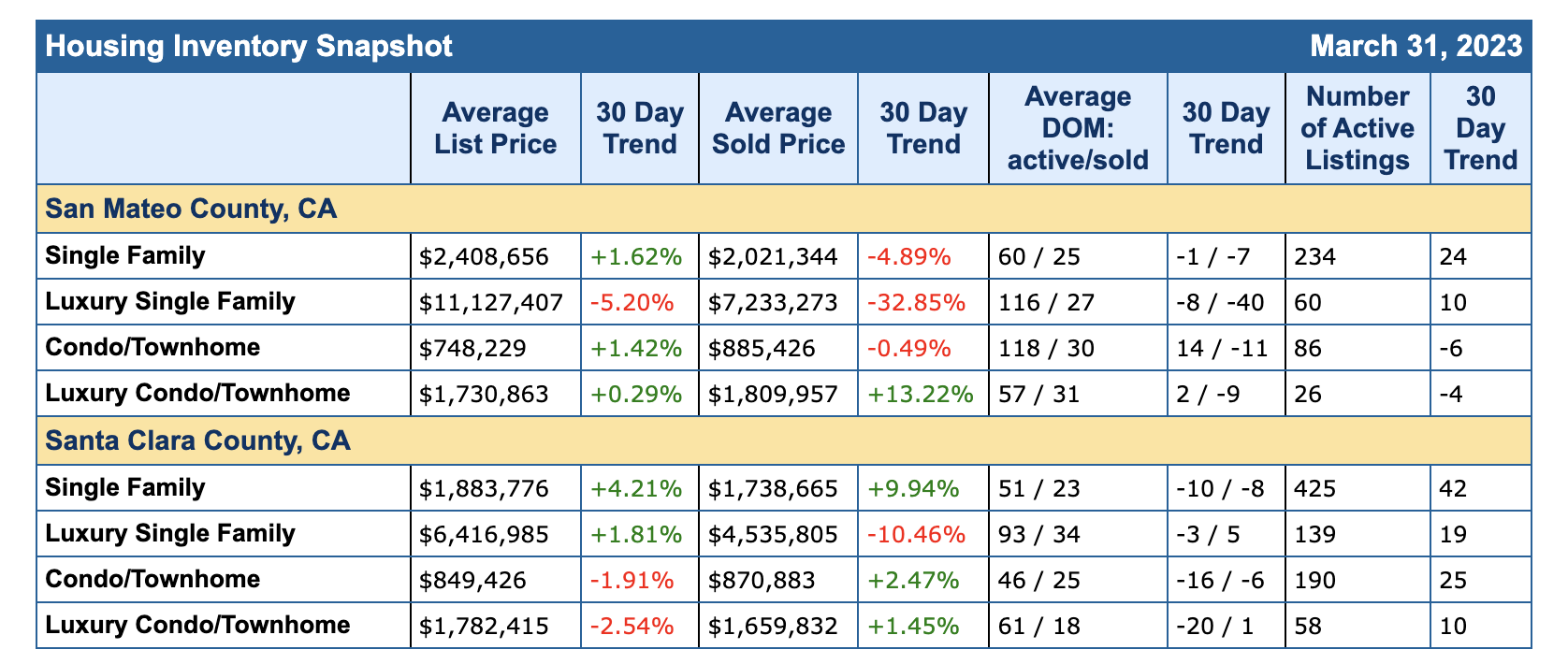

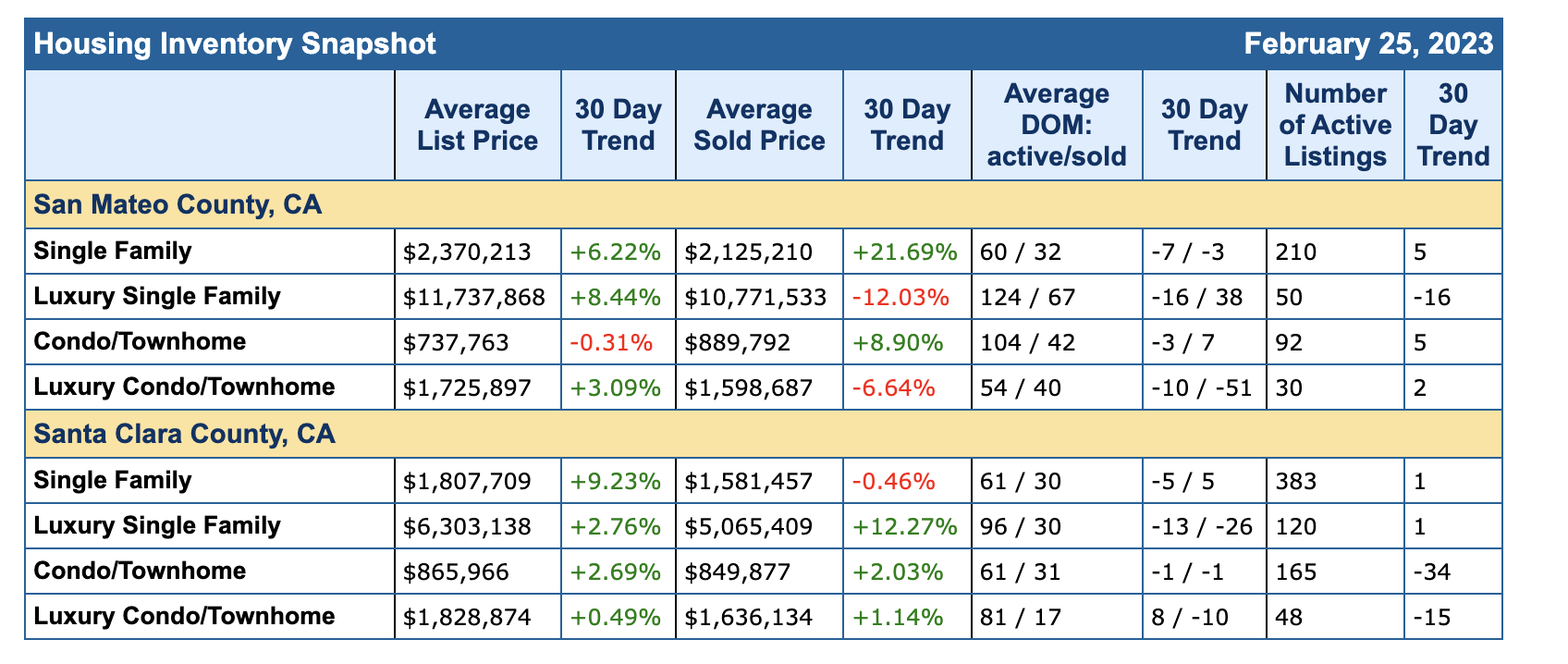

The stats are in for May 2025. In San Mateo County, there are gains in the Single Family Sector and Condo Market. List prices went up and so did the sale price. Though Condo took a slight dip – and I’ll lean on the HOA dues as a possible reason – or the any deck/balcony assessments. Looks like the luxury condo market took a dip list price – so that’s marketing you can see they sold at +6.81%.

In Santa Clara County, we see dips across the board with luxury sales holding tight. The news has reported an exodus in California but I’m seeing this more as an adjustment.

In the Bay Area, we still have demand thought right now there are many homes on the market in each county and some are sitting while some are selling within that two week window, with multiple offers. Each home and each client is unique. So if you’re thinking of buying or selling – reach out for a personal, free consultation. We love what we do and we’re happy to be of service.

If you’re considering a Real Estate move, contact The Caton Team for a free consultation. With over 40 years of combined Real Estate experience, we have the knowledge and know-how to guide you to your goal. Call us at 650.799.4333 or email us at info@TheCatonTeam.com.

Whether you are selling or buying – today or tomorrow – contact The Caton Team – we’re happy to help you achieve your Real Estate goals.

Effective. Efficient. Responsive. The Caton Team 🏡

Each market is unique and with over 40 years of combined Real Estate experience, The Caton Team is more than happy to be of service if and when you are considering a move. Contact us anytime during your journey, together we’ll help you achieve your Real Estate goals.

Got Questions? The Caton Team is here to help.

