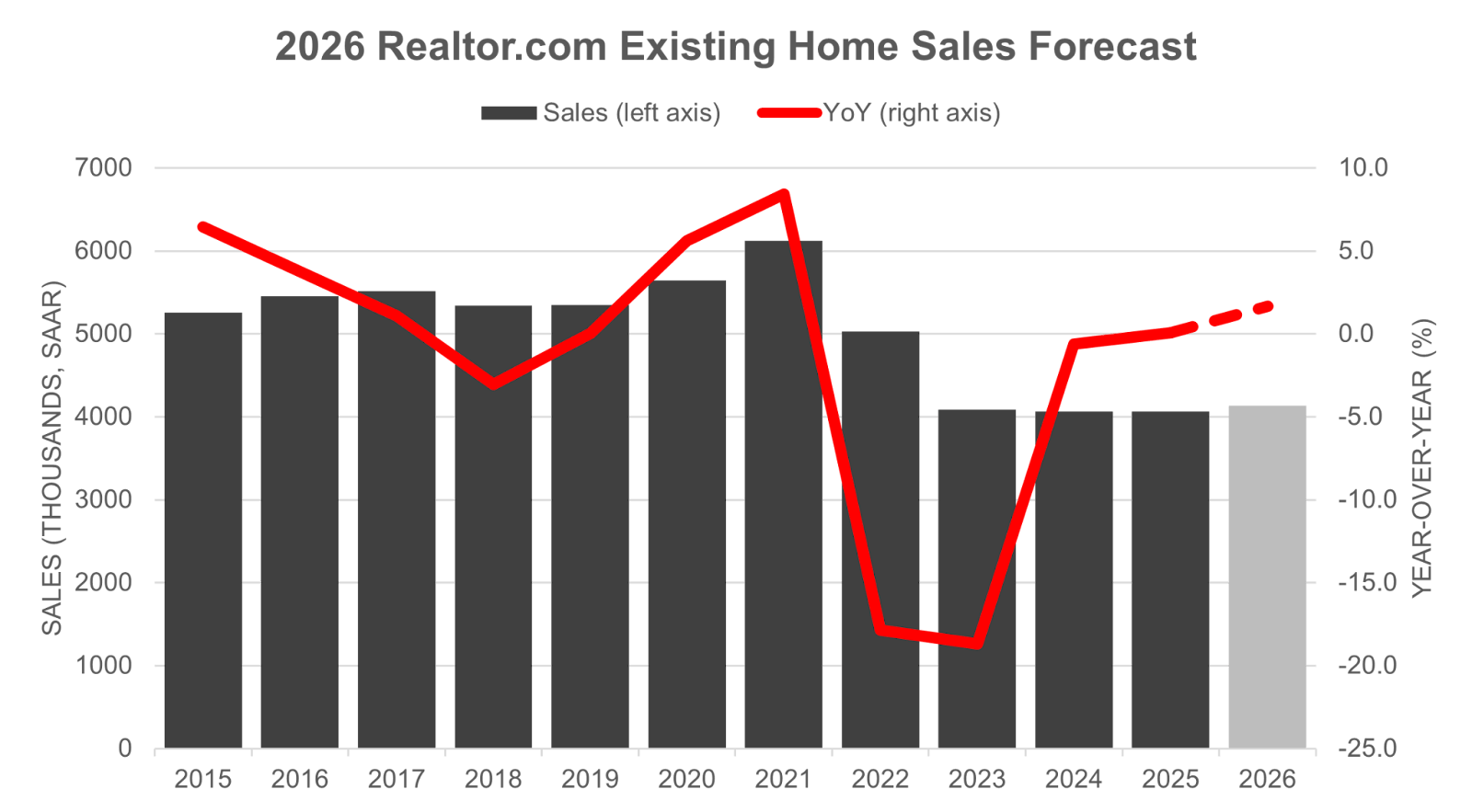

In 2026, we expect a steadier housing market, but it’s not yet off to the races. Mortgage rates are forecast to average 6.3%, easing affordability pressures slightly, while home prices rise modestly by 2.2%. Existing-home sales should climb about 1.7% to 4.13 million, a small but meaningful gain from 2025’s near 30-year low. At the same time, for-sale inventory will continue to recover, up nearly 9% year over year.

