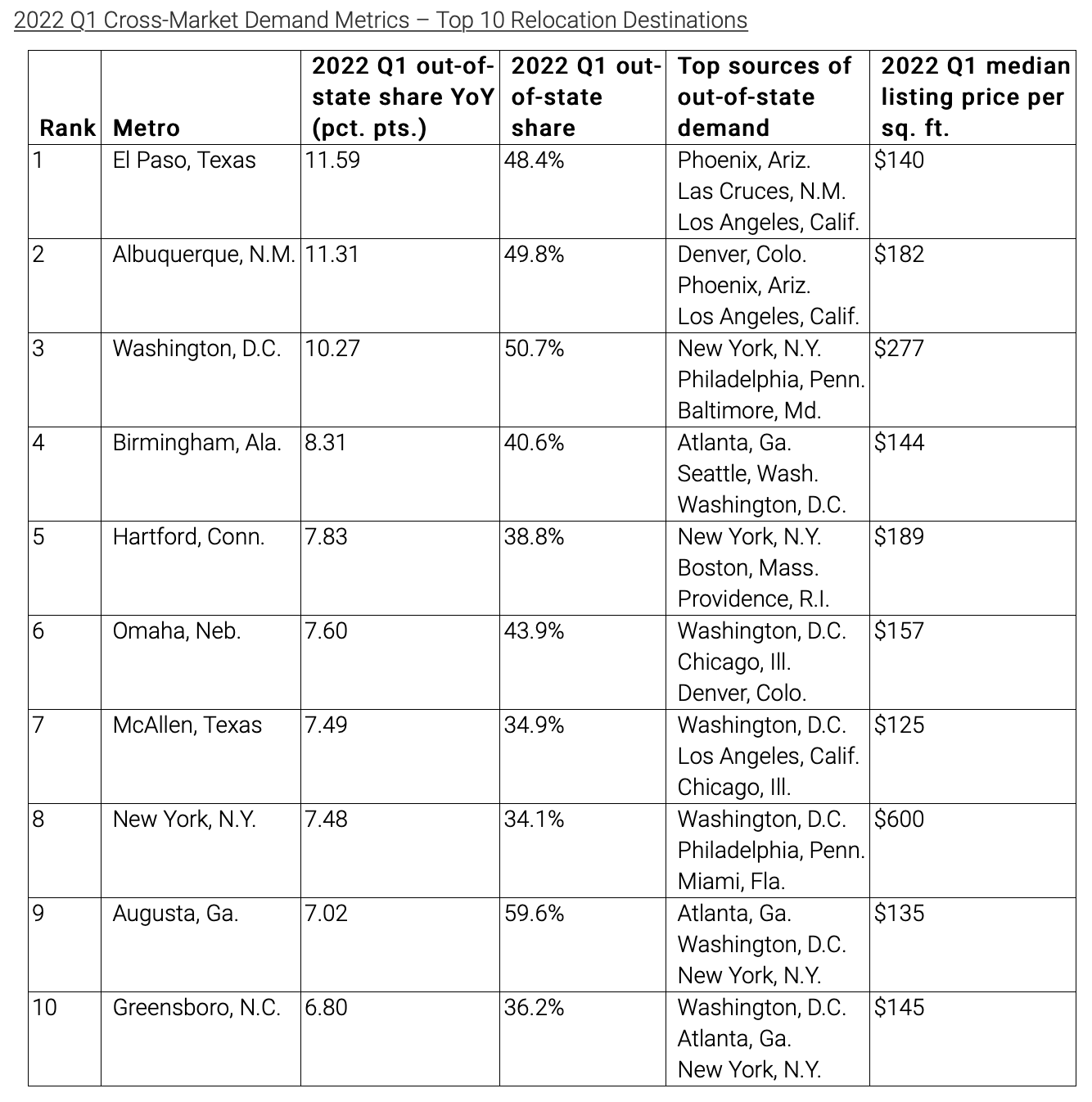

Home shoppers’ interest in relocating to a different state is on the rise, finds a new survey from realtor.com®. During the first quarter, 40.5% of prospective buyers searching for homes for sale on realtor.com® were looking for homes outside of their current state.

“After two years of pandemic remote work, offices have started to reopen, but instead of seeing a slowdown in the number of people interested in homes out of state, we’re seeing an acceleration,” says Danielle Hale, realtor.com®’s chief economist. “Taking a closer look at the top destinations, we see some very different trends driving the desire to live out of state and home shoppers’ diverse needs.”

Affordability remains a key focus for buyers, Hale says. Demand for less expensive areas has increased in recent months due to high inflation and rising mortgage rates. Also, the flexibility from the higher adoption of remote work is fueling greater interest in sunnier climates like the Sun Belt, Hale says. Some buyers also are showing renewed interest in living downtown. Two major metros made realtor.com®’s list of top destinations for out-of-state home shoppers.

The following are the top 10 relocation destinations, according to realtor.com®.

Source:

The Caton Team is here to help.

We love what we do and would love to help you navigate your sale or purchase of Residential Real Estate. Please reach out at your convenience for a personal consultation. Please enjoy our free resources below and get to know our team through our clients’ words. Testinmonials.

How can The Caton Team help You?

Call | Text | Sabrina 650.799.4333 | Susan 650.796.0654 | EMAIL | WEB | BLOG

Get exclusive inside access when you follow us on Facebook & Instagram

HOW TO SELL during COVID-19 – HOW TO SELL – HOW TO BUY during COVID-19- – HOW TO BUY – MOVING MID PANDEMIC – TRUST AGREEMENTS and HEALTH CARE DIRECTIVES – OUR TESTIMONIALS

Got Real Estate Questions? The Caton Team is here to help.

We strive to be more than just Realtors – we are also your home resource. If you have any real estate questions, concerns, need a referral or some guidance – we are here for you. Contact us at your convenience – we are but a call, text or click away!

The Caton Team believes, in order to be successful in the San Fransisco | Peninsula | Bay Area | Silicon Valley Real Estate Market we have to think and act differently. We do this by positioning our clients in the strongest light, representing them with the utmost integrity, while strategically maneuvering through negotiations and contracts. Together we make dreams come true.

A mother and daughter-in-law team with over 35 years of combined, local Real Estate experience and knowledge – would’t you like The Caton Team to represent you? Let us know how we can be of service. Contact us any time.

Call | Text | Sabrina 650.799.4333 | Susan 650.796.0654 |EMAIL | WEB| BLOG

The Caton Team – Susan & Sabrina

A Family of Realtors

Effective. Efficient. Responsive.

What can we do for you?

The Caton Team Testimonials | The Caton Team Blog – The Real Estate Beat | TheCatonTeam.com | Facebook | Instagram | HomeSnap | Pintrest | LinkedIN Sabrina | LinkedIN Susan

Want Real Estate Info on the Go? Download our FREE Real Estate App: Mobile Real Estate by The Caton Team

Berkshire Hathaway HomeServices – Drysdale Properties

DRE # |Sabrina 01413526 | Susan 01238225 | Team 70000218 |Office 01499008

The Caton Team does not receive compensation for any posts. Information is deemed reliable but not guaranteed. Third party information not verified.

You must be logged in to post a comment.