Call| Text | Sabrina 650.799.4333 |EMAIL | WEB| BLOG

We love what we do and would love to help you navigate your sale or purchase of Residential Real Estate. Please reach out for a personal consultation. Please enjoy our free resources below and get to know our team TESTIMONIALS.

Got Real Estate Questions? The Caton Team is here to help.

We strive to be more than just Realtors – we are also your home resource. If you have any real estate questions, concerns, need a referral, or need some guidance – we are here for you. Contact us at your convenience – we are but a call, text or click away!

The Caton Team believes, in order to be successful in the San Fransisco | Peninsula | Bay Area | Silicon Valley Real Estate Market we have to think and act differently. We do this by positioning our clients in the strongest light, representing them with the utmost integrity, while strategically maneuvering through negotiations and contracts. Together we make dreams come true.

A mother and daughter-in-law team with over 35 years of combined, local Real Estate experience and knowledge – wouldn’t you like The Caton Team to represent you? Let us know how we can be of service. Contact us any time.

Call| Text | Sabrina 650.799.4333 | Susan 650.796.0654 |EMAIL | WEB| BLOG

The Caton Team – Susan & Sabrina A Family of Realtors Effective. Efficient. Responsive. What can we do for you?

This year’s home design trends are all about warmth and comfort, personal touches that tell a story, and vintage design details that evoke a sense of nostalgia. To help you capture the charm of the vintage decor aesthetic, industry experts are giving us the scoop on what they’re most excited to see in 2025.

“The 2025 vintage aesthetic isn’t just about looking back—it’s about adding pieces to your home that feel fresh, curated, and uniquely personal,” says Margaret Carroll, founder and principal designer at Margaret Carroll Interiors.

The year’s Color of the Year announcements have served as a hint of what’s to come in the world of home decor—namely the color brown, which fits into a larger vintage-inspired color palette of rusty tones and deep eggplant hues. Wallpaper continues to be popular, with all-over pattern drenching and nostalgic block print patterns maximizing the vintage charm factor. Keep reading for this year’s hottest vintage trends, along with expert tips for implementing them in your own space.

Framed Vintage Items as Art

For a unique way to add vintage character to your walls, frame vintage items and create a meaningful gallery wall with them. “Consider framing vintage maps, quirky game boards, or even antique book pages for a look that feels layered and storied,” Carroll says. Choose frames carefully to create an intentional blend of the old and new. “Frames can lean contemporary with sleek burlwood or simple white matting, but mixing and matching wood tones adds an effortless, collected-over-time charm,” Carroll suggests.

Shades of Brown

There is a nostalgic warmth about the color brown. Design experts predict the color trend will continue into 2025, introducing vintage-inspired sophistication and a welcome reprieve from cool tones. “We’re seeing the color brown seep back into kitchens, furniture, and bathrooms for its rich, moody, natural vibe,” says Teri Simone, head of design and marketing at Nieu Cabinet Doors. Brown is a timeless neutral that ranges from dramatic chocolate tones to soothing sandy hues, proving it’s a versatile color whose vintage appeal translates well into modern interiors.

Vintage Lighting

Lighting presents a great opportunity to add vintage style and personality to a room. “The vintage lighting trend is gaining even more momentum as we head into 2025,” says Jennifer Jones, principal designer at Niche Interiors. She shares that one-of-a-kind vintage chandeliers are having a moment, as are midcentury modern floor lamps, antique desk lamps, and retro-style wall sconces. “Vintage lighting adds so much character to a space and doesn’t have to break the bank,” Jones says. She recommends checking local flea markets, thrift stores, and online shops like Etsy to find hidden lighting gems.

Vintage Linens Featuring Classic Patterns

When it comes to home textiles, Alecia Taylor, interior designer at CabinetNow, says vintage linens featuring classic patterns will be a big trend in 2025. The best part is, you can incorporate it in as big or small a way as you like; For a quick and inexpensive way to infuse your table setting with vintage charm, use fabric napkins with a classic gingham pattern or a pretty floral print tablecloth. For a larger-scale way to channel the trend, opt for a vintage-inspired fabric on window shades or curtain panels. “Look for classic patterns and colors that complement your existing decor,” Taylor says. This way, you can add a touch of nostalgic charm while enhancing the room’s character in a seamless manner.