I read this article HERE. By Anthony Smith

For homebuyers and sellers, the shift signals a more balanced market—one where price growth steadies, rate relief offers breathing room, and negotiating power tilts subtly toward buyers. Housing affordability improves as incomes outpace inflation, pushing the typical payment share of income below 30% for the first time since 2022.

Meanwhile, renters benefit from softening rents—especially in the South and West.

Forecast Table

| 2026 Realtor.com Forecast | 2025 Realtor.com Full-Year Expectations | 2024 Historical Data | 2013–19 Historical Average | |

| Mortgage Rates | 6.3% (avg); 6.3% (year-end) | 6.6% (avg); 6.3% (year-end) | 6.7% (avg); 6.7% (year-end) | 4.0% (avg) |

| Existing-Home Median Price Appreciation (YoY) | +2.2% | +2.0% | +4.5% | +6.5% |

| Existing-Home Sales (YoY | Annual Total) | +1.7% 4.13 million | +0.1% 4.07 million | -0.6% 4.06 million | +2.1% 5.28 million |

| Existing-Home For-Sale Inventory (YoY) | +8.9% | +15.2% | +15.2% | -3.6% |

| Single-Family Home Housing Starts (YoY | Annual) | +3.1% 1.00 million | -4.3% 0.97 million | +6.9% 1.02 million | 0.77 million |

| Homeownership Rate | 64.8% | 65.1% | 65.6% | 64.2% |

| Rent Growth | -1.0% | -1.4% | -0.6% | +5.2% |

Home Sales Rise Modestly From Long-Term Lows

Existing-home sales are expected to edge up 1.7% in 2026 after a nearly flat 2025. Even with this modest rebound, existing-home sales will remain well below normal as high prices and financing costs continue to hold back demand.

If home sales eke out a gain in 2025, as anticipated, 2024 existing-home sales (4.06 million) will remain the record, 29-year low (in 1995, existing-home sales were 3,849,000). Looking ahead, we expect growth in home sales in 2026. Still, the improvement will be modest nationwide as familiar challenges—diminished affordability due to high prices and still-high mortgage rates—continue to weigh on homebuyers.

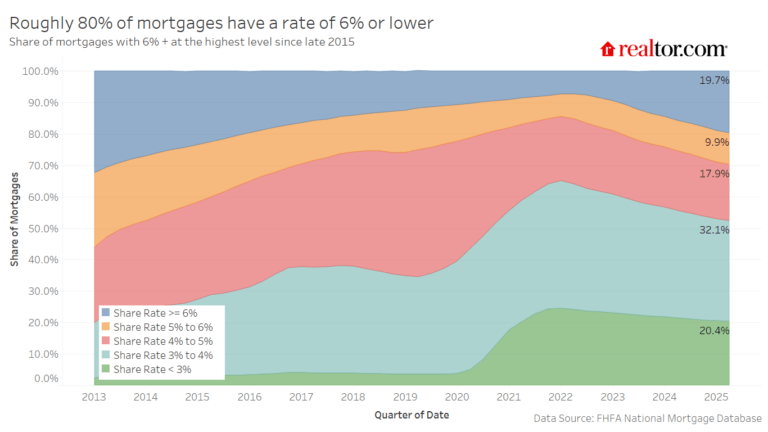

The mortgage rate lock-in effect—caused by market rates that are well above the rates on existing mortgages—has left many homeowners with a strong reason to stay put. In fact, recent data showed that 4 out of every 5 homeowners with a mortgage has a rate below 6%. The share has waned gradually, a trend that will continue in 2026. As a result, turnover will be limited with moves likely to be spurred by life necessities such as job or family changes.