Vintage-Inspired Color Palette

A warm and inviting vintage-inspired color palette is a big trend in 2025, as evidenced by most of the 2025 Color of the Year choices. Camilla Masi, interior designer at Otto Tiles & Design US, says this color trend can be seen in both kitchen and bathroom design right now. “Homeowners are looking towards nostalgia to add a sense of comfort and familiarity to their home and that is why vintage style interiors and decor are having a moment right now,” Masi explains. When piecing together a vintage-inspired color palette, she suggests shades such as classic steely blue, eggplant, nostalgic forest and olive greens, muddy browns, and creamy off-whites.

All-Over Pattern Drenching

When it comes to wallpaper, all-over pattern drenching is another big vintage trend to watch out for in 2025, according to Elizabeth Rees, CEO and co-founder of Chasing Paper. “When considering where and how to apply the wallpaper, the all-over pattern drenching approach can further elevate a space and create an all-encompassing design with the patterns of block print wallpaper,” she says. To give your home a warm and cozy makeover with ample vintage charm, Rees suggests installing going for all-over pattern drenching in a space like a bedroom. “Bedrooms are the most personal rooms in a home and block print wallpaper can help bring an enhanced sense of individuality to the space,” she says. To truly embrace the vintage trend, complete the space with soft accents and thoughtfully curated heirloom furniture.

Block Print Wallpaper

“Block print wallpapers are going to make a mark in 2025 with their artisanal hand-stamped charm, striking the perfect balance between timeless tradition and modern simplicity,” Rees says. She points out that block printing is one of the oldest printing techniques, which often features repetitive, imperfect patterns of geometric shapes, florals, botanicals, and other natural elements. This year, Rees says block print wallpaper is the vintage trend you’ll want to embrace if you want to evoke a sense of nostalgia.

Cell| Sabrina 650.799.4333 |Susan 650.796.0654 | EMAIL | WEB| BLOG

We love what we do and would love to help you navigate your sale or purchase of Residential Real Estate. Please reach out for a personal consultation. Please enjoy our free resources below and get to know our team from our TESTIMONIALS.

Effective. Efficient. Responsive. The Caton Team 🏡

Got Real Estate Questions? The Caton Team is here to help.

We strive to be more than just Realtors – we are also your home resource. If you have any real estate questions, concerns, need a referral, or some guidance – we are here for you. Contact us at your convenience – we are but a call, text or click away!

The Caton Team believes, in order to be successful in the San Fransisco | Peninsula | Bay Area | Silicon Valley Real Estate Market we have to think and act differently. We do this by positioning our clients in the strongest light, representing them with the utmost integrity, while strategically maneuvering through negotiations and contracts. Together we make dreams come true.

A mother and daughter-in-law team with over 35 years of combined, local Real Estate experience and knowledge – wouldn’t you like The Caton Team to represent you? Let us know how we can be of service. Contact us any time.

Cell | Sabrina 650.799.4333 | Susan 650.796.0654 | EMAIL | WEB| BLOG

The Caton Team – Susan & Sabrina A Family of Realtors Effective. Efficient. Responsive. What can we do for you?

We’re so grateful when our clients share their kind words with us. We love what we do and we love taking great care of our clients.