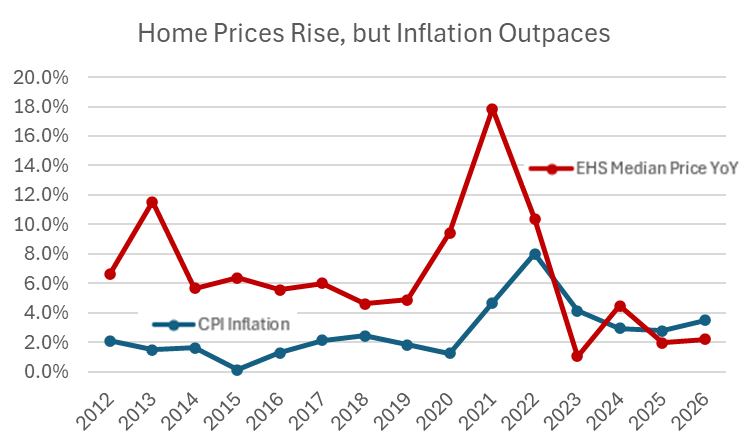

Home Prices Climb, but Not in Real Terms

Home prices are expected to continue to climb in 2026, adding 2.2% for the typical home sold. These gains come on top of the 2% increase registered in 2025. However, inflation is expected to outpace these gains, with consumer prices likely growing more than 3%. That means real (inflation-adjusted) home prices will decline slightly for a second consecutive year.

This dynamic—nominal prices rising but real prices slipping—gradually improves affordability, even if it doesn’t feel like a dramatic shift to most buyers or sellers. Put simply, the sticker price of homes keeps going up, but the overall price level and incomes rise faster, meaning that it takes a smaller chunk of each paycheck to buy a home. The slow normalization process helps buyer incomes catch up.

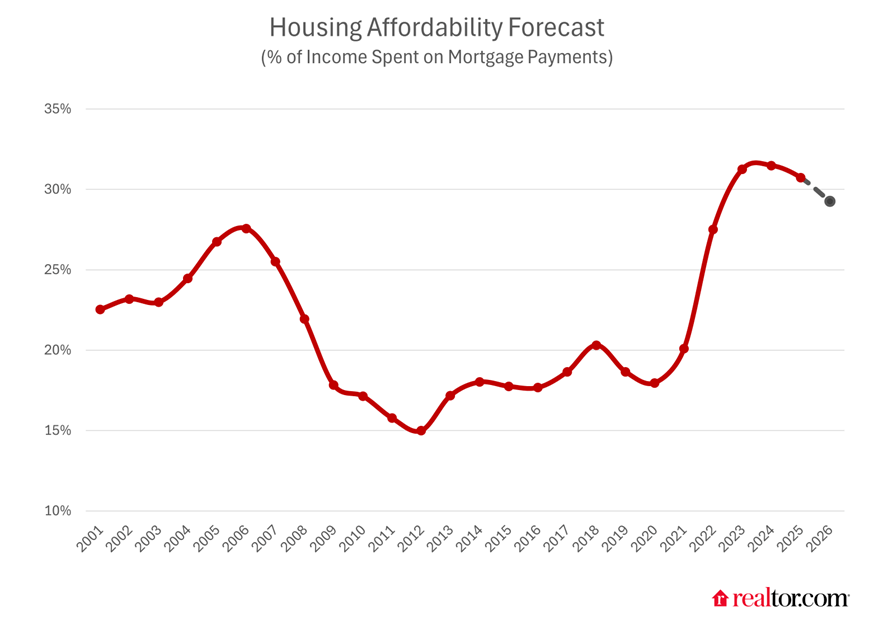

Affordability Improves as Mortgage Rates Steady and Incomes Grow

Even though home prices are expected to go up, affordability is set to improve modestly in 2026. After higher-than-expected interest rates in most of 2025, mortgage rates finally relaxed in the second half of the year, dropping into the low 6% range. We expect the average 30-year fixed mortgage rate to remain roughly in this range throughout 2026, averaging 6.3%, as slowing economic growth and the end of the Fed’s quantitative tightening offset rising U.S. government debt and inflationary pressure that’s expected to be temporary. While this puts the average 30-year fixed mortgage rate on par with the last few months of 2025, it will mark a drop from 6.6% on average throughout 2025 as a whole.

The typical monthly payment to buy the median-priced home sold is expected to fall 1.3% year over year as home price growth moderates and mortgage rates drop on average. This will mark the first decline in monthly payments on average across the year since 2020. Furthermore, rising incomes, which should outpace inflation, give buyers more purchasing power, helping to shrink the share of a paycheck that has to be put toward the mortgage. The monthly payment to buy the typical home is expected to slip to 29.3% of median income, its first year below the 30% affordability threshold since 2022, when mortgage rates shot higher. The gains may be modest, but they mark an important shift toward better conditions for homebuyers.

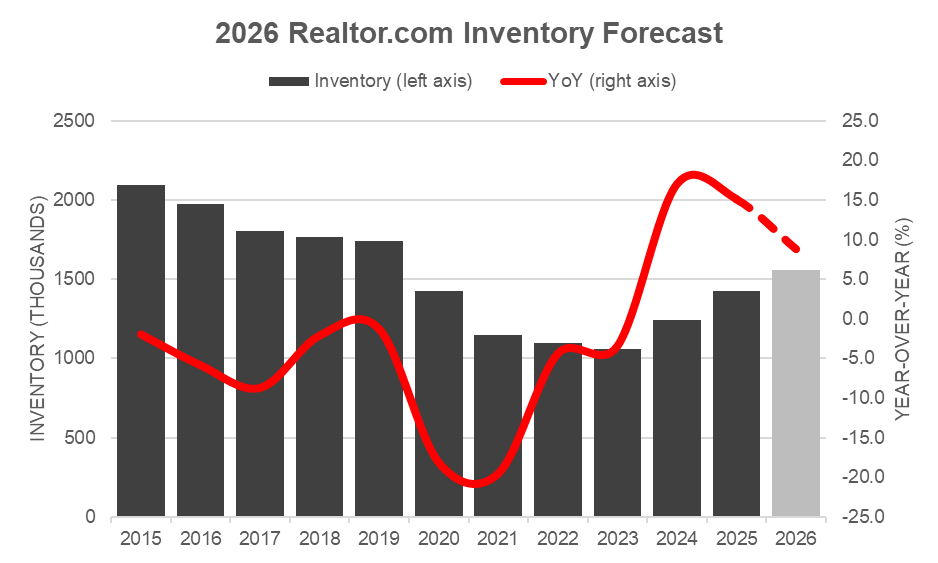

For-Sale Inventory Recovery Slows, but Still Outpaces Sales

Even though we saw some sellers delist rather than accept disappointing terms in 2025, the housing inventory recovery continued. The number of active for-sale listings marked two years of consistent growth in October, and the pace of annual unsold inventory recovery is likely to match 2024. Nevertheless, the pace of recovery has slowed as the market approaches pre-pandemic norms, and we expect this to continue in 2026.

We project an 8.9% increase in active listings in 2026, marking a third consecutive year of gains. The pace of improvement has slowed, however, as the market edges closer to pre-pandemic norms. By year’s end, nationwide inventory levels are expected to remain roughly 12% below pre-2020 averages, an improvement from a 19% gap in 2025 and nearly 30% in 2024.

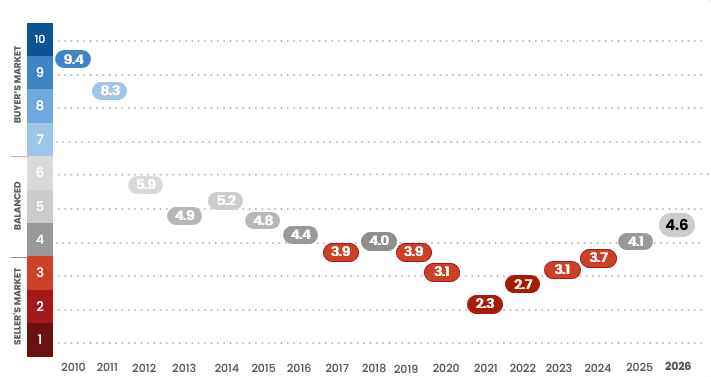

The national housing market will remain in balanced territory in 2026, averaging 4.6 months of supply across the year. Even so, momentum in the housing market is expected to tilt toward buyers as a more substantial growth in the number of homes for sale than homes sold shifts the balance of supply and demand. Housing affordability will remain a stumbling block for many, especially younger and first-time buyers, but negotiating power is expected to improve.