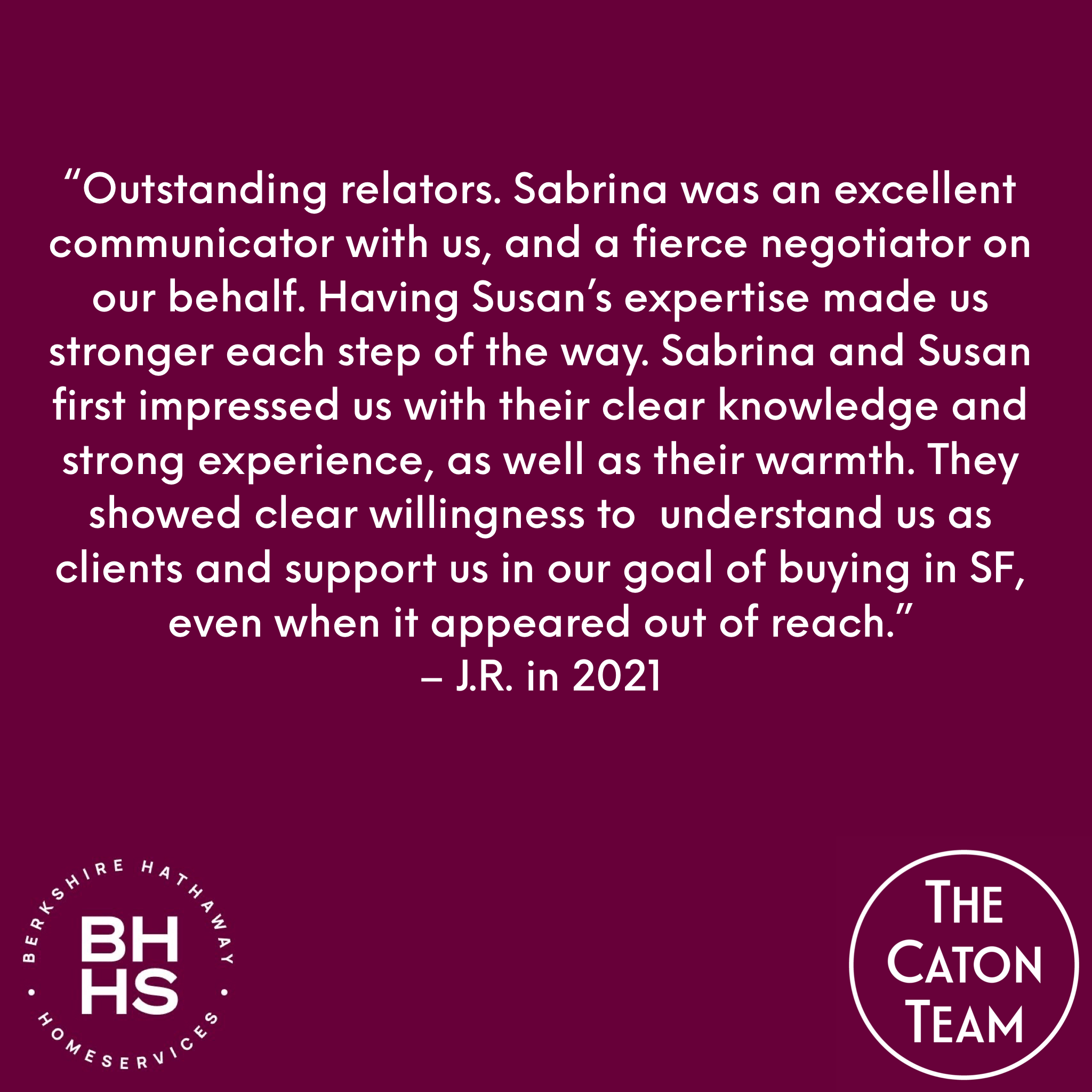

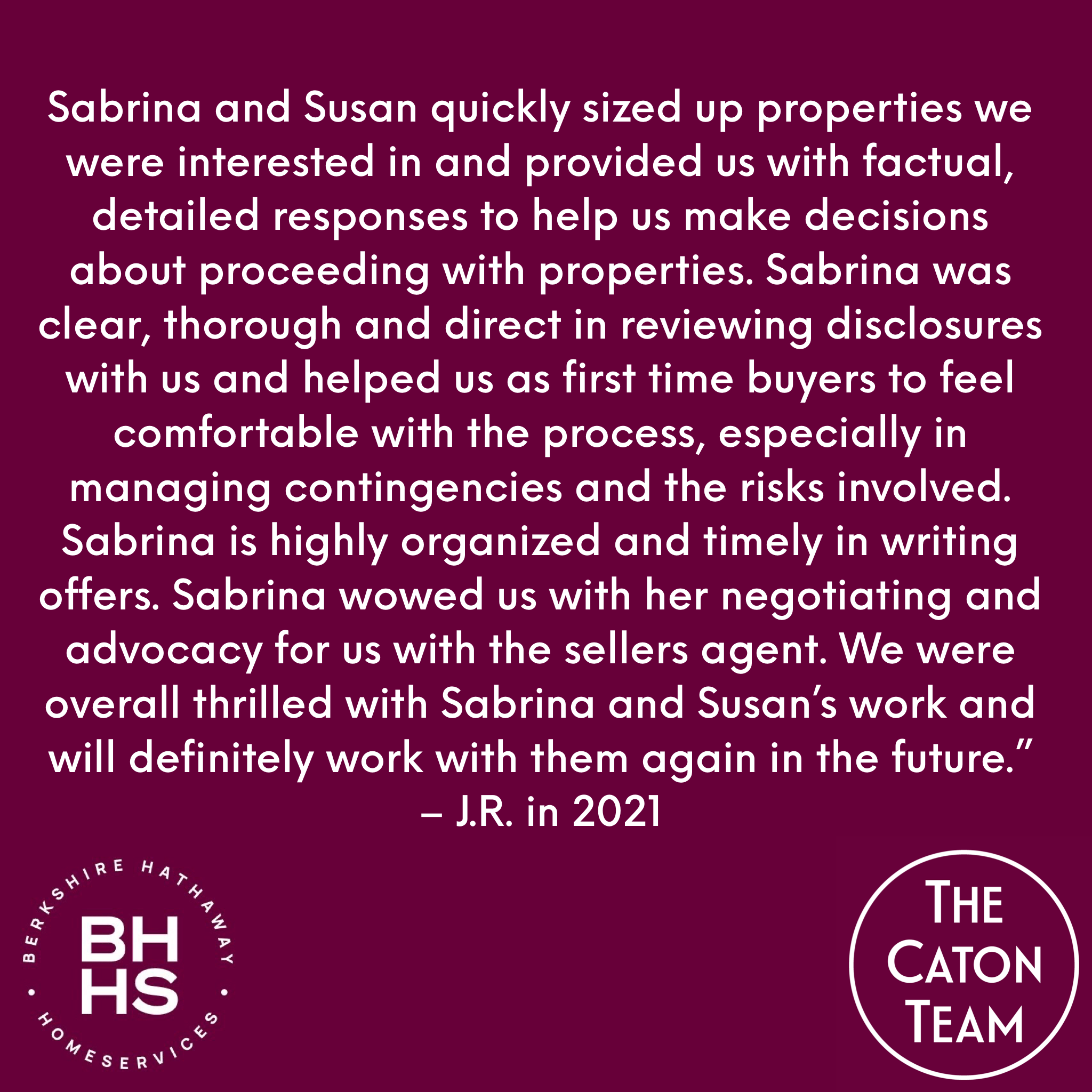

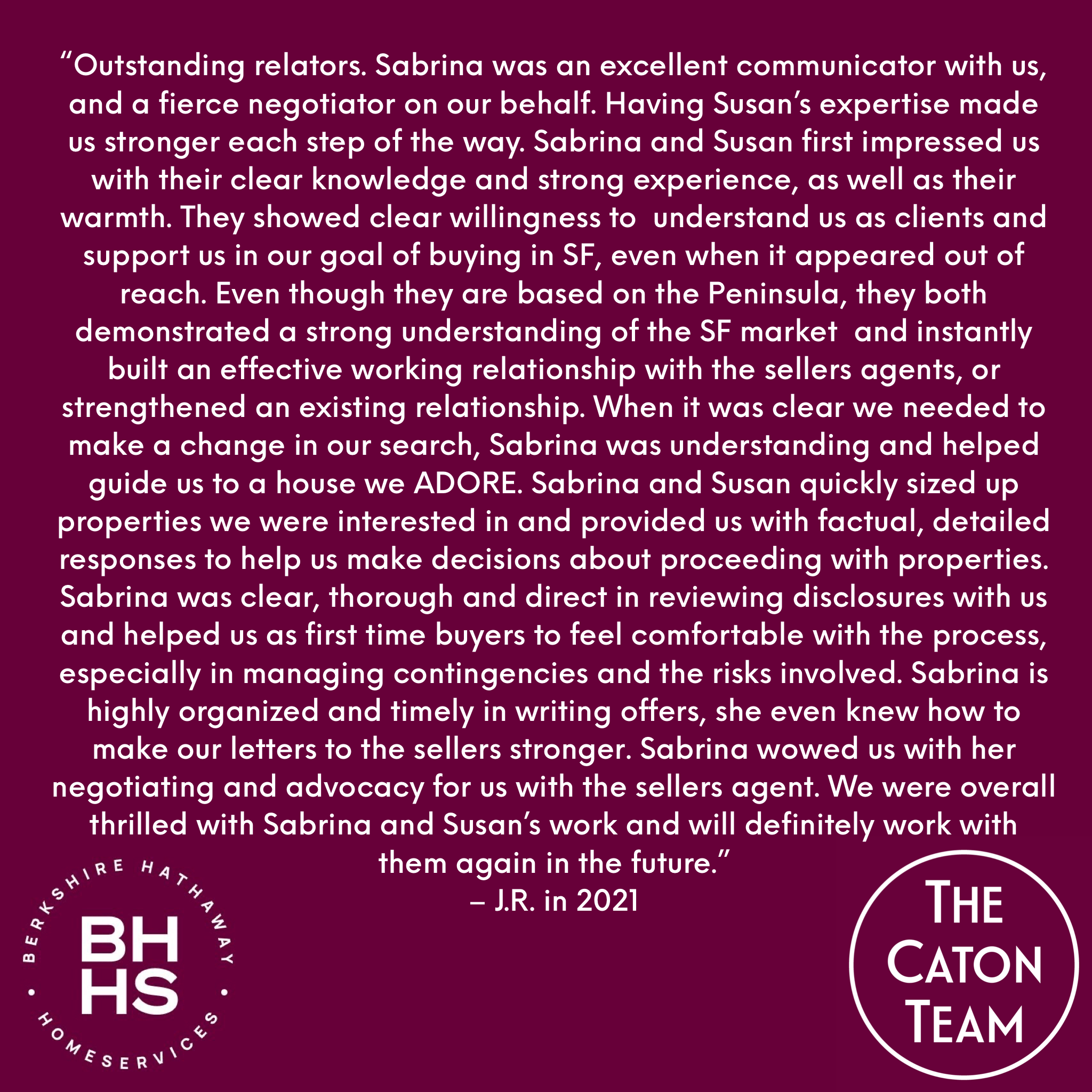

“Sabrina and Susan were an incredible help in selling our house. They moved at the pace we needed and answered every question we had. They adapted to the difficulties of selling in 2020 with ease. FANTASTIC! Thank you so much for all your did helping us. I appreciate how patient you were throughout and how helpful you were to me personally.”

– Ben

Got Questions? The Caton Team is here to help.

Call| Text | Sabrina 650.799.4333 |EMAIL | WEB| BLOG

We love what we do and would love to help you navigate your sale or purchase of Residential Real Estate. Please reach out for a personal consultation. Please enjoy our free resources below and get to know our team TESTIMONIALS.

Got Real Estate Questions? The Caton Team is here to help.

We strive to be more than just Realtors – we are also your home resource. If you have any real estate questions, concerns, need a referral, or some guidance – we are here for you. Contact us at your convenience – we are but a call, text or click away!

The Caton Team believes, in order to be successful in the San Fransisco | Peninsula | Bay Area | Silicon Valley Real Estate Market we have to think and act differently. We do this by positioning our clients in the strongest light, representing them with the utmost integrity, while strategically maneuvering through negotiations and contracts. Together we make dreams come true.

A mother and daughter-in-law team with over 35 years of combined, local Real Estate experience and knowledge – wouldn’t you like The Caton Team to represent you? Let us know how we can be of service. Contact us any time.

Call| Text | Sabrina 650.799.4333 | Susan 650.796.0654 |EMAIL | WEB| BLOG

The Caton Team – Susan & Sabrina A Family of Realtors Effective. Efficient. Responsive. What can we do for you?

:strip_icc():format(webp)/NozDesign_PurpleRoom-1_preview-932f7fb192dd40659018abe10c566c59.jpg)

You must be logged in to post a comment.