National Rent Softening Creates Mobility Opportunities Concentrated in the South and West

Renters are likely to see continued relief from declining rents in 2026, as a robust multifamily construction pipeline adds to rental supply and helps drive rents down. With more new units entering the market, vacancy rates are expected to approach—or even exceed—the long-term average of 7.2% observed between 2013 and 2019 by the end of 2026.

With rents declining for over two years and trends expected to continue in 2026, renter mobility is set to rise as more renters seek affordable housing or upgrades. Renters can find opportunities in markets such as Las Vegas, NV, Atlanta, GA, and Austin, TX, which have experienced the largest price drops from their peaks. At the same time, cross-market rental demand is expected to remain strong in metros like Raleigh, NC, and Richmond, VA, both emerging as top destinations for recent college graduates seeking affordability and career opportunities, as well as in Nashville, TN, which ranks among the nation’s top rental markets.

However, regional trends are expected to be a factor in the rental market in 2026. For renters living in expensive, high-density markets such as New York City, elevated rents will continue to pose significant affordability challenges. Even with rent freezes citywide—a policy preferred by Mayor-elect Zohran Mamdani—and sustained income growth, it would take decades—not years—for rents in New York City to become truly affordable.

New-Construction Trends

New-home construction has faced headwinds in 2025, from new tariffs on lumber and home finishings to a pullback in buyer demand resulting from high mortgage rates and low consumer sentiment. Builders have responded by pulling back on permitting and starting new projects at the same time that they push to sell completed inventory by offering incentives to buyers like mortgage rate buydowns and cash at closing.

New construction has emerged as an affordable alternative to resale homes, with the price per square foot of new builds actually falling below that of existing homes. With the number of newly built homes for sale near an all-time high, builders are motivated sellers—and they provide healthy competition to sellers in the resale market. The inventory of existing homes for sale is lacking low-priced, entry-level options in many markets, so builders are likely to continue to fill that gap, offering smaller and more affordable homes such as townhomes and rowhomes, which have been growing in popularity.

The Economy Continues To Grow Even as It Shows Strains From a Period of Rapid Adjustment

Nominal economic growth in 2025 slowed modestly as the economy weathered sizable changes to trade, immigration, and tax policy. The slowdown moved real, after-inflation economic growth back to trend from a period of above-trend growth. A similar on-trend economic performance is expected in 2026.

Inflation, which has been a thorn in the economy’s side for nearly a half-decade, reached a significant low point in spring—headline inflation hit 2.3%, per the consumer price index. This progress wasn’t sustained, however, and inflation picked back up as new tariffs affected the costs of goods, a trend we expect to see in 2026.

As economists debate the degree to which the Fed needs to respond or look through these price shifts, wages have continued to outpace inflation, creating real additional spending power for consumers. This has enabled household budgets to continue to catch up from the recent inflation-driven squeeze.

But a softening jobs market driven by companies paring back hiring and in some cases shrinking their workforce as they plan to right-size in the face of expanding AI capabilities and investment has put a question mark on whether wage growth will continue with the same strength.

Our outlook for 2026 expects median household income growth of more than 3.6%, which is just expected to exceed inflation, as it edges back up past 3%. Unemployment, which was at 4.3% in August, is expected to climb further, but not exceed 5% in 2026. In aggregate, consumers look to be in good shape, but lower-income and younger individuals may be more vulnerable as the labor market cools.

But Economic and Policy Risks Abound

The U.S. economy has weathered notable challenges in 2025, and several risks could cloud the 2026 outlook. Policy uncertainty around fiscal and trade measures may influence both inflation and consumer confidence. While the federal government has reopened, the recent shutdown caused some permanent economic loss, and the temporary nature of the continuing resolution means fiscal risk looms again at the end of January.

The possibility of a Federal Reserve policy misstep—either remaining too tight or easing prematurely—remains a key concern. Further, the Fed will experience a leadership transition as Jerome Powell’s chairmanship ends on May 15, 2026. A successor has yet to be named, although several candidates have been publicly discussed. The chair plays a strong role as the lead public voice of the Federal Open Market Committee, the body that makes monetary policy decisions, but the chair is also just 1 vote of 12, so the role’s impact on monetary policy is more indirect and will vary depending on the characteristics of the person who fills the role.

A softening labor market poses another risk: If job losses accelerate or wage growth stalls, consumer spending could weaken, potentially dampening both housing demand and economic growth. Additionally, inflation could fluctuate depending on how tariffs, energy costs, and global supply conditions evolve.

While a full-blown recession is not the base case, the economy is in a period of accelerated adjustment where a “misshift” in policy or sentiment could cause a temporary setback that would have implications for the housing market.

Housing Perspectives

What will the market be like for homebuyers, especially first-time homebuyers?

Homebuyers will see modest improvement in their bargaining power in 2026, as affordability and inventory inch higher, building on the gains they saw in 2025. Although the national housing market will remain in balanced territory, there will be substantial regional variation. Already in 2025, at least seven major housing markets have crossed into buyer-friendly territory, and that list is likely to grow in 2026. This doesn’t mean that the housing market will be “easy” for buyers, but we do expect to see more sales in 2026, a sign that more buyers will be able to successfully navigate the market’s challenges.

How can homebuyers prepare?

As affordability remains a top concern, buyers want to be financially ready to find success in the 2026 housing market, and that means not only knowing your budget numbers but also understanding the market norms and cheat codes. Where will extra financial effort pay off, and which goals are not worth pursuing?

Recent data shows that down payments have leveled off as some of the market competitiveness releases pressure to compete here. Buyers don’t need a record-high amount of cash to successfully buy a home, but the down payment size can still affect monthly housing costs. A larger down payment can reduce monthly costs by lowering the amount borrowed and also the mortgage rate buyers may be able to secure. Research shows that even as the typical homebuyer does not get all the way to a 20% down payment, those who are close to that threshold will see a big drop in their mortgage rate if they meet the 20% target.

New construction is another option to consider, especially for buyers in the South and West, where builders have been particularly active. As builders see the number of for-sale homes climb, they are trying to compete and are increasingly offering incentives to help buyers get to the closing table. A recent Realtor.com® study showed that mortgage rate buydowns—when a builder offers special, below-market rate financing—are among the most commonly offered buyer incentives.

Buyers in the Northeast and Midwest may find new construction harder to come by since it generally comprises a smaller share of for-sale listings in these regions. However, metros in these regions tend to have more abundant fixer-uppers. Buying a home that needs work isn’t without challenges, but it may be a move to consider for those with skills and the readiness for a project.

What will the market be like for home sellers?

In 2025, sellers faced a year of rising home inventory and sluggish sales. These trends combined to nudge the housing market away from a seller’s market to a balanced market for the first time in nine years, as we anticipated in our 2025 housing forecast. This momentum is likely to continue in 2026, when sellers will face a market moving even further into balanced territory.

Sellers who definitely want to sell will want to pay attention to the competition when setting a price, and they may need to be prepared to adjust expectations based on market feedback. The degree of adjustment will depend on their geography and their price point. Recent data shows that price cuts are somewhat more common among lower-priced homes, and comparatively rare among homes priced above $1 million.

Sellers who list, but are inflexible on price or other terms, may not find a buyer willing to meet them. An increasing number of sellers in 2025 chose to delist and walk away from the market, and this trend could continue in 2026. Fortunately, the lengthy average tenure among today’s homeowners suggests that many are in a position to walk away with good money if they were to choose to sell.

One source of demand that has remained relatively steady comes from investors who comprise just over 1 in 10 homebuyers in the most recent quarter nationwide, and up to twice that share in some metros.

What will the market be like for renters?

In 2026, rental supply is expected to continue outpacing demand, driving down rents and increasing renter mobility—especially cross-market rental demand. While more new multifamily units are anticipated to enter the market, a slowdown in permitting activity—potentially linked to tariffs on construction materials—could pose headwinds to future rental supply growth and exert upward pressure on rents.

Nevertheless, rental affordability is expected to continue improving in 2026, making renting a consistently cost-effective option compared with buying in the short term across most markets. Young adult renters, who lack access to historically high home equity to purchase a home, could take advantage of this trend by searching for more budget-friendly options and saving money in the process.

When evaluating housing options, it’s important to consider both market trends and how long you plan to stay in your next home. The Realtor.com Rent vs. Buy Calculator helps individuals and families compare the costs and benefits of renting versus buying, showing how long it may take before buying becomes the more financially advantageous choice. By providing tailored insights, the tool helps users weigh current and future trade-offs.

Local Market Predictions

All real estate is local, and while the national trends are instructive, what matters most is what’s expected in your local market. See below for a list of the largest metro sales and price growth predictions in 2026.

Methodology

The Realtor.com model-based forecast uses data on the housing market and overall economy to estimate values for these variables for the year ahead. The forecast result is a projection for annual total home sales increase (total 2026 existing-home sales vs. 2025) and annual median home sales price increase (2026 median existing-home sales price vs. 2025).

Got Questions? The Caton Team is here to help.

Cell| Sabrina 650.799.4333 | Susan 650.796.0654 | EMAIL | WEB | BLOG

We love what we do and would love to help you navigate your sale or purchase of Residential Real Estate. Please reach out for a personal consultation. Please enjoy our free resources below and get to know our team from our TESTIMONIALS.

Effective. Efficient. Responsive. The Caton Team 🏡

How Can The Caton Team Help You?

TESTIMONIALS | HOW TO SELL | VIRTUAL STAGING | A GUIDE TO BUYING | BUYING INFO | MOVING | TRUST AGREEMENTS | HEALTH CARE DIRECTIVES | TESTIMONIALS

Get exclusive inside access when you follow us on Facebook & Instagram

TESTIMONIALS | HOW TO SELL | VIRTUAL STAGING | A GUIDE TO BUYING | BUYING INFO | MOVING | TRUST AGREEMENTS | HEALTH CARE DIRECTIVES | TESTIMONIALS

Got Real Estate Questions? The Caton Team is here to help.

We strive to be more than just Realtors – we are also your home resource. If you have any real estate questions, concerns, need a referral, or some guidance – we are here for you. Contact us at your convenience – we are but a call, text, or click away!

The Caton Team believes, in order to be successful in the San Francisco | Peninsula | Bay Area | Silicon Valley Real Estate Market, we have to think and act differently. We do this by positioning our clients in the strongest light, representing them with the utmost integrity, while strategically maneuvering through negotiations and contracts. Together we make dreams come true.

A mother and daughter-in-law team with over 35 years of combined local Real Estate experience and knowledge – wouldn’t you like The Caton Team to represent you? Let us know how we can be of service. Contact us any time.

Cell | Sabrina 650.799.4333 | Susan 650.796.0654 | EMAIL | WEB| BLOG

The Caton Team – Susan & Sabrina

A Family of Realtors

Effective. Efficient. Responsive.

What can we do for you?

Website | The Caton Team Testimonials | Our Blog – The Real Estate Beat | Search for Homes | Facebook | Instagram | HomeSnap | Pinterest | LinkedIn Sabrina | Photography | Photography Blog

Berkshire Hathaway HomeServices – Drysdale Properties, Redwood City Ca.

DRE # | Sabrina 01413526 | Susan 01238225 | Team 70000218 | Office 01499008

The Caton Team does not receive compensation for any posts. Information is deemed reliable but not guaranteed. Third-party information not verified.

You must be logged in to post a comment.